Dear Chuck,

A friend suggested we get a home equity loan to cover our daughter’s wedding this summer. This makes me very uncomfortable, but I want my daughter to have her big day.

Money for Matrimony

Dear Money for Matrimony,

I have a very wise friend that always responds to my questions with the same reply: “This is a question that demands some education!” What he is somewhat jokingly telling me is that he will explain the why behind his answer before he actually answers. Well, I sense the same opportunity with your question. I need to talk about home equity loans before I talk about financing your daughter’s wedding.

Understanding a Home Equity Loan

A home equity loan is a type of second mortgage. Funds are taken from the equity—the difference between the home’s value and the mortgage balance—and repaid over a certain period of time. For some, it is an easy and practical way to access cash. Equity is typically used for big expenses and can be more cost-effective than credit cards or personal loans with high interest rates. These loans average 6.36% compared to 15.96% for credit cards and 11.79% for personal loans (March 29, 2021).

Home equity fluctuates based on the market. Currently, home prices are climbing in much of the United States, but property values could plunge should we experience some catastrophic event. In 2007, home prices hit a high, then they steadily fell 35% by 2012.

A Motley Fool article at fool.com, “The Only 4 Reasons to Use Home Equity Loans,” approves these uses:

Not So Fast or Easy

I understand the first three as possible justifiable reasons; however, I do not recommend borrowing money to make any investment.

Michele Hammond, of Chase Private Client Home Lending, notes that applicants’ debt-to-income ratio, loan-to-value ratio, credit score, and annual income are checked. “Additionally, to determine the amount of equity in a home, a lender will employ an appraiser to determine the current market value of the home, which is based on its conditions and comparable properties in the area.”

If the money is used for home improvements, make sure they actually increase the home’s value and marketability. This website provides job cost and resale data for different regions of the country.

My Straight Answer

I don’t like the idea of using a home equity loan to pay for your daughter’s wedding. While you could pay for a nice experience for her, borrowing money puts your entire family at unnecessary risk.

Although a repayment plan must be in place for the loan, the same need for cash could arise in the future. Using the cash to cover debt or luxury lifestyle choices can compound a spending problem. Late payments could impact your credit score. Defaulting could mean losing your home.

Some Options

Do your homework to avoid the possible pain and stress of two mortgage payments. The pandemic has impacted the employment of many Americans. Analyze your income and employment situation, and put your pencil to the numbers to determine how much wedding you can afford without debt. Talk this over with your daughter.

When Jesus told a crowd (Luke 14:25-33) to consider the cost of discipleship, He gave an illustration: “For which of you, desiring to build a tower, does not first sit down and count the cost, whether he has enough to complete it?” This diligence and analysis is necessary for every big decision we face in life.

It is possible to do a cash out refinance. Rates are beginning to rise, but they may be lower than your current mortgage. Talk to several lenders, know all the costs involved, and pray for wisdom to determine if you should proceed. Seek counsel from those who understand the pros and cons.

Look at alternative ways to host the wedding that reduce the typical costs. Here are a few ideas: ask friends to help you crowdsource flowers, look for venues that are less expensive to rent, and seek volunteers for music, pictures, and even meals for the rehearsal and/or reception. Frugal weddings are nothing to be ashamed of. Years ago, I read a survey that weddings featuring low costs but a high number of guests produced longer lasting marriages than high cost weddings with fewer guests.

Be encouraged and patient. I am not sure how long you have before the big day, but disciplined spending and saving now can help you avoid borrowing. My hope is that this information will help you show the maximum amount of love and support to your daughter and future son-in-law, with the minimal amount of financial stress.

Want to Stay Connected with Crown?

I spoke about finding Renewed Hope in Crown’s Winter update; you can view the 15 minute video here. Join me for more encouragement during our Spring update on Renewed Faith on April 22nd. The virtual event is free, but registration is required, so sign up today.

Dear Chuck,

I am working hard to be better with money. What’s your best tip for getting out of debt?

Debt Free in Three

Dear Debt Free in Three,

I am excited that you have a goal to be debt free. I am hoping that your phrase “debt free in three” is a three year goal—or maybe even less—to pay off your debt. What I want to address is your first comment about wanting to become better with money.

Stewarding involves the heart and what we believe about God.

If all we ever do at Crown is get people on a budget, out of debt, or to have more savings in the bank, then we’ve failed because fixing our money problems is not the goal—our hearts need to be changed.

People can retire as millionaires and die as billionaires. But, unless they turn to God for the forgiveness of sins and the gift of new life, they will remain paupers—eternally separated from Jesus Christ.

How To Know the Lord

Man’s relationship with God was broken when Adam disobeyed the Lord. The guilt had to be punished; the debt had to be paid. In the Old Testament, Passover and sacrifices foreshadowed a future event in which God provided the perfect sacrifice, a Lamb without blemish—His only Son.

Jesus is God’s gift to us. We can’t earn salvation. We don’t deserve it. We can only receive it by humbly trusting the Lord and His grace.

“If we confess our sins, he is faithful and just and will forgive us our sins and cleanse us from all unrighteousness.” (1 John 1:9 ESV)

“If you declare with your mouth, “Jesus is Lord,” and believe in your heart that God raised him from the dead, you will be saved.” (Romans 10:9 ESV)

Our goal is not simply to help you get out of debt and on a budget. Our goal is to lead you to God so that you can know Him as Lord and Savior. Stewardship is born out of this relationship. When you know Him, you then want to obey what He teaches about finances.

A Long-Term Plan

True stewardship flows out of love and gratitude for what He gave. Faithful stewards don’t see their lives, money, and possessions as their own. They acknowledge that everything they have belongs to God, and they manage it accordingly. They desire to handle money wisely, to care for the earth and others, and to further God’s Kingdom. They don’t order their lives so that they can spend whatever they want. They order their lives so that God can spend them however He wants. They are thinking not just about how to get to the end of this life comfortably but also about how to prepare for the life to come.

Larry Burkett said, “Most Christians are more than content to live out their lives surrounded by the trappings of our world, rather than to risk losing them in becoming a radical Christian—one who will put God first in all decisions, even when putting God first is costly.”

In a few years, everything you have will either be thrown away or will belong to someone else—your house, your car, your clothing, your books, and all of your most prized possessions…everything.

Guard yourself from the material distractions of this temporary life, and focus your time and money on the eternal. You’ll only spend a few years here on earth. Our deepest needs can never be met with more things; they can only be satisfied with more of Jesus.

Debt Free in Three

I encourage you to continue your quest to become debt free. God wants us free from all earthly masters. He identifies financial debt as a form of slavery. More importantly, recognize that Jesus paid a debt that He did not owe so that you could be free of the debt you could not pay. That is the debt you owe for your sin. When you confess that Jesus Christ is Lord and surrender your will to obey His, you will be set free of your sin and shame and the penalty of eternal separation from God. You will be set free by the Father, Son, and Holy Spirit. This is the beginning point of your stewardship journey. It is the best advice I could ever give you.

Dear Chuck,

I’m getting nervous about the rising cost of gasoline because of my long commute each day. How can I avoid having my budget whacked?

Bring Back Cheap Gas!

Dear Bring Back Cheap Gas,

You have good reason to be concerned, but it is not all bad news. There are plenty of reasons not to panic. You have a number of good options that I will recommend.

Gasoline is Moving Higher… and Maybe Lower

Prices at the pump follow fluctuations in crude oil prices. California’s known for the highest prices in the nation. On March 16, the Orange County Register reported that the average price per gallon was $3.73, the highest in 67 weeks. One week later, it rose to $3.76, with premium at $4.108. Price comparisons by state can be found here.

On the 22nd, GasBuddy released a report entitled “Upward Gas Prices Broken as Oil Sags.” Although the national average gas price was 22.2 cents higher than a month ago, prices dropped slightly for the first time in 11 weeks. Patrick De Hann, head of petroleum analysis for GasBuddy, addressed the decrease.

“While gas prices still rose in a majority of states last week, we may see some price decreases in the week or weeks ahead, even as U.S. gasoline demand continues to rally to the highest level since the pandemic started nearly a year ago. It’ll be a bumpy road the next few weeks as markets sort out the bearish and bullish factors, but I still believe prices will likely experience more upward momentum ahead of Memorial Day.”

According to Trilby Lundberg, an industry analyst, prices are up due to higher crude oil costs, the February snow storm that shut down Texas refineries and reduced operations, and surging prices on credits for a renewable fuel.

In an NBC News article, De Hann said we have a supply and demand problem. “Covid decimated demand. It caused a lot of contraction and production cuts. 2020 set things back for U.S. oil production by several years.” Now that people are moving about, demand has increased, but production is short of where it was a year ago.

Sergio Avila, of AAA Nevada, says, “This increase isn’t something that is just isolated to the west. It’s something happening across the country. Every state average has climbed by double-digits since February resulting in 1 in 10 gas stations with pump prices that are $3 per gallon or more.”

Gasoline Prices Impact Us All

Jean Folger, at Investopedia, shares how gas prices impact the economy. Increased cost of transportation will be felt in:

Food prices go up as a result of more than just transportation. Farmers require diesel fuel to run machinery, and many fertilizers contain oil byproducts.

Gasoline prices impact spending and consumer confidence. A U.S. Gallup poll in August 2020 revealed that one’s view of the economy appears to be inversely correlated to the price of gasoline. Increases in state gas prices create pessimism about the economy.

How to Reduce Your Gasoline Spending

Many companies are now offering remote work since adapting to the challenges of COVID. Since you have a long commute, ask your employer to reduce the number of days that you need to drive into the office. Two of our employees with long commutes now only come into the office once per week. This has not only saved them gas money but also has improved the quality of their lives.

In addition, I recommend you plan your outings to reduce drive time and mileage. Remove any unnecessary weight in the vehicle, and make sure your gas cap seals properly. Skip premium gas, and use grocery store loyalty cards for discounts. Budget for increased gasoline prices when making vacation plans.

MoneyCrashers.com gives several tips to prepare for rising prices.

How to Reduce Your Stress

I often say that 90% of what we are worried about will never happen. The Lord reminds us not to use our time and energy to try and project the future.

“Therefore I tell you, do not be anxious for your life … But seek first the kingdom of God and His righteousness, and all these things shall be added to you. Therefore do not be anxious for tomorrow, for tomorrow will be anxious for itself. Sufficient for the day is its own trouble.” (Matthew 6:25-34 ESV)

Taking one day at a time means keeping your thoughts confined to the present. Yes, we should all do scenario analysis to prepare for and avoid danger, but we should also trust the Lord for right now.

One practice that I recommend is to verbalize all that you are certain about today. Make as long of a list as you can think of, and say it out loud. For example, I might say, “ I am alive. I am able to walk, see, hear, smell, taste, touch, and talk. I am free. Our nation is not under the threat of an invasion. I have friends and family who love me. I can afford gasoline today. I have a job! The Lord knows me. The Lord cares for me. The Lord promises to provide for me…” This will reduce your anxiety and bring your thoughts captive to enjoy what you do have and to praise the Lord for His goodness.

You are not alone in your feelings of concern about the future, which is why I recently spoke about finding Renewed Hope in Crown’s Winter update; you can view the 15 minute video here. Finally, I invite you to join me for more encouragement during our Spring update on Renewed Faith coming up soon on April 22nd. The virtual event is free, but registration is required, so sign up today.

Dear Chuck,

Do you think we are heading towards runaway inflation? If so, how should I prepare financially?

Inflation Fears

Dear Inflation Fears,

Any commentary on the state of the economy is like commenting on the water level in a river—it is an ever-changing dynamic. So, whatever is said is likely to be wrong within minutes, hours, or, certainly, days. In spite of this, general trends and specific directional observations may prove helpful.

Since inflation is on everyone’s mind, allow me to paraphrase Shakespeare’s character, Hamlet: “Inflation or No Inflation? That is the question.”

While economists and central bankers prefer a low level of controlled inflation, it is a very difficult scenario to achieve. Needed to create economic growth, inflation can negatively impact other areas, like the federal debt. Managing inflation requires the precision of a brain surgeon operating aboard a ship that is rocking back and forth in a stormy sea.

One thing I have learned about investing in public securities (stocks and bonds) is how emotion drives value from one day to another. Stocks drop with fear and danger, rise with optimism, and rotate with foreseeable trends. Investors shift in anticipation of economic winds. As Wayne Gretzky famously said, they are attempting to “skate to where the puck will be.”

The best way to answer your question is to give you the three prevailing viewpoints from very capable, professional investors. Here is the general spectrum on the topic of inflation: Yes, it is coming and fast; No, it is under control by the Fed; and It could go either way.

Dr. Michael J. Burry – Investor, Hedge Fund Manager, Physician; featured in The Big Short

A recent article explains that Dr. Michael Burry, in his recent tweets, spoke of current modern monetary theory policies with a quickly growing debt-to-GDP ratio along with more stimulus and the re-opening of the economy. He said, “…employee and supply chain costs (will) skyrocket.” He expects a market crash within months.

Warren Buffet – CEO of Berkshire Hathaway; considered one of the most successful investors in the world

In a current YouTube video, Buffet says, “The best businesses that will perform the best are the ones that require little capital investment to facilitate inflationary growth and that have strong positions that allow them to increase prices with inflation.”

Ray Dalio – Founder and Co-CIO of Bridgewater Associates; one of the top investment managers in the world

Dalio spoke at the opening panel of the Future Investment Initiative, saying, “We will see a rebound in growth and a rebound in inflation.”

Larry Fink – Chairman and CEO of BlackRock, the largest investment fund in the world

“I think we are going to have a huge amount of job creation, but all these elements are highly potentially inflationary,” Fink predicted. “It is fair to assume we are going back into an era of growing inflation.”

While businesses are already raising prices and seeing inflationary headwinds, the Fed disagrees. A recent Washington Post article says, “The Fed’s view is that the long-term forces keeping inflation low for the past decade and more are still at work, while the economy still has a way to go before completing its pandemic recovery.”

John Mauldin – Widely Recognized Financial Writer, Publisher, and Best-Selling Author

Mauldin says that the current bull market is a perfect cash-flow storm because of the following:

In a different, not-so-bullish article, Mauldin explains that he thinks we will see both inflation and deflation. He adds, “If we get even a modest recovery in the COVID numbers, we clearly could see some short-term ‘inflation’ in annual data… It won’t last… The debt burden will cap growth enough to keep the inflation mild.”

While difficult to predict, due to a number of factors, the majority of high-profile investors seem to think that inflation is imminent. As one article summarizes: “Increasing inflation can be caused by increases in the supply of money, increased access to credit, or demand that outstrips supply. In reality, inflation is usually caused by all or a combination of these factors.” Only time will tell.

To be prepared, be sure you are following these timeless investment principles:

Diversify – This means having investments in asset classes that can benefit from inflation, such as commodities and hard assets like real estate and precious metals, etc.

Get Debt Free –Your flexibility to adapt to a changing economy is improved when you are no longer shackled with debt, especially consumer debt like credit cards, automobile loans, and student loans.

Increase Financial Margin – If you spend less than you earn each month and increase your savings, you will reduce your stress, be in a position to navigate rising costs, and be able to take advantage of new opportunities.

Don’t Try to Predict the Future – The Bible makes it clear that no one knows the future. Many investors try to convince us that they do. Follow God’s financial principles, and stay the course.

“ Steady plodding brings prosperity; hasty speculation brings poverty.” (Proverbs 21:5 TLB)

This article was originally published on The Christian Post on March 19, 2021

Dear Chuck,

We just bought an older home and intend to remodel it. We hope to flip it within two years. We want to be prepared for the inevitable challenges. Do you have any tips besides building our emergency fund?

First-Time Remodelers

Dear First-Time Remodelers,

I hope this ambitious undertaking to remodel and flip your house for a profit is not driven by watching too much Fixer Upper or other home remodeling programs on HGTV. It is risky and more difficult than it looks on TV.

I have lots of advice from experience; in fact, I have more advice than I can write on this topic in this article! Hopefully, these crucial tips will help you achieve your goal.

Tip #1 – Prepare for the Unknown

Taking on a remodel, especially of an older home, is a venture into many unknown problems lurking behind the walls, under the carpets, or beneath the foundations! Plan on the likelihood of cost increases, time delays, and material shortages.

Tip #2 – Consult Experts

It sounds like this is a do-it-yourself project. All DIY projects are improved by learning as much as you can before you start. Read manuals and handyman books, and watch YouTube explainers. Recruit friends to share their expertise. If they already own the tools, you may save even more if they are willing to help. Trade your skills for theirs, or provide meals or yard work to pay them back for the help they bring to your project.

Get word-of-mouth referrals to find trustworthy contractors. Check their references and insurance coverages, and ask to speak with their most recent clients before you hire them.

Tip #3 – Conduct a Market Analysis

One of the biggest mistakes is to spend more money than you will ever get out of the house by over building in your market or making improvements that do not improve the value of your home. I have made both of these mistakes! It is painful. Once you know what you can market your house for, you can work backwards on your remodeling budget.

Tip #4 – Count All the Costs

“Suppose one of you wants to build a tower. Won’t you first sit down and estimate the cost to see if you have enough money to complete it?” (Luke 14:28 NIV)

Knowing you have the money to complete the job is step one. But, the cost of remodeling and flipping a house goes far beyond the financial. It takes a toll on your marriage, your ability to conduct your normal job, and your emotional health. Be sure you have counted all the costs before you start to demo anything.

Tip #5 – Maintenance and Repairs

Once the remodel is complete, an older home will need continual maintenance. According to one financial advisor, nearly 70% of his clients reject the idea of budgeting for repairs and maintenance. That’s a mistake that will eventually have consequences. The age and condition of your home, your climate, and the previous owner’s care will impact the amount of money you should budget for costs while living in your home. The Balance recommends the following calculations. Allow for more depending on your particular home.

Track your home maintenance and repair costs, and file your receipts. The total cost of owning an older home can be shocking. Any upgrades to energy efficiency of the home may qualify for tax benefits.

Tip #6 – Think Like the Future Buyer

Far too often, we remodel a home according to what we like or the styles that we prefer. That is fine if you plan to live in the home for years to come. Since you intend to sell your home in a short period of time, I recommend that you research the home styles preferred by today’s buyers. It may not be your style, but it will help you when it is time to put the home on the market.

As of the writing of this article, mortgage interest rates have begun to rise from historic lows. Don’t assume the market for selling your home will be the same two years from now. Be prepared to live in your home if you are unable to sell it.

This can be an exciting opportunity for your family to make some money on this project. But, it will be hard work. I know a couple who has done this on their first two homes where they have lived. It was very successful for them financially; however, by the third home they purchased, they did not want to think about fixing it up and flipping it again. They wanted home to be a place of rest, not stress. Thanks for writing.

This article was originally published on The Christian Post on March 12, 2021.

Dear Chuck,

I have several friends who are in deep financial trouble in the early years of their marriage. I want to avoid the stress they’re experiencing. Do you have any helpful tips so that I can guard my home and marriage?

Avoiding Disaster

Dear Avoiding Disaster,

Being under constant financial stress is terrible at any age, but it is especially dangerous in the “early years.” This is a time when most couples are vulnerable to separation and divorce.

I assume your friends are struggling with debt due to being unprepared for their lifestyle.

It usually occurs in a series of small mistakes, as a result of one huge accident, or because of the assumption that “this is just the way it’s done.” Since I don’t really know what happened to your friends, I will give you some financial advice and also some general principles so that you can avoid the five most common causes of debt.

Plan on financial disaster if you fail to plan for unexpected expenses. These are often things that have yet to come due or the unexpected costs of maintenance, repairs, or health issues. Anyone with a car, home, children, or pets understands this. Ignoring the inevitable or not working expenses into a budget creates credit card dependency. Adjust the budget to include setting aside money into an Emergency Account. Though temporarily uncomfortable, it is very wise long-term. It is best to have 3-6 months of your monthly expenses in an Emergency Fund.

If you are struggling with credit card debt now, contact our friends at Christian Credit Counselors. This should be done before you dig a deep hole.

Purchasing a home too early in marriage or paying too much for one creates problems. A house payment for the average family’s budget should not exceed 40% of net spendable income after giving and taxes. Include the mortgage, utilities, HOA fees, property tax, maintenance, and repairs. Destroying the budget to get into a home is not logical. It restricts the ability to give, save, and invest. Only purchase if the numbers work, preferably based on one income only.

If you cannot put 20% down before you take on a mortgage, it is best to rent and save until you can.

Most people look at the monthly payments for a car instead of the overall price. Interest translates into paying significantly more than the asking price and being burdened by the debt for years. Unlike a house, a car depreciates in value the moment you drive it off the lot. So, do not finance something that will lose money. Save, and buy reliable used cars with cash.

Disaster Proofing the Marriage

There is no silver bullet to protect “your home and marriage” from a disaster. Satan prowls around seeking to cause havoc in all relationships including the best marriages. Having your finances under God’s control is a sign of wisdom, and I highly recommend it. At the same time, let me give you a few tips that have helped us through the hard days.

Pray together, often. This took us years to get comfortable with, but it is now a way of life. Often, we take long walks and pray aloud together the entire time.

Seek to grow as Christ’s disciples. When you are both pursuing this goal, you will experience the fruit of the Spirit which is a glue to make any marriage even better.

Invite your spouse to be your most intimate, trusted advisor on all decisions. This trusting submission builds confidence and leads to better outcomes in all things as you work in unity.

Be humble, gentle, and quick to apologize. Nobody escapes hurting their spouse in a marriage. We can escape becoming indifferent about it through showing mercy, kindness, and grace when we are offended.

A good marriage is a financial benefit. A divorce is emotionally and financially devastating. My wife and I wrote an entire book on the topic of money and marriage, called Money Problems, Marriage Solutions. It is a step-by-step guide to growing in unity. You can get your copy here.

I made many of the mistakes that you are hoping to avoid. By God’s grace, He kept our marriage together, and we worked through the mistakes. Today, we are in a much better place and stronger because of our ability to work together. There is always hope when you fully trust Him and apply the principles of God’s economy.

This article was originally published on The Christian Post on March 5, 2021.

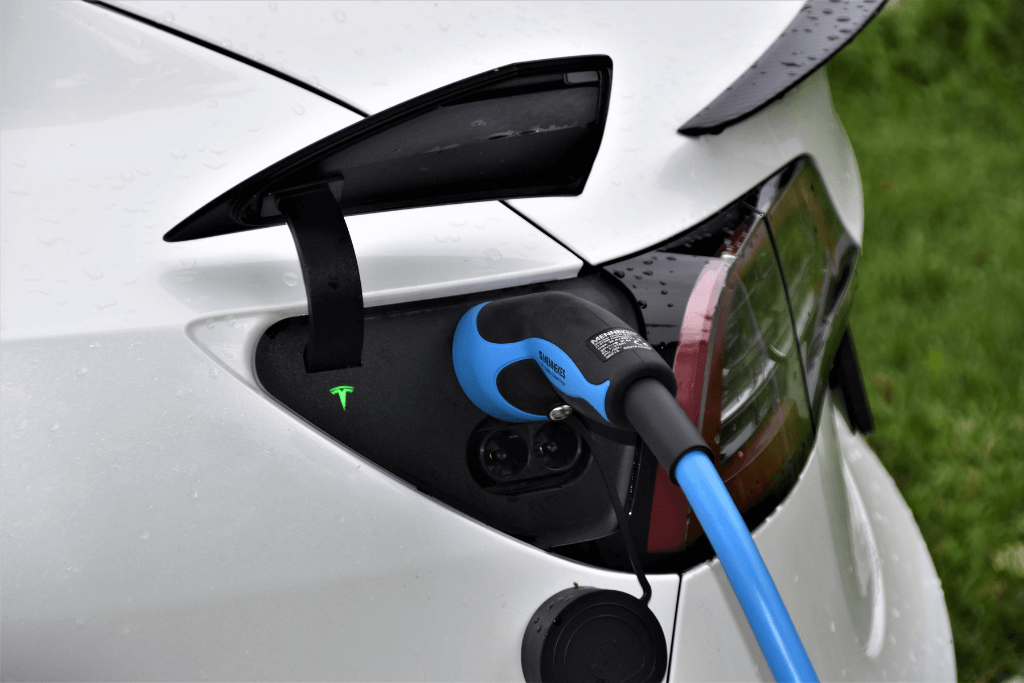

Dear Chuck,

I need to replace my car this year. I’m trying to decide if I should buy an electric vehicle or not. What would you do?

Car Choice

Dear Car Choice,

This is a timely question as a great deal of policy is attempting to move us towards electric vehicles with the assumption that it is “clean energy” and good for the environment. Let’s get some context first; then, I will give you my recommendation.

The Push for Electric-Powered Cars

Governor Newsom of California wants to ban cars with gasoline engines by 2035, and President Biden hopes to replace the government’s fleet with electric vehicles.

Tesla, the leading manufacturer of electric vehicles, is now worth about as much as that of the nine largest car companies in the world, combined! Obviously, investors believe this is the wave of the future. This is not an endorsement of the stock, by the way.

Electric vs. Gasoline-Powered Cars

It is important to research and understand the costs of time and money before making any purchase. “For which of you, desiring to build a tower, does not first sit down and count the cost, whether he has enough to complete it?” (Luke 14:28 ESV)

One of my friends bought a new, high-end Tesla and loves it. He calls it the “iPhone of cars” because of its ease of functionality and its superior performance compared to all other electric vehicles. Of course, he spent $75,000 for it, which is far more than I would ever want to pay for transportation. By the way, Apple is looking to enter the market if they can find a willing partner to create “autonomous (self-driving) cars.”

Nerdwallet proposes several questions to think about before purchasing an electric vehicle.

Can you afford one? How far do you need to drive on a single charge? Where will you charge it? What will you use it for? Do you enjoy performance?

In addition, I’ve gathered some pros and cons to consider.

Pros

Cons

Some Facts To Consider

Most electric cars are able to go more than 200 miles when fully charged, but that is still much less than gasoline powered cars. Tesla’s Long-Range models can go over 300 miles, but the cost is significant for the longer-lasting power supply. Plug-in hybrids have a combined gasoline and electric range of 400 to 550 miles. However, air conditioning, heat, and hills can reduce that number.

Charge times vary. Currently, the cheapest and most convenient option is to do it overnight at home. Fast chargers are spreading throughout the country, but they still take longer than refueling at a gas station. Plus, the cost will fluctuate with the cost of electricity. To drive across the country, you have to map out your stops in advance by locating the charging stations and including downtime for charging, which is much longer than refueling gasoline.

Hybrid vehicles have experienced significant depreciation. Be sure to research depreciation of an electric vehicle. Some early models have not done well in the after market.

At What Cost?

Base prices range from $30,000 for the Hyundai Ioniq and Nissan Leaf to six figures for some Tesla and Porsche models. Home charging units cost under $1,000, with rebates available in some states. Some question whether or not our power grid has the capacity to keep millions of cars charged each night.

In addition, there is another cost to consider. Battery manufacturing is water-intensive and pollutes air, soil, and water. Lithium and cobalt are needed to make rechargeable batteries. With increased production of electric vehicles, there will be negative ecological and human issues to consider.

In January, The Guardian reported that 60% of cobalt comes from the DRC (Democratic Republic of the Congo) where men, women, and children are miners. Unregulated mines and contaminated discharge is life threatening. The Lithium Triangle of South America (Chile, Argentina, and Bolivia) has experienced groundwater depletion and the spread of deserts. In Tibet, a leak from a lithium mine poisoned a local river. According to the UN, an electric car boom will result in devastating ecological side effects.

Consumer Reports provided much of the information for this article. For additional interesting statistics regarding electric vehicles, see this website.

To Buy or Not to Buy?

In spite of the potential of electric cars, I plan to drive my good, used gasoline-powered cars as long as I can, while observing what happens within the auto industry. I expect the cost to purchase battery-operated cars to come down and the overall performance to improve, with more and more technological advances in the near term.

Speaking of gasoline-powered cars, I recommend that you buy a used car, paying cash for one that will hold its value. The world will sell you lots of reasons to buy a new car, but, remember, a car is simply a way to get from point A to point B. Driving an older, reliable car can be an excellent financial decision in addition to keeping you humble.

Hope that helps!

Originally published on The Christian Post on February 26. 2021

Dear Chuck,

My 13-year-old wants a credit card since her best friend has one. Seems young to me. Would you say yes or no?

Credit for Kids?

Dear Credit for Kids,

My first reaction is, no! However, it has some potential upside, so let’s vet this a little closer.

Far too many young people are learning how to be consumers and not producers. In other words, they become expert spenders but have not been taught how to generate income.

Setting that aside, this credit card idea has some possible benefits.

Upside

Giving your teen a credit card is an opportunity to teach responsibility and restraint. Ideally, no child should leave home without understanding Biblical stewardship. Knowing how to manage God’s property impacts one’s eternal destiny. If a credit card can reinforce that, welcome it.

Why Make Your Teen an Authorized User on Your Card

Authorized users are dependent on your credit history to build theirs. If you have good credit, it will show up on their credit report. Adding your teen to your card has the potential to:

Different cards have different age requirements for cardholders. There are starter cards for college students or those with no credit which can be opened in their own name if 18 or 19 years old. If younger, they can be added as authorized users on a parent’s card. Look for no-annual-fee cards, and be aware that some charge fees to add authorized users.

Making your teenager an authorized user on your account while teaching him/her wise use can build a positive credit history for him/her. Timely payments, low credit utilization, and the age of the card will be added to the teen’s history. Good credit will prevent the need for co-signing in the future, which the Bible warns against anyway. The Balance states the following reasons for teens to build credit:

Guidelines

A teen who is mature and teachable will welcome the responsibility you give him/her. It demonstrates your trust, which will boost his/her self-confidence and the desire to handle a card wisely.

Before having a card, teens should have a checking account. Knowing how to write checks or make online payments, keeping their check register up to date, and balancing the checkbook monthly will help them understand the connection between cash and credit. Have them write the check or make online payments for their monthly spending.

Teach them how a credit card works, how it affects their credit score, and the financial consequences of not paying in full each month. Explain the dangers of losing one, not keeping track of spending, and exceeding limits. Give them a credit limit, and show them how to keep track of spending. Require them to cover specified charges. This will vary among families depending on the maturity level of the child. They must guard the number and never share it with friends. Check their credit score periodically, and celebrate their good work.

Have a plan in place should they overspend. Give them the opportunity to work for you, to pick up extra work somewhere, or to sell something of value. Bailing them out will only weaken their resolve to be responsible.

Warnings

Credit card debt is a problem for many. If you struggle with it, please do not give your teen a card until you get your finances in order. Use your situation as a teaching tool for your teens. They may be the encouragement you need to systematically pay off your debt.

You are legally responsible for any authorized users. If the card is mishandled, your credit score and theirs can be negatively affected. Text message alerts for charges can be helpful.

If you prefer that they not have access to your account and its credit limit, then apply for a new card, and set a low credit limit for their use. Then, continue using your original card for your daily-use. Should they lose their card, it can be canceled immediately and replaced, without disturbing your primary card.

Resources

Training young people in the proper use of credit will prepare them to be wise stewards.

For a list of recommended credit cards for teens, check out Credit Karma and Wallet Hub.

For help teaching, see ThePennyHoarder.com, Credit cards 101, and How to Use a Credit Card.

Stress the importance of being a manager of all that God provides, and set before them the goal of hearing the words: “Well done, good and faithful servant.” Crown offers several courses that may be of benefit to you. Your Life: Financial Stewardship for Teens is one such course. You can find it as well as many others at www.crown.org.

This article originally published on The Christian Post on February 19, 2021.

Dear Chuck,

I was laid off because of COVID. My company may rehire me soon, but I am thinking of getting out of the travel industry completely. Should I wait it out or move on?

Stuck in Unemployment Land

Dear Stuck in Unemployment Land,

I am sorry that you are feeling stuck. Having been laid off twice in my life, I understand the dilemma you face. Let’s start with the big picture and, then, get practical.

The job market has been affected, if not permanently changed, as a result of COVID. But, the dynamic change is being led by many other factors. In 2018, the World Economic Forum reported that automation, robotization, and digitization would impact the workplace. So, it is important to prepare yourself for what lies ahead, regardless of whether you’re unemployed or are considering a career change.

According to CareerBuilder.com, a few trends are obvious:

Get Busy

View your job search as a full-time job. Currently, there is actually an upside of unemployment, but it is your responsibility to maximize this time. Do not expect others to do it for you. Avoid the temptation to fall into bad habits or squander time during this period of unemployment. Invest in yourself. When a professional athlete gets cut by a team, he/she still has to stay in shape and strive to improve in order to win a spot on another team. Keep that in mind.

Read, study, and research. Then, gain the necessary skills to make yourself more valuable and, thus, attractive to potential employers.

The best investment you can make is in your gifts, talents, and professional abilities. Develop a daily schedule, and set deadlines while working toward specific goals. Take time to clean up your social media. It is almost as valuable as a resume in today’s world.

A Career Direct assessment could help you get to know yourself. You’ll gain an understanding of your personality, skills, interests, and values. We have coaches to help you find a new direction should you decide not to wait out the time to potentially be rehired.

Find a mentor who will be direct while offering encouragement, accountability, and guidance. Think through your relationships at church, with family, in the workplace, or in your neighborhood. Ask the Lord to direct you to the right person.

Some Practical Tips

Next Avenue recommends the following job search tactics:

Build hard skills with courses, certificates, and degrees online. Coursera offers training from leading universities and companies.

Don’t Overlook Soft Skills

Develop your soft skills as well. These are more personality focused and are highly underestimated. A study at MIT Sloan revealed that training in these skills grants a substantial return on investment to employers, while it also benefits employees. Communication, leadership, time management, problem-solving, adaptability, positivity, learning from criticism, and working under pressure are essential in being able to interact well with others.

The top five soft skills cited for 2020 by Business.linkedin.com included creativity, persuasion, collaboration, adaptability, and emotional intelligence. Different companies offer training. Udemy offers 130,000 courses online with a special division for Soft Skills development.

Mind the Gap

There are several reasons to consider a temporary job. Besides providing income and relieving despair, it keeps you productive. It can fill in gaps in your resume, allow you to explore a field that may prove to be interesting, and even be a step to a job you love. A temporary job provides the opportunity to develop new skills while broadening your network. It will give you some understanding of a position before committing to it full time.

Work can be a positive witness for the Lord or a negative one. Give it your all, exercising common sense, diligence, and excellence. Set yourself apart by striving to do your very best.

“Whatever you do, work heartily, as for the Lord and not for men, knowing that from the Lord you will receive the inheritance as your reward. You are serving the Lord Christ.”

(Colossians 3:23-24 ESV)

We are all hoping for the economy to be fully open soon. Yet, the travel industry may be the one most affected in the short-term. My advice is to get an interim job, pursue new opportunities, and wait on the Lord to show you where He wants you to work. Let us know if we can help.

Dear Chuck,

Can you explain what happened with the GameStop fiasco this week? It is very confusing to understand why it was such big news.

Shocked by GameStop

Dear Shocked by GameStop,

Like you, I was stunned by the hysteria to own shares of this seemingly small, struggling retailer called GameStop. It was certainly never one on my personal radar as a choice investment opportunity.

The saga of what happened as the stock soared from $40/share until it peaked at $468/share within one week will go down in the annals of Wall Street history. It turned out to be the biggest “short squeeze” in the past 25 years.

To explain it simply, an angry mob of small day-traders decided to try to injure the largest hedge fund on Wall Street. It was the classic “little guy vs. big guy” fight. Billions of dollars were lost (by most everyone involved) as this extraordinary event unfolded.

My understanding is that a box-office movie is already being planned to showcase what some are calling an uprising of “the ants vs. the elephant” in a life or death battle.

There is a lot to learn from this incredible story, especially in regards to the biblical principles of investing.

Some Background

GameStop bills itself as the world’s largest retail gaming destination for Xbox One X, PlayStation 4, and Nintendo Switch games, systems, consoles, and accessories. They also sell gamer-centric apparel, collectibles, and more. However, the company was clearly struggling. They once operated nearly 6,000 stores worldwide, but the move to online gaming was hurting the company badly. They closed 600 stores in 2019, and by September of 2020, they announced they would be closing another 450 stores due to the strain placed on the company by COVID. The publicly traded stock under the symbol GME fell to $4-$7/share during that time.

Identifying the Key Players

It is important to understand how this epic financial struggle between the so-called “little guys” and the “big guys of Wall Street” developed. Let’s identify a few of the key players:

If we go much deeper, it will only get more complicated. For now, this will help set up the main point of what happened.

The Story

Melvin Capital and a number of other hedge funds took a short position in GameStop/GME, which means they were betting that the company would fail. This is perfectly legal, but some accuse hedge funds of using their power and connections to help accelerate their desired objective, thus hurting all the “little guy investors” who may be betting that the company does not fail.

Some astute day traders noticed that the hedge funds had over-shorted their positions, and the potential for a “short-squeeze” was possible if they could drive up the price of the stock. It was a clear opportunity to make an investment out of revenge to cause Melvin Capital massive losses. The rallying cry was to make a YOLO trade, which means “You Only Live Once.” The idea was to throw off concerns about one’s money and make the big guys lose, for once in a lifetime. Millions of small investors did just that. Using their Robinhood app, many day traders shrugged off the risk and bought GME shares for the joy of “putting it to the big guys.”

Melvin Capital and others lost billions of dollars on their short positions as the stock soared against all logic. However, after reaching the incredible overvalued price of $468/share, self-interest overruled mob justice, and millions of the “ants” began rushing to sell their stock. The price plummeted as small traders experienced the pain of owning shares in a company that was wildly overvalued. Now, their personal losses mounted.

What to Learn?

The irony of the entire story is the name of the company that found itself at the center of this dramatic, high-stakes game of poker: GameStop. Millions were mobilized to think of investing as a game. The painful losses will hopefully forever remind them to, indeed, stop.

“For the love of money is a root of all kinds of evils. It is through this craving that some have wandered away from the faith and pierced themselves with many pangs.” (I Timothy 6:10 ESV)

Events like the GameStop frenzy can be unsettling, which is why I recently wrote Seven Gray Swans: Trends That Threaten Our Financial Future, where I discuss global trends that have the potential to shake up our world, economy, and stock market. By preparing wisely for these “gray swan events,” we have the opportunity to be salt and light to the world should they occur.

This article was originally published on The Christian Post on February 5, 2021.