Dear Chuck,

Many of our friends are moving to the South. We are reluctant to leave our family, but the financial benefits seem worth it. What do you advise?

Considering a Move South

Dear Considering a Move South,

In January, I went to the dentist where I live in Tennessee. The dental assistant was new, so I asked her to tell her story. Since I could not really talk, I learned a lot! She, her husband, and their two children had recently relocated from California. She had done extensive research on all of the “lower 48” states looking for lower taxes, lower housing costs, access to outdoor recreation, mild weather, and a strong job market. Tennessee came up the overall leader according to their criteria, so they moved. But even more remarkable to me was that 12 other members of their extended family from California followed them! They all bought homes in close proximity to each other.

Relocation Trends

Extraspace.com reports that more than one in ten Americans moved in early 2021 alone. The shifting economy, remote work, and the desire for less densely-populated areas—all sparked by the pandemic—led to a migration to several key states. 35 million addresses changed last year.

Politics and crime are influencing others to relocate. People are moving to be near family. Others want bigger homes in the suburbs with yards for children and pets along with affordability and good schools.

North American Moving Services released a 2021 migration report. The top five states that people left are Illinois, California, New Jersey, Michigan, and New York. The top five states they moved to are South Carolina, Idaho, Tennessee, North Carolina, and Florida. The main reasons given include:

Other reasons people move are to escape high taxes, heavy traffic, and crowded cities, as well as the desire for better weather and proximity to outdoor recreation. I have included numerous charts that provide helpful information if you’re considering a move to another state.

Here are some practical helps: 42 moving tips and how to cut moving costs should you decided the benefits outweigh the overall risks.

Family

Pandemic restrictions revealed the desire for many families to live near one another. Assuming healthy boundaries can be established or are already in place, you will find numerous financial benefits of living close to your family. A few of these include free babysitters, reduced travel costs to visit at holidays, sharing tools and equipment, and passing down knowledge and skills. Young and old benefit from living close to one another as long as parameters are respected. Children and grandchildren benefit from serving older relatives. Older family members gain meaning and purpose in life by helping younger ones. Healthcare costs can decrease also.

In your case, moving away from family may be the determining factor whether you should move or not. One couple I met said they were able to budget for annual travel to see their family, and they were also to pay for airfare for some family members who wanted to visit them in their new location. This, too, can be an expensive consideration to factor into your decision.

Making a Wise Decision

An important aspect to consider is finding a new church. Research options in the city where you want to move. Stream services, and reach out to staff. If you can plug in before you move, it will make the transition much easier. We need the Body of Christ. Seek to get involved in a class and/or small group. They can help you navigate a new city, find doctors and repairmen, and answer other questions you may have. We have benefited from the weekly fellowship in our small group.

Pray, seek lots of wise counsel, and speak to your family about their views. Ask God for wisdom and direction to place you where He wants you to be, then come to unity with your spouse and children. It may be He wants you right where you are. I hope this information will help you make the best possible decision. If you come to Tennessee, be sure to say hello!

My new book, Economic Evidence for God: Uncovering the Invisible Hand that Guides the Economy, is available as of today. As you press into the evidence, it will become more and more exciting as you begin to see the world and even your own economic activity through an entirely new perspective. Money―and our personal and collective use of it―can be examined to reveal our faith, or lack thereof, and God’s ever-present reality in our affairs. I hope you enjoy it!

This article was originally published on The Christian Post on March 25, 2022.

Dear Chuck,

We’re trying to buy a house, and our realtor suggests we sign an “Appraisal GAP” clause in our offer that is above the asking price. Should we do it?

First-Time Homebuyers

Dear First-Time Homebuyers,

For some, it is a crazy real estate market right now! A member of our staff is trying to purchase her family’s first home, which has required them to offer up to 20% over the asking price in a very competitive real estate market. When they texted me this question, I did not know what they were talking about since I have never bid above asking for a home we tried to purchase. It took some research to understand the implications of this new trend in real estate.

Appraisal Gap

When a buyer makes an offer and the appraiser finds that the home’s value is less than the offer, a gap occurs. The home “doesn’t appraise” for the amount the buyer is willing to pay. When this happens, buyers may not find a lender willing to take the risk on a home that is valued for less than the purchase price. So the buyer must be willing to pay the difference in cash. An appraisal gap clause is an addendum to a contract confirming that the buyer will cover any difference between a home’s appraised value and the offer.

The rise of appraisal gaps is happening in parts of the nation where housing inventory is low and the demand for homes is high. Appraisals may not reflect the current value of a home. This happens when home prices accelerate fast. It gives sellers comfort in knowing a contract won’t fall through because of a low appraisal. It protects buyers from having to back out of a deal.

When a home is appraised, buyers have several choices to make. They can:

Consider Your Options

With an appraisal gap clause in your offer, you must buy the home even if it appraises lower than your offer. I recommend you avoid this due to the possibility that a market correction could create a situation where you are “upside-down” on your home or have “negative equity.” This would mean that you owe more or have more invested in your home than it is worth. Another option is to cap how much you’re willing to pay to cover the gap. This prevents you from spending more than you can really afford. Far safer for the buyer is to request an “appraisal contingency.” If the appraised value does not match a buyer’s offer, he/she can back out of the contract and keep any earnest money.

First-time homebuyers face many expenses other than the purchase of the home, such as moving costs, repairs, and upgrades or modifications to the house. It is wise not to overextend on the purchase price and deplete your savings. You will place yourself under enormous stress that can be unhealthy for your marriage and family.

Even though you may be renting now, you have a place to live, more time to accumulate savings for your eventual purchase, and the opportunity to take advantage of a better deal should market conditions change.

This is a good time to be patient and wait on the Lord. He knows your needs and will guide you to the best home for you in His time.

“Delight yourself in the Lord, and he will give you the desires of your heart. Commit your way to the Lord; trust in him, and he will act.” (Psalm 37:4-5 ESV)

While you are waiting on the Lord’s plan in the purchase of your first home, if credit card debt is an issue for your family, Christian Credit Counselors is a trusted source of help. They can help your family get on the road to financial freedom.

This article originally published on The Christian Post on March 18, 2022.

Dear Chuck,

I am being hit hard by the cost of gasoline. Haven’t you written about how to save money on this in the past?

Shocked By Gasoline Prices

Dear Shocked By Gasoline Prices,

Yes, I have answered this question before but not during a time when prices were rising this sharply! You and millions of others are feeling the pinch at the pump along with all the other products impacted by the rising cost of oil.

Prepare to Pay More

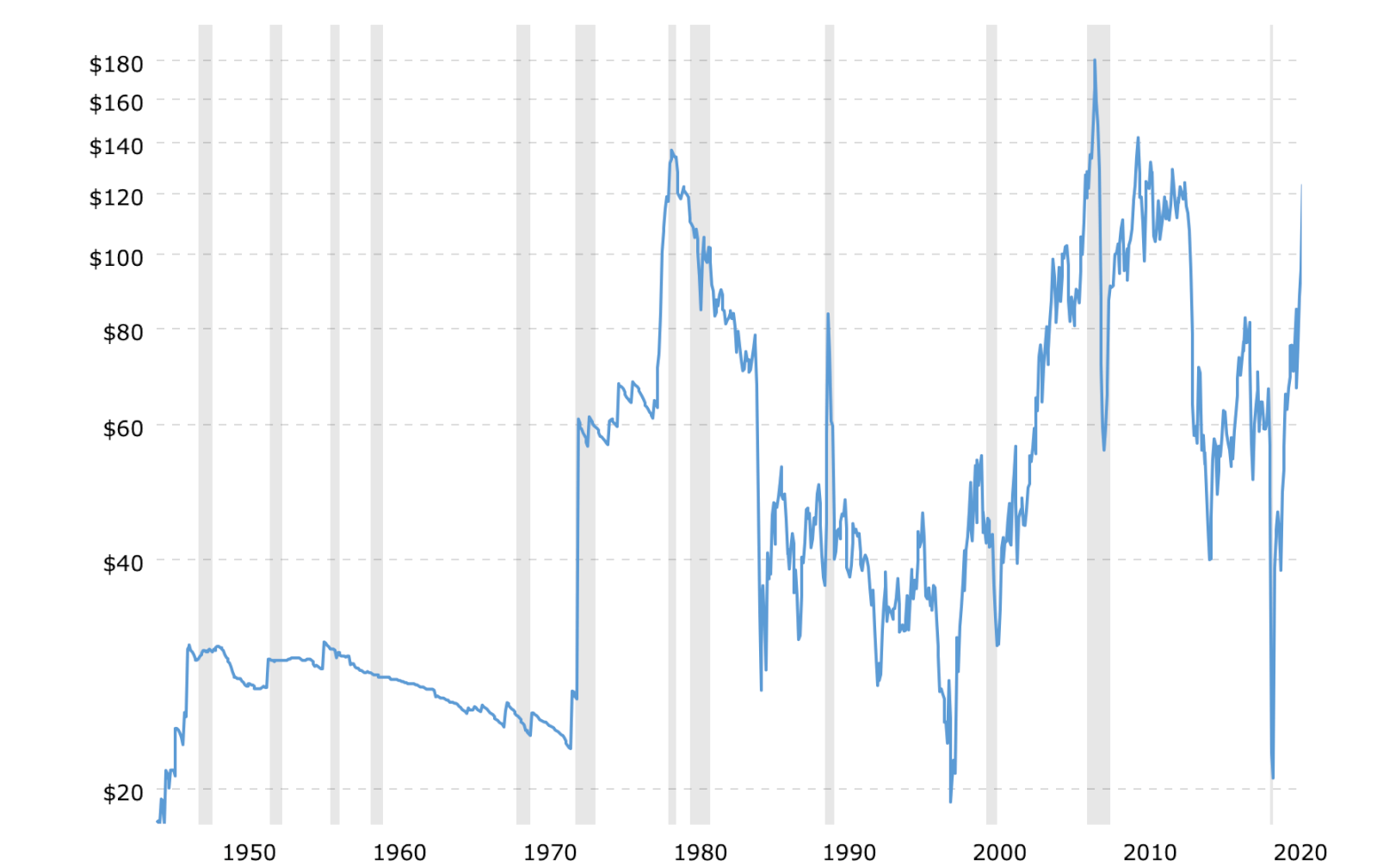

Patrick DeHaan of GasBuddy says, “As Russia’s war on Ukraine continues to evolve and we head into a season where gas prices typically increase, Americans should expect to pay more for gas than they ever have before. Shopping and paying smart at the pump will be critical well into summer.” The chart below shows the trendline of gas prices from the last 18 months.

Here is a short list of things you can do to save some money:

Here is a short list of things you can do to save some money:

Effect on Consumer Prices

The cost of crude oil affects the prices of everything we buy due to the impact on shipping and trucking. Expect to pay more for food at the grocery store, when dining out, on heating bills, and on things made with petroleum, like plastics and fertilizer. Those who need a bigger car should be on the lookout for used models that sellers will unload if gas prices get exorbitant

Keep It in Perspective

Crude oil prices fluctuate between extremes—often very quickly. Over the past 70 years, you can see in the chart below that these sharp spikes seldom last very long. Many believe that with the rise in purchases of electric vehicles, we will see a steady decrease in the price of oil. In the shorter term, a peaceful resolution to the war in Ukraine will hopefully reset the price—all the more reason to pray for peace.

A Recession?

Experts pose the possibility of this leading to a recession.

Troy Vincent, DTN senior market analyst, told CNET that if crude oil continues to rise, $6.50-$7.00 per gallon would not be impossible, though it could trigger a global recession.

Nicholas Colas, co-founder of DataTrek Research, covered the auto sector earlier in his career. He recently told msn.com: “The rule of thumb I learned from auto industry economics in the 1990s is that if oil prices go up 100% in a one-year period, expect a recession.” Thursday, March 4, 2021, crude oil was $63.81. Friday, March 4, 2022, WTI crude was $115. Monday, it touched $130 but dropped. In recent cycles, when oil gained 100% in a 1-year period, a recession occurred. This happens because consumers readjust their budgets so they can cut back, and spending declines. According to Kiplinger, the average length of recessions from 1857 forward is less than 17.5 months. This includes the 65-month recession of 1873 and the Great Depression, which lasted 43 months. (Check the website for more recession facts.)

Adjust Your Budget

Adjust Your Budget

Consider what you can give up to cover the higher cost of gasoline and consumer goods.

Turn down the thermostats, and dress in layers until temperatures rise this spring and summer.

Start a garden, grow some food, and shop at farmers’ markets. Supply an emergency long-term food pantry buying nonperishable food in bulk. Analyze vacation plans. Avoid extra airline fees when flying. Consider alternate means of transportation. It may be necessary to have a staycation or find a creative way to spend less while taking necessary time off.

Do Not Fear

When facing the lingering impact of the pandemic, a war, and inflation, there are many concerns right now. We can take comfort in God’s Word that reminds us that we have nothing to fear

Psalm 37:16 – “Better is the little that the righteous has than the abundance of many wicked.”

Psalm 112:7 – “He is not afraid of bad news; his heart is firm, trusting in the Lord.”

The Crown God is Faithful devotional provides inspiring and practical biblical wisdom. You can sign up to receive the devotionals daily to help transform not only your finances but also every area of your life.

This article was originally published on The Christian Post on March 11, 2022.

Dear Chuck,

I’m single and have saved enough money to buy a house and have a sizable emergency fund for any surprise repairs. Do you consider this a good time to enter the real estate market?

Single Home Buyer

Dear Single Home Buyer,

Reuters released an article on February 24th on the rise of the solo American homebuyer, which highlighted Bank of America’s recent survey of potential buyers. Results showed that singles do not want to delay a home purchase. Kathy Cummings, a Bank of America senior VP, relates: “9 out of 10 single women dismiss the idea of being married before buying a home. They see that as old-fashioned thinking.” In addition, the article noted:

Considerations on Buying a Home

The higher your credit score, the better opportunity you have to lock into a good mortgage rate.

Get pre-approved so you can act quickly when the right house becomes available. I recommend a minimum 20% down payment so you can avoid private mortgage insurance.

When budgeting the cost of buying a home, include insurance, property taxes, utilities, repairs, maintenance, HOA fees, landscape, trash pickup, appliances, window coverings, furniture, renovations, etc.

In purchasing a home, you lose flexibility but gain fixed costs and equity. A roommate can help with bills. Do you think you will stay put for a while, or is there a chance you will have to relocate? If relocation is a possibility, would you sell, or could you rent the home?

When Jesus taught a crowd about the cost of discipleship, He gave the example of building a tower. First, sit down and calculate the cost to complete it (Luke 14:28-30). Everyone who contemplates buying a house must do the same.

Interest Rates

The national average 30-year fixed mortgage rate on Tuesday, March 1, 2022, was 4.30%, an increase of 8 basis points from the previous week. The national average 15-year fixed mortgage rate was 3.5%. The national average 30-year fixed refinance rate was 4.23%, while the 15-year fixed refinance rate was 3.49%.

Greg McBride, chief financial analyst at bankrate.com, recently stated, “Although the national average on a 30-year fixed rate mortgage is above 4 percent, plenty of sub-4 percent rates are available for borrowers that shop around. Conducting an online search can save thousands of dollars by finding lenders offering a lower rate and more competitive fees.”

McBride recommends steering clear of adjustable-rate mortgages for now. He says, “While rapidly rising mortgage rates may temper the demand somewhat, don’t expect home price appreciation to come to a halt. A more modest pace of appreciation is the likelier outcome.”

Check bankrate.com for the latest rates and offers below the national average.

Is Now the Time?

Many are asking, is now the time? From a personal standpoint, you need to consider if you are financially stable and ready to lock into a mortgage, with no guarantee that the home will retain its value over 15–30 years. Is your career inflation-proof? Can you afford a plumber or electrician, or can you make repairs? If you are okay financially, remember we are in the midst of the lowest inventories of available homes in decades.

In today’s market, depending on the state that you are in, you may have to consider how high you are willing to bid on a home. One of our staff members placed an offer on a home in February that was 15% higher than the listing price! The seller received better offers than theirs, so they were not able to purchase the home they really wanted.

It was not very long ago, during the Great Recession (2008-2009), that people were contacting us for help after the value of their home dropped below the amount they had financed to purchase it! It was a painful and devastating time as many families experienced foreclosure.

Only God knows the future. I surely do not. If you believe you are ready for the responsibility of homeownership, there are many advantages, not the least of which is benefiting from building equity and from inflation. Using the qualifying questions above, it can be a blessing. Pray for wisdom, and seek wise counsel before you enter into a contract for purchase. Be patient. Allow the Lord to guide you to the home that is best for you. Thanks for the question.

In the meantime, if you find yourself needing help with credit card debt, Christian Credit Counselors is a trusted source of support. They specialize in assisting people with getting out of debt and on the road to financial freedom.

This article was originally published on The Christian Post on March 4, 2022.

Dear Chuck,

Inflationary prices are hitting our family, and I am getting worried. What can we do to ride this out?

Inflation Fears

Dear Inflation Fears,

Gasoline is way up, oil is way up, food is way up, rents are rising, and housing prices are soaring. The price of used cars is nuts—in my opinion. Inflation is definitely impacting us all!

My wife and I lived through the inflationary period of the ‘80s and survived. We were a young, married couple and didn’t always make the best decisions, like buying our first home with an adjustable-rate mortgage when mortgage rates for 30-year fixed-rate loans hit 18%. But I learned some helpful lessons that I can pass on here.

Make Some Key Adjustments Now

As the price of goods and services increases, our purchasing power decreases. There are several things you should do because things could get a lot worse before they get better.

It is important to know and understand your true financial picture. Last year, the Penny Hoarder conducted a budgeting survey of 1,900 Americans. Results showed that those who kept a budget were more likely to know how much they spent the previous month and less likely to splurge on a purchase that hindered their ability to pay bills. More than half (56%) of the respondents did not know how much money they had spent the last month.

Of those who use a simple budget, 40% use a spreadsheet, 14% use an app, and 12% use the most basic method of all—the cash envelope system. Here’s how to get started. You may benefit from the advice and helpful assistance of a Crown budget coach.

Prioritize God’s Way

Give first to honor the Lord with all that He has provided. He offers us the only guaranteed return with money—treasures in Heaven. After giving, pay yourself next (save); then prioritize what you can spend on your bills. Warren Buffett says, “Do not save what is left after spending, but spend what is left after saving.” This will give you financial margin and increase your options to overcome the erosion of your spending power by being able to invest in assets that benefit from inflation. That is the best way to keep up with the rising cost of goods and services.

Evaluate Your Income

Determine if your company is benefiting from inflation or getting hurt by it. If your career is in a field that cannot make adjustments to rising costs, your employment may be threatened should inflation persist. Consider alternative sources of income, or begin looking for employment that can endure—or even thrive—during inflation. If you have children nearing adulthood, emphasize the importance of inflation or recession-proof careers. Here are some suggestions along with some work-from-home ideas.

Hyperinflation

Hyperinflation, though rare, usually occurs when a government prints too much money. The more money in circulation, the less a currency is worth. As value drops, more money is needed, so more is printed, and prices rise faster. Consider what happened in the following nations:

America is not near hyperinflation levels, although our government has indeed printed an excessive amount of money before and during the pandemic. It is difficult to control inflation, so we must keep a watchful eye for signs that hyperinflation has become a real threat.

I have traveled to parts of the world where people survived hyperinflation. They have lived through what many would consider the Americans’ worst nightmare: losing all we have in terms of our worldly wealth. Yet the Christians who lost everything really did not lose “everything.” They became rich in the things money cannot buy. They learned to trust God in the midst of their financial pain. Things become less important than relationships. People sacrificially shared with one another and discovered the joy of giving and serving. One family believes it was the best thing that ever happened to them since they gained far more “true riches” than they lost in the temporal wealth of this world.

Be Prudent

I will write more about this as we watch changes in fiscal and monetary policy; however, you are wise to be prudent and make adjustments now. We are not guaranteed what the future will hold, but we can weather all storms when our house is built upon the Rock.

The Crown Stewardship Podcast is a valuable resource during these uncertain times. It is a wonderful tool to help guide you in the many facets of God’s financial principles. You can subscribe for alerts of new episodes. I hope you find it beneficial.

This article was originally published on The Christian Post on February 25, 2022.

Dear Chuck,

My female boss frequently laces her comments with profanity in the office. While it is never directed at me personally, it makes me cringe when I hear it. I have lost respect for her leadership and want to change jobs. Should I approach her or quietly find another place to work?

Tired of the Profanity

Dear Tired of the Profanity,

Many people in the workforce likely have had similar experiences and thoughts about what to do. I hope I can help you make a good decision regarding the choices you have presented.

Profanity at Work

While I did not find a lot of current research on the topic, according to a 2016 Wrike survey, it is far more common than we may think.

A majority of people (57%) say they swear in the workplace; however 41% feel that swearing is too casual and unprofessional. Here are some other findings:

I actually found some research claiming that people who cuss at work are considered smarter and more honest than non-cussers. I would disagree on both conclusions. Fortunately for you, the cussing by your boss has never been directed at you personally. Unfortunately for me, I have been personally cussed out on the job—not once, but twice. It happened when I was 16 and again at 26. These are experiences I will never forget.

Taming the Tongue

Although incensed by each experience, I somehow did not return curse for curse or condemnation for condemnation. Believe me, I had plenty of colorful things I wanted to say in retaliation for the stinging blow to my pride. In both cases, I was falsely accused. In both cases, I remained calm, refusing to get into verbal battles. In both cases, I later received an apology from the person who issued the tongue lashing. One, who in anger described me as similar to an uneducated donkey (among other things), went out of his way to call me, apologize, and explain that he was also disarmed by my self-control during the call when his outburst happened.

Like you, I have been around successful business leaders who, while not cussing me or anyone else out, used the F-bomb and foul language in their normal interactions with others. Without fail, I have thought less of them for their lack of discernment.

The word profanity means unholy, debased, irreverent, or impure. As Christ followers, we are admonished to avoid cursing. Words are powerful.

“Death and life are in the power of the tongue . . .” (Proverbs 18:21 ESV)

“Answer not a fool according to his folly, lest you be like him yourself.” (Proverbs 26:4 ESV)

“The heart of the righteous ponders how to answer, but the mouth of the wicked pours out evil things.” (Proverbs 15:28 ESV)

“A soft answer turns away wrath, but a harsh word stirs up anger.” (Proverbs 15:1 ESV)

Those who are in Christ are new creations. Christ reconciled us to Himself, made us His ambassadors, and gave us the ministry of reconciliation. In all our verbal interactions, we should be conscious of this fact. We represent the Lord wherever we go. Those who know us as Christians will observe our work ethic, our treatment of others, and the words we speak.

Speak Up or Change Jobs?

My suggestion is to pray for the right attitude, then set a time to privately speak to your boss. With gentle, non-condemning words, let her know you would prefer not to be subject to her (or others’) profanity on the job. If she receives it well, you have won a friend. If she is offended by your comments, be prepared to seek other employment, but give it a chance for improvement—before slipping silently away.

For inspiration and instruction on a number of financial and career topics, tune in to the Crown Stewardship Podcast. It is a wonderful tool to help guide you in the many facets of God’s financial principles. You can subscribe for alerts of new episodes. I hope you find it a valuable resource!

This article originally published on The Christian Post on February 18, 2022.

Dear Chuck,

We have to cut our spending this year, but I really don’t know where to begin. When I bring up the subject, my spouse always has an excuse. If we don’t get things under control, we are going to face eviction from our landlord.

Cash Crunch

Dear Cash Crunch,

I’m so glad that you wrote to me and are ready to make some big changes. My hope is that if you set a clear direction, your spouse will be inspired to join in the effort. Forced eviction is devastating emotionally; it is expensive and wrecks your credit score. Let’s work hard to avoid it!

Some of the obvious ways to reduce spending include eliminating the big expenses, like a car payment or rental/living costs in excess of 40% of your net spendable income. Look at both of those expenses closely, and determine if you need to make any changes. If not, there are some not-so-obvious ways you can save money each month that really add up over time. Cutting what seems like a necessity may seem impossible, but over time, the sacrifice will prove rewarding. Here are a few examples I want you to consider.

Do You Really Need Amazon Prime?

Membership fees jump for new members on February 18th. Renewals take the hit on March 25th. The annual cost will be $139/year plus taxes or $14.99/month plus taxes. An alternative is to keep a shopping list until you reach a total that qualifies for free shipping from Amazon or other companies. You may have limited shipping options, but this leads to better planning and less impulse purchasing. You can also use Amazon gift cards to limit spending since a credit card is not linked to your account.

Do You Really Need That Streaming Service?

According to The Streamable, in 2021, the average viewer had five or more subscriptions. The top five include Netflix, Amazon Prime, Disney+, Hulu, and HBO Max. In May 2021, Bloomberg reported that the average streaming consumer spends $40 per month. That comes to $480 per year! Different streaming prices can be seen here. The average cost of cable TV comes in at $64 but can run from $11 to $127 or more per month.

Do You Really Need Audible or Spotify?

Free audiobooks are available via Overdrive and Hoopla with a library card. Spotify and other small monthly fees that seem insignificant can really add up. Nothing is too small to eliminate to help you avoid eviction!

There’s More

Look at your spending with a critical eye. What could you realistically eliminate? What are your real needs? What do you need to reprioritize? Small daily purchases can add up quickly.

Analyze what is spent on subscription services, fast food, coffee, bottled water, shoes, clothes, gym membership and gear, house plants, manicures, pedicures, tattoos, haircuts and color, lottery tickets, toys for children, etc.

Challenge

Ask your spouse to join you in tracking all spending for the next 30 days. When Ann and I did this years ago, we found that recording each dollar spent made us more aware of our actions. We realized that we had some costly habits. Write down your expenses. Don’t leave anything off your list so that you know where your money is really going.

After 30 days, come together and share what you learn. It may only take a few days before a heightened awareness sets in. Prayerfully discuss what you could sacrifice for six months or a year. I suggest you gently educate your spouse on the long-term benefits. Can you agree to get the help of a mentor or come under the accountability of trusted friends? How about planning a reward when reaching your goal? You can likely cut back on your spending 25% by just changing some of your habits.

Once you get your spending under control and avoid eviction, there are many other reasons people decide to better manage their money. Reduced spending builds the habit of saving, and with the help of automatic deductions, people learn to live without. The possibilities can include:

Years ago, a woman confided in my wife that she was tired of her husband limiting her spending. She felt like she was being treated as a child. Ann listened and then asked, “Have you considered the possibility that he loves you so much that he wants to protect you and save for your future together?” The thought had never entered the woman’s mind. It changed her entire perspective and opened the door to healthy dialogue about their finances.

We enter marriage with a philosophy of money. Most often, we marry an opposite. The goal is uniting around God’s principles regarding our finances. Pray about how to lovingly communicate with your spouse. Treat him/her with respect and love so you can make progress. My desire is to see God’s people free and marriages united, strong, and thriving. We must recognize the errors in what the world has taught us about finances and have our minds renewed by God’s truth. With Valentine’s Day just days away, consider this effort to lead the way out of this crisis the best gift you can give your spouse.

If credit-card debt is a source of frustration in your marriage, consider contacting Christian Credit Counselors. They specialize in assisting people with getting out of debt and on the road to financial freedom, and they are a trusted source of help.

This article was originally published on The Christian Post on February 11, 2022

Dear Chuck,

My wife and I are aggressively saving for a down payment on a house. We’ve toyed with the idea of selling one of our two cars. Is that too radical?

First-Time Homebuyers

Dear First-Time Homebuyers,

This is a great question. Because of the inflationary market we are in right now, it is somewhat risky to sell a car and buy a house. As opposed to telling you what to do, I think some context will help you make a wise decision. I also have some Bible verses for you to consider.

Sell The Car or Keep Two?

One of my sons recently totaled his car after hitting black ice. By God’s grace, neither our son nor any of the other people in the six-car pileup were injured. He borrowed mine so he could get to work until insurance took care of his car. My wife and I were able to make do because we work remotely. When one of us needed a vehicle, we simply planned ahead and combined errands. Fortunately, our flexible schedules made it work. However, your question of what to do with the second car depends on three factors:

Let’s take a quick look at each question. First, if the car is older, it likely has marginal value, and it may be best to hang on to it because used cars are very expensive to replace if you suddenly realize that you need a second vehicle.

Second, whether or not it is radical to sell one of the cars depends on where you live. Is it radical for someone living in New York City? No. What about for the Amish? No. How about for an American suburban family? Yes. But, hey, being radical does not mean it is bad. Many financial decisions require us to go against the flow of what everybody else is doing.

The third question about lifestyle is important because as a first-time homebuyer, you may have two incomes right now, but a family may be in your future that could change your transportation needs quickly.

The cost savings of going from two vehicles to one can quickly add up. Lizzie Nealon at Bankrate reports that the total cost of owning a new car last year was $9,666. A report in June 2021 revealed that American households spend an average of $5,435 a year just on auto loans and insurance. The costs add up quickly when owning a vehicle, yet most people are unaware of the total expense. Consider this in your equation apart from what you would get for the price of the used vehicle. You will save on:

Options besides owning a car can include public transportation, walking, biking, carpooling, or car sharing through companies like Enterprise or Zipcar. If needed, you can reserve an Uber or simply rent a car. We’ve done that for road trips on numerous occasions.

So there is some great upside to unloading an unnecessary car in the current seller’s market. Besides getting your equity together, you can use the savings for building an emergency fund, paying down debt, saving for a major purchase, going back to school, starting a business, etc. If you decide that going from two cars to one is just too difficult, consider ways to lower the cost of ownership. Minimize depreciation by finding a car that holds its value. Look for good fuel economy. Shop around to get a good rate for insurance. Try to drive less by planning ahead and combining errands. Then find a reputable mechanic who will perform routine maintenance and any necessary repairs.

First-Time Home Buying

Buying a home right now is risky, too, because it is so expensive. Yes, a home is a good hedge against inflation and is the number one source for wealth building in an average American household. However, the first-time buyers I have been counseling feel they are being forced to stretch $50,000 to $100,000 more than they are comfortable spending just to get a house in an area they want. On top of that, all of the costs of homeownership are rising, such as insurance, taxes, utilities, maintenance, and remodeling. Our oldest son recently told me that the decision to rent for 10 years helped them be ready for buying their first home. They bought a fixer-upper that had been foreclosed upon. It looked like a disaster to me. Yet their eye for design and sweat equity paid off in a handsome profit and led to a comfortable purchase of their future homes.

Here are my rules of thumb for first-time home buyers. Have a 20% down payment. Don’t pay Private Mortgage Insurance. Have at least $10,000 in emergency savings after you move in. Be sure you can live there 5–7 years. Do you meet that high bar? If so, go for it.

Reflect on These Proverbs

“Better to be a nobody and yet have a servant than pretend to be somebody and have no food.” Proverbs 12:9 ESV

“One person pretends to be rich, yet has nothing; another pretends to be poor, yet has great wealth.” Proverbs 13:7 ESV

The Bible supports the idea that we should avoid putting on appearances to impress others when, in reality, we are living foolishly. We often have to make sacrifices to get ahead. So if you decide to go “radical,” let me know how you get along.

In the meantime, if you need help navigating any current debt, Christian Credit Counselors is a trusted source of help.

This article was original published on The Christian Post on February 4, 2022.

Dear Chuck,

My adult children rarely cook. They eat out and have groceries or meals delivered. I’m on a mission to teach my grandchildren how to cook—to prepare them to save money and become more self-sufficient in the future. I want to make it fun but could use some tips.

Cooking Up Some Savings

Dear Cooking Up Some Savings,

Food and entertainment can average 15% or more of the average American budget. This is a great way to help your grandchildren (and maybe your children too) learn to save a lot of money over their lifetimes. However, I am pretty limited on how to make cooking fun. So, I have asked my wife, Ann, to help me out here. She does a great job holding our food costs down!

My Limited Experience

While I was in college, my Dad paid for all my meals. Most were eaten in the campus cafeteria. When I got married, we ate most of our meals at home as a means to save money. Since Ann knew how to cook and I did not, my experience at it remains very limited. That was in 1978. Today, many young people, married or single, do not know how to cook or even how to shop for groceries.

Twenty years ago, Ann and I led a group of teenage Boy Scouts through the Crown Bible Study for Teens so they could earn a particular merit badge. They learned basic financial concepts—the importance of keeping a budget, avoiding debt, and so on. Before graduating, we wanted them to learn how much they could save by cooking their own food vs. eating out. We had them bring $5 for a meal that Ann cooked. They loved it. The following week, they brought $5 to eat out, and they chose a pizza buffet. Even those teenage boys noticed how much farther their money went by eating at home versus eating out.

Look at the Numbers

Yahoo! Finance reported that a survey by Visa found that the average American spends about $20 a week eating out for lunch. That comes to over $1,000 per year—for just one person. Priceonomics conducted research and found that “on average, it is almost five times more expensive to order delivery from a restaurant than it is to cook at home. And if you’re using a meal kit service as a shortcut to a home cooked meal, it’s a bit more affordable, but still almost three times as expensive as cooking from scratch.” The average price per serving based on 86 meals revealed the following costs:

Why People Eat Out

Why People Do Not Cook

Many recognize the need to change their habits. They want to save money, eat nutritiously, and impact their children’s futures. Start by learning to make one meal well. Learn to master something. Me? Well, I like to cook eggs and make smoothies. Let’s get Ann’s take.

Tips From Ann

With the goal of making cooking and eating at home appealing, prepare ahead by knowing what you plan to cook and gathering all ingredients. Consult cookbooks, websites, YouTube, or cooking shows to plan your menu. Search for budget-friendly, nutritious foods. After a few tries, you will gain confidence and should venture out into other meals.

Aim to make mealtime special by including the entire family. Rotate preparation, cooking, and clean-up chores. Teach children how to set the table, then let them be creative with cloth napkins, dinnerware, and centerpieces. Consider eating in different places, indoors and out. Turn off the TV and put away electronics to allow for family communication. Invite friends to join you. Ask relatives to demonstrate how to prepare favorite foods. Invite internationals in to teach you to cook specialties of their culture. Pick a night of the week to have a certain meal. This will cut down on menu planning: Meatless Monday, Taco Tuesday, Crockpot Night, Soup and Salad, Pizza or Pasta, Breakfast for Dinner, etc. Also, consider a baking competition where someone judges the dishes your grandchildren make. You will be surprised what a little recognition will do to motivate them.

Discover salvage and surplus grocery shopping to stock your pantry at reduced rates. Take the grandkids with you to learn. It is always a treasure hunt. Skip the prepackaged, microwavable stuff, and learn to eat fresh foods. God made them for us, and they are full of vitamins. Limit the foods that cause inflammation in your body, and you will save money and also improve your health.

My Tips

Eating out is a treat in our home. Ann and I have our favorite spots. We try to find coupons or ways to save while enjoying the splurge. We prefer to eat lunches out when we can since they are less expensive than dinners. We have not ordered a beverage at a restaurant in years. Water is good for you and saves a crazy amount on your total bill. Sometimes, we split an entrée, and we seldom order desserts.

It is interesting to note that the ant is considered wise for planning and storing its food supply in advance. “Go to the ant, O sluggard; consider her ways, and be wise. Without having any chief, officer, or ruler, she prepares her bread in summer and gathers her food in harvest. (Proverbs 6:6-8 ESV) Good stewardship eliminates the waste of time and money.

Hope it goes well! Thanks for contacting Crown. We invite you to listen to our Stewardship Podcast series; you will find many ideas on how to best manage God’s resources. Enjoy!

This article was originally published on The Christian Post on January 28, 2022

Dear Chuck,

My husband’s sales job has not produced good income since the pandemic. We’re in our early 60s, have $10,000 in a savings account, $25,000 in our 401(k), a paid-off home, and no debt. We’ve considered downsizing. Do you advise drawing down on our 401(k) now?

Managing Cash Flow

Dear Managing Cash Flow,

Unfortunately, for many who are in sales positions, lingering effects of the pandemic have caused inventory challenges, a decrease in demand, or a slow down in normal sales volumes in some industries. However, I think you have better options than turning to your retirement savings right now.

Rejoice in the fact that you are debt-free and in no immediate need of the money. If you can cut expenses and pick up some extra income, you may not need to draw down from your 401(k) at this point. If you have no other option, do not feel guilty about possibly borrowing some money to get you through a tough time. Do some deeper analysis with your husband on what I’ve suggested below, and then, consider my recommendations together.

Analyze Your Overall Picture

The fact that you have no debt and no mortgage gives you better options than depleting your retirement funds. How much income do you need per month to fill in the cash-flow gaps? This is the most important number to guide you in determining your best option.

Do you know what your home is really worth in today’s market? Seriously evaluate all available housing options: staying where you are, selling, buying something smaller, renting, or moving into a tiny house, an RV, or even a friend’s temporary guest house. Decide whether renting or buying is the best choice for you. Can you rent out your home for more than you could rent something else? Is it in an area that could produce Airbnb or VRBO income for you? Think creatively because a temporary move may be necessary until your husband regains stable income. More importantly, will downsizing relieve you of your income shortages long term? If not, don’t be too quick to downsize, as it is expensive to relocate.

How long does your husband plan to work? Have you or your husband considered temporary part-time work as a way to bridge the gap until his industry recovers? Do you have any other means of income? Have you looked for different jobs where his skills may generate more income?

When do you plan to start drawing Social Security benefits? What will your income/overhead look like when you get to that point? Since retirement is not too far away, it is better to think about building your 401(k) than shrinking it.

The rules for 401(k) withdrawals depend on the kind of account and where it is. Is it with a current employer or previous employer? You may be able to withdraw from your 401(k) based on your age, but you also may have to pay income tax on it. Check with your plan administrator. See if there’s an “in-service” withdrawal. Also, consider a 401(k) loan. See details here.

Alternative Stop-Gap Recommendations

Invite the Lord to Help

I know this is a stressful time for you, and it can feel very daunting to be short of funds for day-to-day expenses. Don’t panic; rather, see this as an opportunity to experience greater trust in the Lord’s faithfulness to show you which way He wants you and your husband to go. My wife and I have been through similar challenges a few times in our married life!

Pray with your husband every day, asking the Lord to show you His way forward. Be honest, transparent, and open to do whatever He may lead you to do. Ask a group of close friends to pray with you and for you. Remember God’s promises: “Again I say to you, if two of you agree on earth about anything they ask, it will be done for them by my Father in heaven. For where two or three are gathered in my name, there am I among them.” (Matthew 18:19–20 ESV)

Humbling ourselves before the Lord in the company of trusted friends opens the door for Him to do more than we can dream or imagine. We’ve seen it happen over and over. I am confident that this challenge will pass, and you will be in much better shape as you analyze your options, unite with your husband, and seek the Lord’s path forward.

You may be interested in some of our recent Crown Stewardship Podcasts; you will find much wise advice on managing resources for God’s glory. Thank you for writing. Keep us posted!

This article was originally published on The Christian Post on January 21, 2022