Dear Chuck,

I am a young investor and need advice. Bitcoin looks like a great investment. Is now a good time to start investing in it?

Bitcoin or No Bitcoin?

Dear Bitcoin or No Bitcoin,

Before you make the decision to “invest in Bitcoin,” be sure you understand the risks. People are buying Bitcoin with the hope of making big money without fully considering the big risks. While it is the leading form of cryptocurrency in the world right now, most of the people I respect consider it more of a wager than an investment. They look at it like buying a lottery ticket in that it may be a big winner or loser.

Early in January, Britain’s Financial Conduct Authority warned crypto traders to be prepared to lose all of their money. “Consumers should be aware of the risks and fully consider whether investing in high-return investments based on crypto assets is appropriate for them,” the article states. There are two key issues: volatile prices and no guarantee that digital currencies can be converted back into cash.

Crypto Currency?

Some perceive Bitcoin as inflation protection while serving as an alternative to gold. But, Nouriel Roubini, professor of economics at NYU’s Stern School of Business, strongly disagrees. He argues, “First of all, calling it a currency – it’s not a currency. It’s not a unit of account, it’s not a means of payment…it’s not a stable store of value. Secondly, it’s not even an asset.”

According to Roubini, Bitcoin has no intrinsic value because it does not provide income, capital gains, or some form of utility like bonds, stocks, real estate, or precious metals do. It is purely speculative. He further explains that academic research suggests that the “pseudo stable coin Tether has been created by fiat and is …used literally to manipulate the price of Bitcoin.”

Crypto Volatility

Bitcoin peaked above $41,900.00 on January 7th. Then, prices began dropping. Reuters reported on January 19th: “Nearly 90% of respondents in Deutsche Bank’s monthly investor survey said financial markets now had a number of price bubbles, with cryptocurrency Bitcoin and U.S. tech stocks top of the list.”

On January 21st, Bitcoin fell 11%. Two things happened. During Janet Yellen’s confirmation hearing, she suggested that lawmakers curtail Bitcoin use because of its association with criminal activity, including terrorism. In addition, “double spend” was thought to have occurred. It is a feared flaw in which someone can spend the same Bitcoin twice. In reality, two blocks were mined simultaneously. But, confidence was shaken.

The Financial Press addressed the price drop as well. Scott Minerd, with Guggenheim Partners, claimed that prices may fall back to $20,000 despite the fact that several weeks ago, he forecasted a price of $400,000. However, Michael Saylor of MicroStrategy says Bitcoin could reach $14 million.

Volatility is clearly evident. Manipulation, regulation, fear, and greed are only a few of the factors playing into it. On January 26th, at 10:00 a.m., Bitcoin was up to $31,320.90. BlackRock, the world’s largest asset manager, authorized two funds to invest in cash-settled Bitcoin futures. Marathon Patent invested $150 million on the 25th. Who will be next?

Crypto and Electricity

Creating Bitcoin requires specialized hardware called Application Specific Integrated Circuit (ASIC). They are large and require a lot of electricity which gives incentive for companies to establish locations where electricity is cheap.

There is a growing concern about the centralization of mining. China supposedly accounts for 50-65% of the mining. Cheap electricity, inexpensive labor, and proximity to ASIC manufacturers are driving this. According to an article on Bitcoin.com, the Iranian government is blaming power shortages and rolling blackouts on Bitcoin mining. “Police in Iran have reportedly seized 45,000 bitcoin mining rigs for illegally using subsidized electricity from the state,” the article states.

Defenders claim renewable energy will make mining more affordable. Others claim it is far less expensive than mining gold.

Crypto Opportunity?

Some find price drops as opportunities to buy. Bitcoin magazine reports that over $30 billion has been accumulated for the long term: 2.814 million Bitcoin or 15.16% of the total in circulation. Supposedly, less than 15% is actively traded. The majority of people are accumulating, not trading.

Others see a correction as a case for creating a Bitcoin exchange traded fund (ETF) that would allow for smaller trading sizes. An ETF is a basket of securities that is listed on exchanges and traded like stock. ETF share prices fluctuate with trades being made throughout the day, while mutual funds trade once after the market closes and not on an exchange.

Invest or Pass?

Frances Coppola, at coindesk.com, has an interesting take on the topic.

So the faith of bitcoiners is what gives bitcoin its value. If they were to lose that faith, the currency’s value would fall to zero. But, is their faith alone enough for bitcoin eventually to replace the U.S. dollar as global reserve currency?…The sort of social and political collapse that would destroy the dollar would surely also destroy global civilization.

What does the Bible say?

“Do not toil to acquire wealth; be discerning enough to desist. When your eyes light on it, it is gone, for suddenly it sprouts wings, flying like an eagle toward heaven.” (Proverbs 23:4-5 ESV)

“As for the rich in this present age, charge them not to be haughty, nor to set their hopes on the uncertainty of riches, but on God, who richly provides us with everything to enjoy. They are to do good, to be rich in good works, to be generous and ready to share, thus storing up treasure for themselves as a good foundation for the future, so that they may take hold of that which is truly life.” (1 Timothy 6:17-19 ESV)

My view is that there are better, more stable opportunities to begin your investment experience. If you think you want to own Bitcoin, start small, be in a position to lose it all without regret, and diversify.

This article was originally published at The Christian Post on January 29, 2021

Dear Chuck,

I don’t think I have ever felt more uncertain about America’s economic future than I do now. Do you see any light at the end of the tunnel? My anxiety levels are growing!

Anxious American

Dear Anxious American,

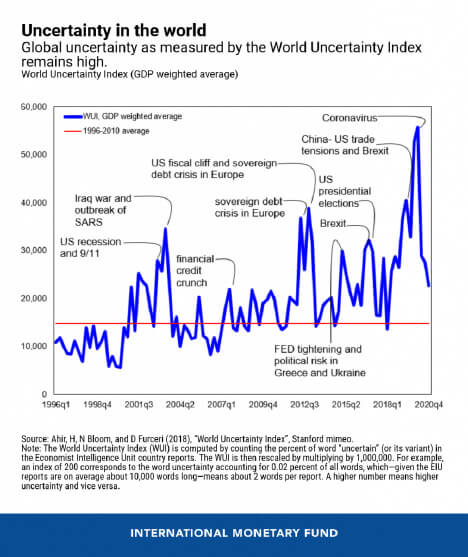

Your question prompted me to see if there was some measurement of the sense of uncertainty that so many of us are feeling and I found one! The International Monetary Fund published a graphic of the “World Uncertainty Index” in context over the past twenty-five years. The interesting takeaway for me is that the index peaked with news of the Coronavirus but has decreased by about 60% since the middle of last year. Take a look:

The point is, you are not alone. The world is in a history-making shift right now and most of us are experiencing greater levels of concern and anxiety.

Dealing with Our Unknown Future

If we focus our minds on all of the uncertainty we are truly in right now, it will no doubt breed anxiety. Financial anxiety begins when we start projecting how our future will be impacted by current events. Not knowing if our needs or expectations will be met creates worry. Dwelling on the unknown can propel us into a vortex of hopelessness. Doubt, disbelief, and negativity will eat away the peace and confidence that God wants us to experience.

In July of 2020, AnxietyCentre.com released an article with data and facts worth reading to get an idea of how serious this issue is. It states:

According to The Economic Burden of Anxiety Disorders, a study commissioned by the ADAA and based on data gathered by the association and published in the Journal of Clinical Psychiatry, anxiety disorders cost the U.S. more than $42 billion a year, almost one third of the $148 billion total mental health bill for the U.S.

Anxiety can raise its ugly head concerning health, money, education, careers, family, on and on. However, this is not new to humanity. An idiom came into use in North America during the mid-1800s. You’ve probably heard some form of it: “don’t borrow trouble.” Worrying solves nothing. It wastes time and energy and distracts us from more important things. Most of what we worry about never happens and reveals our lack of trust.

That idiom is nothing new. The Bible addressed the issue centuries ago:

Because we cannot know the future, we will always be prone to experience financial anxiety if we dwell on all the “what if” scenarios that race through our minds. Here is a simple framework that may help. When financial anxiety is rising, remember S.O.S. Stop. Organize. Start.

Stop!

If you are overspending, accumulating debt, and living with financial stress to make it to the end of the month, declare that you will stop repeating those mistakes now. This is the first step in gaining financial wisdom that will reduce your anxiety. Stopping is progress!

Humble yourself and recognize your need to place full confidence in the Lord. Repent of mishandling the money He entrusted to you. Don’t blame others or beat yourself up. Simply agree that you want to discontinue old bad habits with your finances.

Organize!

Make a plan to repair the problems you have created. They will not disappear by winning the lottery or ignoring them. Get help and seek training to address your issues and establish goals.

Begin a process to right the wrongs. Ask the Lord to help you persevere through this step with discipline, self-control, and hope. This will reduce your anxiety even more. God promised that we will experience tribulations and storms but He will never leave us or forsake us.

Start!

Once you have stopped and organized, you are two-thirds of the way there. God wants you to start doing what is good and faithful with money. His goal is not that we simply have freedom, but that we use money for His purposes, not our own.

It can be helpful to find wise mentors and gain knowledge from others who can guide and encourage you. Prioritize your life around the basic principles of giving first, saving second, and living on the rest. Restructure your lifestyle within a defined budget and renew your mind daily.

Light at the End of the Tunnel

I truly do not know what lies ahead, although I enjoy watching trends and keeping up with events that threaten our financial future. I just released a new book called 7 Gray Swans where I discuss many of these trends. I also know that there is always a reason for hope. Most of what we worry about will never happen. If it does, God will work it together for our good. We can find His Light shining brightly, no matter how dark our circumstances may seem.

We offer a variety of online courses and other resources to ground you in Biblical financial principles and fortify you for the days ahead. Christian Credit Counselors can help you eliminate credit card debt. Their Christ-centered values and experienced team of professional counselors can help you overhaul your finances. That step alone will reduce your anxiety.

Pray for our nation. We are in a turbulent time. We need you and all believers to be the salt and light that Jesus created us to be for such a time as this.

This article originally published on The Christian Post on January 22, 2021

Dear Chuck,

Is America heading towards an economic collapse? If so, how do I prepare?

Worried Boomer

Dear Worried Boomer,

My view is we are headed towards another economic crisis with a low risk of an actual economic and/or currency collapse. In either scenario, there are ways to be prepared.

Economic Crisis vs. Collapse

An economic crisis is different from a collapse. America has worked through several in my lifetime: ‘70s stagflation, ‘81 recession, ‘89 savings and loan crisis, post-9/11 recession, ‘08 great financial crisis, and the 2020 coronavirus crisis we are in now. A collapse is brought on by a complex set of factors that must merge simultaneously but at its very core is a devastating interruption in economic output and/or a loss of confidence in a currency.

In an article for Investopedia, Sean Ross explains, “The root of any collapse stems from a lack of faith in the stability or usefulness of money to serve as an effective store of value or medium of exchange. As soon as users stop believing that a currency is useful, that currency is in trouble.”

The advantage America has is that no other nation has the vast diversification of economic output nor presents a viable alternative to the stability of the U.S. dollar….yet.

The two warning signs of a possible collapse are (1) high unemployment and (2) runaway inflation. Essentially, this is when there are not enough jobs for the economy to grow and too much worthless money being pumped into the economy.

Reasons the Dollar Could Collapse

What Would Happen?

Panic would ensue because it would happen quickly. Demand for the dollar would drop dramatically along with U.S. Treasuries. Interest rates would increase. Hyperinflation would occur as investors would turn to other currencies. The dollar would decrease in value and prices would jump.

A collapse would be cataclysmic in the damage and disruption it would cause to not only our lives but to the rest of the world. Imagine how your life might be affected if banks and ATMs suddenly closed, you had no access to credit, there were limited supplies of groceries, gasoline, and other essentials, paired with an increase in civil unrest and crime. These scenarios would impact the postal service, transportation, education, health care, etc. Survival in this kind of environment for any length of time would be difficult.

We have many contemporary examples to learn from with varying degrees of damage: Germany, Argentina, Iceland, and Zimbabwe have all suffered a currency collapse. Of course, none of those nations have the size and stature of the U.S. dollar so a similar event in this country seems unimaginable, but it is not impossible.

How to Prepare?

Solomon commented on this back in ancient times. In Ecclesiastes 11:2 he advises us to diversify into seven or eight differing assets while in Ecclesiastes 11:6 we are advised to have multiple sources of income.

Ask yourself if your career provides an essential service. If not, consider changing or getting certified in areas that would give you greater job security. This is important to remember when preparing your children for their future.

The Bible warns us repeatedly to avoid enslavement and compares debt to being like a slave. You can weather a crisis or a collapse with less stress and greater flexibility without debt.

Gold and Bitcoin represent an alternative to the U.S. dollar. When fear or volatility begins to rise, the price of these alternatives also rises. But these are not the only options to hedge against a crisis or collapse. Real estate, equipment, commodities, and precious metals are also favorable investments during a time of turbulence. There is not one single option that will always protect you; that is why diversification is essential.

Seat Belts, Not Parachutes

Brad McMillan at Forbes believes doomsayers are coming out of the woodwork. He says, “Volatility in a currency’s value does not mean the currency will collapse any more than a drop in Amazon’s share price means the company is going away.” In July, he said we would see a collapse coming long before it happens but did not believe it was coming soon.

I want the body of Christ to be prepared if and when a crisis/collapse occurs. In my new book, 7 Gray Swans, Trends that Threaten Our Financial Future, I discuss the economic trends that concern me and the present challenges we face such as Universal Basic Income, Modern Monetary Theory, and a cashless society, among others.

Taking precautions now is like wearing a seatbelt in a fast-moving car or airplane. It makes sense. However, I do not believe it is time to look for the parachute!

This article was originally published on The Christian Post on January 15, 2021

Dear Chuck,

I did not grow up in a home that gave generously. My wife did. She (and the Lord) are convincing me to make it a priority. Can you help me get a better understanding?

Holding On for Retirement

Dear Holding On,

Well, you sure sound a lot like me about 20 years ago! I happily donated 2.6% of our gross annual income each year and I was content with that. That was the national average at the time, by the way. When my wife pleaded with me to give more, I had lots of ready rebuttals to prevent it from happening. So let me say up front, I was wrong, and my, how God has wonderfully transformed my heart on this topic!

Giving has become a deep source of joy for us. Now, it is even our tradition, as a couple, to spend a few hours the last week of December to total our giving for the year and seek ways to give more. We try to surpass what we gave the previous year. My only regret is that it took several decades for us to get to this point. I hope you don’t make the same mistake I did.

The Surprise Gifts

One Christmas, Ann and I were broke and unable to buy our two young boys the Christmas presents we really wanted to give them. I remember feeling frustrated and depressed about it.

Meanwhile, God moved in the heart of another family of modest means that we knew at church to bless us. But not just any family. Earlier that year, the oldest of their two sons was tragically killed in a freak accident on the day of his high school graduation. He had a bright and promising career ahead of him both as a student and an athlete. His parents were devastated by the loss. Little did we know that the money they had saved for their son’s Christmas gifts would instead go to supply for our two sons. We will never forget our shock and the love we felt for them through those gifts for our boys. We were so grateful to have presents under the tree but it was their unexpected generosity that ended up being the greater gift to us. They set a beautiful example of granting hope to others through giving. Since that time, we have had opportunities to give that have stretched us and blessed others in ways we could never have imagined.

We Are All Generous

Todd Peterson, a friend and former NFL kicker, came up with my favorite quote about generosity. He said, “We are all generous…Nobody has to teach us anything about being generous. The challenge we face and the choice we must make is, are we going to only be generous towards ourselves or are we going to be generous towards God?”

It’s a matter of breaking the habit of self-generosity. A lifestyle of giving makes you think before you buy something. You have to consider whether you really need it while others are truly in need. God wants us to direct that generosity towards Him, to be “rich toward God” instead of ourselves, so we will share what He has provided for us.

Our founder, Larry Burkett, once said, “My greatest fear in life is standing before the Lord and hearing Him say, ‘I had so much more for you, but you held on too tightly.’”

When we choose to obediently follow biblical financial principles, giving becomes our highest priority. Oftentimes, God supplies our needs in unexpected ways, allowing us to give more generously. Eliminating debt frees up funds to share with others. When we give with no expectation of anything in return, we are the ones rewarded.

Benefits of Giving

Barriers to Giving Generously

FidelityCharitable.org suggests ways that charitable giving can help with tax planning.

Ask the Lord to Open Your Eyes

Besides supporting your church and organizations dedicated to building the kingdom, make it a goal to serve together as a family to help others in 2021. There are needs everywhere. People are hurting and often too embarrassed to admit it. Your attention encourages and grants hope to the receiver. We became aware of that fact in our very own neighborhood. Couples have pulled together to help a precious soul who was hurting so badly she couldn’t even help herself.

The Apostle Paul told the Ephesians, “In all things I have shown you that by working hard in this way we must help the weak and remember the words of the Lord Jesus, how he himself said, ‘It is more blessed to give than to receive’” (Acts 20:35 ESV). I now know this for a fact!

Don’t worry about your retirement; rather focus on that day that you will stand before the Lord and be evaluated for your stewardship. I agree with your wife; make giving a top priority and you will never regret it.

This article originally published on The Christian Post on January 8, 2020

Dear Chuck,

My husband and I really need this to be the year for a financial turnaround. What are the best practical steps we can take to achieve this in the new year?

PTL it is 2021!

Dear PTL it is 2021,

Happy New Year! We join you in thanking God for another year! It is a time to start fresh and pursue our God-given purpose. Improving your finances is a fantastic goal for any couple and I have practical advice to help you.

“Unless a particular man made New Year resolutions, he would make no resolutions. Unless a man starts afresh about things, he will certainly do nothing effective.”

– G.K. Chesterton

The last sentence is so true. Nothing effective is accomplished unless we purpose to achieve something new!

If you and your husband sincerely want to make financial progress and are willing to commit to a plan, here is the most simple and sure way to do it: Give first. Save second. Say it to yourself, write it on post-it-notes, shout it out loud, make it your mantra for 2021, and put it into practice starting today!

Give First

“Honor the Lord with your wealth and with the first fruits of all your produce.” (Proverbs 3:9 ESV)

Step 1: Give a portion of everything that you receive. Make it your absolute first priority and do not compromise.

God wants to conform us into His image. He does that by asking us to trust Him enough to give away a portion of all that He provides. He wants us to simply let go of it. When we acknowledge that He is our Provider, we honor Him by giving first. We do not honor Him when we donate from what we have leftover at the end of the month.

It is vital that we learn to be generous with others to avoid the dangers of trusting in our possessions, our assets, or our net worth. As we advance God’s kingdom by practical means, we experience true riches through giving.

As you begin the year, resolve to honor the Lord by the way you handle money. Giving is not mandated by God. He asks us to give so He can pour out his blessings on us and others (Malachi 3:10). Generous living is one of the greatest blessings of financial freedom. When it comes from a heart of love and gratitude, not an obligatory attitude, it can change you. Plus, giving multiplies in value here and on into eternity. Paul wrote an entire apologetic for the benefits of giving in 2 Corinthians 9:6-12. Be sure and meditate on it.

Believing He loves us and knows what is best for us, we can trust Him even when giving just makes no earthly sense. We give first because He asked us to do so. And when He increases our income, He wants us to increase our standard of giving, not our standard of living.

When confronted with this practice, I told my wife that it would be necessary for us to change everything in the way we managed our budget. She said, “Exactly!”

Giving first does require an adjustment to your budget so you’re prepared to give on a regular basis. Once you develop the habit, it will become something you look forward to doing.

Start by tithing to your church. It is not a law or a tax but a great principle to apply for a beginning goal. Once this is in place, continue to seek His will and direction to grow more and more generous.

Save Second

“Go to the ant, O sluggard; consider her ways, and be wise. Without having any chief, officer, or ruler, she prepares her bread in the summer and gathers her food in harvest.” (Proverbs 6:6-8 ESV)

Step 2: Save a portion of everything that you receive. Make it your absolute second priority and do not compromise.

When it comes to saving money, consistency is key. That can be achieved by living below your means which requires contentment.

Contentment motivates us to enjoy frugality. We gratefully drive used cars, live in smaller homes, and ignore the newest fads. It gives us flexibility and margin in our budget so we can give generously first and save second as our most important priorities.

To get started right in 2021, make your first savings goal to set aside $1000 in an emergency fund. Then work on setting aside a full three months of living expenses. This money should be in an accessible savings account in the event of an emergency. You may want to increase this fund to six months of your living expenses but that can happen in 2022. For now, achieve this initial savings threshold and you will be on your way to a new habit that will completely change your finances for the better. Crown has excellent online courses to help guide you on this journey.

Whether you can save a little or a lot, your confidence must rest in the Lord. He will never leave you or forsake you. Money will.

“Keep your life free from love of money, and be content with what you have, for he has said, ‘I will never leave you nor forsake you.’” (Hebrews 13:5 ESV)

Stay Focused

Start this year with hope and anticipation of what you can accomplish in the strength of the Lord. Most people abandon their New Year resolutions by mid-February! Take it a day at a time and realize that the benefits will last beyond a lifetime–they will ripple into eternity!

“Delight yourself in the Lord and He will give you the desires of your heart.” (Psalm 37:4 ESV)

Praise the Lord, it is 2021!

This article was originally published on The Christian Post on January 1, 2021

Researchers at Statista.com estimate that consumers in the United States are projected to have spent an average of $850 on Christmas gifts this year. That is similar to what was spent in 2019.

While we may fuss that this holy season has become all about materialism or consumer-driven hyper-indulgence, much is to be appreciated about the incredible outpouring of love, gratitude, and generosity that is shown to family members, friends, employers, employees, and even strangers because of this miraculous birth of the Christ-child in a crude, Middle Eastern manger. What started with gold, frankincense, and myrrh to honor this very special newborn babe has exponentially rippled into a massive economic surge the world over. The biggest birthday party in the world is still cause for celebration and the giving of gifts more than 2,000 years later. Yet, it is not what we give on Christmas that matters the most.

Famed scholar and author C. S. Lewis said, “The Son of God became a man to enable men to become sons of God.” That, dear Christian, is the most glorious gift of Christmas!

Today we celebrate Christ’s birth, planned before the creation of the world. As you go about your day, ponder these life-changing truths from Scripture:

Christmas Prepares the Way for Our Redemption

“For God so loved the world, that he gave his only Son, that whoever believes in him should not perish, but have eternal life. For God did not send his Son into the world to condemn the world, but in order that the world might be saved through him.” (John 3:16-17 NIV)

“For the wages of sin is death, but the free gift of God is eternal life in Christ Jesus our Lord.” (Romans 6:23 ESV)

Christmas Prepares the Way for Our Adoption

“… When the fullness of time had come, God sent forth his Son, born of woman, born under the law, to redeem those who were under the law, so that we might receive adoption as sons.” (Galatians 4:4-5 ESV)

Christmas Revealed God’s Greatest Gift to the World

Christmas Revealed God’s Greatest Gift to the World

“But God, being rich in mercy, because of the great love with which he loved us, even when we were dead in our trespasses, made us alive together with Christ—by grace you have been saved— and raised us up with him and seated us with him in the heavenly places in Christ Jesus, so that in the coming ages he might show the immeasurable riches of his grace in kindness toward us in Christ Jesus. For by grace you have been saved through faith. And this is not your own doing; it is the gift of God, not a result of works, so that no one may boast.” (Ephesians 2:4-9 ESV)

That gift will change your life – both now and for eternity! Receive it, believe it, and glorify God with all He’s so lavishly given to you and me.

I, Chuck Bentley, together with my wife Ann, who assists me with writing and researching this weekly column, and all of us at Crown Financial Ministries, wish you a very Merry Christmas!

This article was originally published on The Christian Post on December 25, 2020.

Dear Chuck,

Covid set me back financially this year. As a result, we’re having a very frugal Christmas. Can you offer any tips on setting financial goals for next year? I want to be better prepared for what may lie ahead!

Getting Ready for 2021

Dear Getting Ready,

I am so sorry for the setbacks you have suffered during this pandemic. Millions of people just like you are looking forward to the new year with great anticipation and are hoping to make improvements in our finances.

New Year, New You

January is typically a time of renewal. For many of us, that includes diets, health and fitness goals, relationships, or financial plans. However, after what we have experienced in 2020, our highest need will be for renewed hope. Watching the news, scrolling through social media, and listening to certain friends or family members will not fulfill that need. Hope gets us through the tough seasons and gives us direction in times of uncertainty. Thankfully, we have the ultimate source of hope: Jesus. We need to learn to rely on Him in order to cultivate that hope. Here is a quick outline of steps for 2021.

Step One: Make a Vow. Dedicate this year to the Lord and seek his guidance in all decision-making.

“Commit your work to the Lord, and your plans will be established.” (Proverbs 16:3 ESV)

Step Two: Make a Plan. Plan and encourage one another daily.

“Two are better than one, because they have a good reward for their toil.” (Ecclesiastes 4:9 ESV)

Pray for self-control and the willingness to stay focused throughout the coming year.

“But the fruit of the Spirit is love, joy, peace, patience, kindness, goodness, faithfulness, gentleness, self-control; against such things there is no law.” (Galatians 5:22-23 ESV)

Step Three: Make a Target. Defining your financial goals gives you something to aim for.

Step Four: Make a Budget. Gather your financial records, track your expenses, and create a budget. Make giving your first priority. Establish an emergency account. This will enable you to cover unexpected expenses so that you can avoid debt. Start with $1,000 and then aim for an amount that covers 3-6 months of your overhead expenses. Analyze lifestyle decisions. Some short-term ones to consider include replacing a vehicle, repairs, maintenance, vacation, gifts, etc. Long-term decisions may include a down payment for a home, education, retirement, etc. Keep your tax liability in mind and plan accordingly.

Step Five: Review Your Insurance. This is a good time to review your insurance coverage: Homeowners or Renters/Auto/Liability, Disability, Life, and Long-Term Care. Not only should you determine if you have coverage but also if you are getting the right price for what you have in place.

Don’t Overlook These

Update your will. Today this includes creating a Living Will or Trust, Health Declarations, Power of Attorney documents, and password files.

Pick a debt management plan and pay off all credit cards! Christian Credit Counselors are trusted partners of Crown and have helped hundreds of thousands of families eliminate their credit card debt. Once free of consumer debt, you can begin investing.

Depending on your age, put a reminder on your calendar to enroll in Medicare before your 65th birthday. Determine when you should begin to draw social security.

Check your credit reports from Equifax, TransUnion, and Experian. This is important with the number of security breaches. Check to make sure information is correct and report any inaccuracies. Contact them to freeze your credit if necessary. This will prevent thieves from applying and obtaining credit in your name. You can unfreeze as needed.

Know your credit score. A free report is available at www.annualcreditreport.com. Some credit cards update your FICO score for free each month.

Calculate your net worth (assets minus liabilities). Aim for a positive number!

Get Wisdom!

There has never been an easier time to attain a Biblical financial education. Books, online studies, and insights from places like Sound Mind Investing, Generous Giving, and Crown’s online library of courses make it convenient and practical to learn year-round.

Most importantly, read the Word of God. You will gain wisdom, discernment, and hope that is more advantageous than anything the world offers.

God has called us to himself that we might shine light into the darkness and bring Him glory. At Crown, we provide resources that will renew your hope through Biblical truths about the Father and the gifts He has entrusted to you.

Merry Frugal Christmas

It has been our experience that a frugal Christmas is often the best Christmas. The focus shifts away from the number of boxes under the tree or the expense of the season to the awe and wonder of celebrating the incarnation of Christ; Emmanuel, God with us.

I wish you and yours a very Merry Christmas and a blessed New Year. We are here to help you on your journey in 2021.

The Article was originally published on The Christian Post on December 18, 2020

Dear Chuck,

I get tired of hearing how celebrity athletes flaunt their wealth and waste ridiculous amounts of money on frivolous “stuff.” Didn’t Larry have an outreach to professional athletes?

Tired of NFL, MLB, and NBA

Dear Tired Fan,

You are correct; Larry Burkett, Crown’s late founder, often advised professional athletes or spoke at events hosted by team chaplains. While we often read about the big salaries and over-the-top lifestyles, that is only one dimension of the story.

One of the factors we often forget is just how short the careers are for professional athletes. The Bleacher Report says that the average career in football is 3.5 years, basketball is 4.8 years, and baseball is only 5.6 years. Some of them spend years sacrificing while attempting to qualify for a spot in pro sports. Further, it is not uncommon to see the sudden wealth of athletes evaporate through bankruptcy, poor investments, mismanagement, or drug and alcohol abuse once their career is over.

We need to have greater sympathy for those who are in high-risk careers during and after their short run in sports. We also need to remember that each person has an individual choice in how they manage wealth, and there are some great exceptions to those you describe.

There Are Exceptions

Although not impacted by this ministry, as far as we know, there is an athlete who is doing it differently and who may impact your perspective of those who get paid well for their athletic skills. I looked deeper into the story of a very good steward whom you have probably heard of.

A Miracle Baby

35 years ago, the Tebows were working as missionaries in the Philippines. While there, Pam suffered complications with her pregnancy. A doctor recommended an abortion in order to save her life. Instead, she and her husband trusted God and delivered “a miracle baby.” They asked for prayers that their sickly baby would become big and strong. Little did they know that one day he would become a Heisman Trophy winner and professional NFL/MLB player who attempts to honor God in his endeavors.

Tim Tebow was interviewed by MarketWatch. This is where I learned some encouraging things about his financial philosophy and practices.

Tim’s Financial Advice

First, tithe. Second, be involved in things that make you money when you aren’t present. Things that will earn you a return while you sleep, are with your family, or are playing ball. Listen to people who have financial wisdom in areas that you do not. Tim knows his strengths and weaknesses. He says, “I try to fill my life up with people that are really good in certain areas because I think it’s important to be a good steward of your money and your resources. Money gives us the ability to bless and to help. It’s not just having it, it’s how you use it.”

He wants to put money away and live on a portion of it. Making memories is important to him, so planning is crucial. If you don’t make an effort to invest in your family, time can pass you by. He says that making special things happen is worth more than new shoes or clothes.

The Tim Tebow Foundation gives money to projects important to him: special needs ministries, orphan care and prevention, helping children with profound medical needs, and fighting against human trafficking. He strongly believes in helping those who cannot help themselves.

Photo by Tim Tebow Foundation on Unsplash

Tim’s Way to Keep Perspective

Tim starts and finishes each day with prayer. His favorite possession is the Bible he has owned since he was a child. He no longer takes it with him everywhere, but there was a time in his life when he did. It reminds me of Paul’s letter to young Timothy in 2 Timothy 3:14–17 (ESV):

But as for you, continue in what you have learned and have firmly believed, knowing from whom you learned it and how from childhood you have been acquainted with the sacred writings, which are able to make you wise for salvation through faith in Christ Jesus. All Scripture is breathed out by God and profitable for teaching, for reproof, for correction, and for training in righteousness, that the man of God may be complete, equipped for every good work.

In a blog post, Tim wrote that his life changed when he shifted focus from himself to things that really matter. Society stresses fame, fortune, and power, but abundant life is not found in that arena. He defines success as “the difference you can make in someone else’s life.”

He contrasts earthly success with eternal significance in another post:

When we succeed, we get to earn more, move up, take vacations, and reap the fruits of our efforts, but when we strive for eternal significance, we become compelled to share and give back. When we succeed, we impact our individual lives, but when we are significant, we impact others. To transcend business success into eternal significance, you have to take your gifts, find a need and meet it. Achieving significance means we go beyond gaining financial comfort and we strive to serve others.

Lessons for Us All

Tim’s life reminds me of the passage in Luke 16, beginning in verse 10: “One who is faithful in a very little is also faithful in much…” I am encouraged that Tim and other believers who hold positions of influence honor God with their finances and steward all that they have wisely for His glory. May they boldly proclaim the gospel and winsomely defend it.

Each of us is given unique talents, abilities, and resources to steward as well. God wants us to reflect His light upon this dark world. Let us follow Tim’s example! Join me in praying for the protection and faithfulness of those God has put into professional sports.

This article was originally published on The Christian Post on December 11, 2020

Dear Chuck,

My husband told me we need to discuss our family finances. I asked him if we could wait until after the holidays. He agreed to but I’m a nervous wreck. What should I do to prepare?

Nervous about Our Finances

Dear Nervous about Our Finances,

The fact that your husband wants to discuss your finances does not necessarily mean that something is wrong. It could be a very positive step in the right direction! He may just want to open the dialogue so you two can get on the same page and work towards some common goals. Prepare your heart, encourage his leadership, and welcome his desire to talk.

Some Possible Scenarios

There are several reasons that spouses get nervous when it comes to discussing finances. Painful memories from childhood or later on may reveal insecurities. The fear of changing one’s lifestyle can uncover misplaced dependencies. There’s a fear of shame that accompanies bad investment decisions or the loss of income. Financial infidelity may be discovered and trust may be threatened. He may need to talk to you about his job or a potential layoff.

Is debt an issue in your marriage? A survey conducted by Fidelity Investments found that couples concerned with debt argued significantly more than those without debt concerns. They also found that they have difficulty having conversations about budget/spending, managing debt, saving, and investing for the future.

The truth is, marriages function better when there are no secrets. Financial decisions need to be shared and discussed with honor and trust. If mistakes have been made, this is the time to confess, repent, and forgive. Regardless of what is revealed, we can trust the Lord because of His promise: “And we know that for those who love God all things work together for good, for those who are called according to his purpose.” (Romans 8:28 ESV)

Build Trust

46% of those surveyed at Wallet Hub said they’d leave a relationship if their partner spent money foolishly. Half wouldn’t marry someone with bad credit, and a majority said financial infidelity might be worse than actual cheating. This reveals the impact money has on couples.

Financial issues can signal a lack of self-discipline, drug or gambling addictions, or unmet emotional needs. If your marriage is under a great deal of financial stress right now, taking the time to sit down with your spouse and talk about any deeper issues could be the best thing that could happen.

Ask the Lord to prepare your heart by removing any fear or anger. Then set aside a time and place, free of distractions, so you and your spouse can focus on your situation.

Ways to Prepare

Solomon said, “Wisdom, like an inheritance, is a good thing…it preserves those who have it” (Ecclesiastes 7:11). Ask the Lord for wisdom with your finances. Seek to preserve or find unity.

Topics to Discuss and Act Upon

You can get through this together. Many couples are helped by scheduling regular money dates to better understand and apply Biblical financial principles. Crown’s online courses are a convenient way to start growing a similar financial mindset. You might also benefit from working with a believing mentor or couple. Ask your pastor for recommendations or consider wise people you know.

For an in-depth understanding of money and marriage, get a copy of my book, Money Problems Marriage Solutions. Here are 7 steps that helped me and my wife get unified and that I believe are critical to assist any couple to make financial progress:

Don’t let this ruin your Christmas. Blessings to you and your family. Let us know how it goes!

This article was originally published on The Christian Post on December 4, 2020.

Dear Chuck,

My husband and I just relocated and want to start a business in which he has years of experience. He left a company that lacked integrity and was losing clients. We have money but don’t know many people here yet. Any suggestions before we step out?

Pensive Entrepreneurs

Dear Pensive Entrepreneurs,

It would help to know what kind of business you want to start. It sounds like it may be dependent upon your network to be able to grow and your concern is that your capability is high, but prospects are low. Just guessing.

Relational Capital

Far too often people measure their business plan only by how much financial capital they have. If they have lots of money they may become overconfident. If money runs low, stress and vulnerability increase. This narrow focus omits a form of capital that is of equal or greater value: relational capital. More often than not, it is your relationships with others that can make or break your business.

Let’s review some principles around this that you can hopefully apply to your plans.

Business

Your husband can give thanks for lessons learned and build a business grounded in the knowledge he gained. Evaluate your relational capital in three areas: staff, clients, and suppliers.

A company’s culture is built on the way it values people. This requires investing time, expressing appreciation, communicating details effectively, and setting realistic goals and deadlines. Always treat others with courtesy, compassion, and integrity to build trust. Relationships within a company create a team that respects and enjoys working together. Employee retention rises with job satisfaction which is impacted by positive morale and productivity.

Can you attract good staff to your company in the new location? Give this a “Red Light/Green Light” evaluation.

Good client relationships build loyalty. This can lead to referrals and word-of-mouth recommendations which grow sales and provide more jobs. Do you have good potential clients in your new location? Give this a “Red Light/Green Light” evaluation.

Positive relationships among suppliers are valuable too, especially if you ever need their help. A good reputation can even put you in good standing with competitors. Not all locations are conducive to have good supplier relationships. Give this a “Red Light/Green Light” evaluation.

I would not launch the new business until all three of the essential aspects of these relationships were “Green Lights” depending upon the type of business you plan to start.

What does God say about the importance of relationships?

The Bible instructs us in the way we should treat those with whom we have relationships. I am including only a few verses.

“Put on then, as God’s chosen ones, holy and beloved, compassionate hearts, kindness, humility, meekness, and patience, bearing with one another and, if one has a complaint against another, forgiving each other; as the Lord has forgiven you, so you also must forgive. And above all these put on love, which binds everything together in perfect harmony.” (Colossians 3:12-14 ESV)

“Repay no one evil for evil, but give thought to do what is honorable in the sight of all. If possible, so far as it depends on you, live peaceably with all.” (Romans 12:17-18 ESV)

Where to Develop Relationships

Church is a great place to meet like-minded people. As you are able, plug into the church, volunteer to serve, and take an active role in classes, trips, fellowships, or small groups.

Professional organizations related to your career offer community and relational capital opportunities. Not only are they a place to be served but also a place in which you can serve and help others. They can be a source of guidance, accountability, growth, and encouragement.

Your neighborhood is a great place to plug in. Offer to serve on your homeowner’s association (HOA) and be attentive to the needs around you. Reach out to the lonely, the elderly, the single, or the overworked parents. You will quickly grow relationships as you get involved and possibly make lifelong friends.

Author Gary Chapman says, “Love is the fundamental building block of all human relationships. It will greatly impact our values and morals. Love is the important ingredient in one’s search for meaning.” By showing love to your staff, clients, and suppliers, not only will your business grow, but you will have a much happier and fulfilled life as well.

Let me know if you decide to launch the company. Remember, financial capital is important but has a limited value. Relational capital is priceless.

This article was originally published by The Christian Post on November 20, 2020.