Dear Chuck,

My wife and I are newlyweds and struggling to spend less than we earn. Our parents agreed to help us until our first anniversary which is in February. To prepare for that date, we need help now.

Spending Stress

Dear Spending Stress,

This has been a challenging time for many couples especially with the ease and constant availability of online shopping. With the click of a button, we can have just about anything we need or want delivered to our doorstep.

Spending less than you earn is the golden key to financial stability. Without this, you will always be under stress. But it is not a common practice for millions of individuals and couples.

Many Americans live paycheck to paycheck. Bankrate’s January Financial Security Index survey of Americans revealed:

You can order your finances in a way that honors God by establishing a reasonable standard of living and choosing to make His priorities yours.

Look back over your marriage and pre-marriage years. Both of you came into the marriage with a philosophy of money. Instead of relying on what you were taught in the past, learn God’s financial principles.

Romans 12:2 says, “Do not be conformed to this world, but be transformed by the renewal of your mind, that by testing you may discern what is the will of God, what is good and acceptable and perfect.”

We can be trained to change our behaviors, but transformation–a total renewal from the inside–comes through having our minds renewed by God’s truth. Good beliefs produce good behavior. When a couple’s beliefs are unified, the fruit we produce as husband and wife will bless each other and the world.

If you lack a financial plan, have bad spending habits, and make extravagant lifestyle choices, you and your wife need to unite in a concerted effort to make a change. Recognize that God is the owner of everything and that you are a steward, a manager, of all He provides.

Learning to spend less than you earn now will impact your marriage and finances for the rest of your life. You will be free to give as God directs, save, invest, and not have to borrow for major expenditures. You will set an example for others and motivate them to make adjustments.

I recently asked people for tips on living below or within their means. Perhaps some of these suggestions will resonate with you and your wife.

Another idea is financial fasting. Like fasting from food, you give up something for a period of time. It can provide margin quickly on a tight budget. Here are some examples: don’t eat out for a month, don’t buy new clothes for 3 months, don’t buy entertainment – instead, play board games, borrow videos, hike, bike, or go to museums…don’t buy anything new for a month. You get the idea.

A new survey conducted by MassMutual reveals that 1 in 5 Americans saved $1,000 this summer due to coronavirus restrictions. They spent less on weddings, vacations, travel, nightlife, and personal care. Without a clear plan, that money will be spent elsewhere. That plan is called a budget.

If you have consumer debt, then you, the borrower, are a slave to the lender. Since we don’t see lenders face-to-face we don’t think about this truth every…single… time we use a credit card. But, we are, in fact, held captive until that money is paid back. Debt limits generosity. We miss the joy in blessing others because oftentimes money is spent on stuff we don’t need. But, there are millions of people with needs we cannot even fathom. Make a plan to pay off your debt.

Paul learned to be content in whatever situation he was in and so can you:

I have learned in whatever situation I am to be content. I know how to be brought low, and I know how to abound. In any and every circumstance, I have learned the secret of facing plenty and hunger, abundance, and need. I can do all things through him who strengthens me. (Philippians 4:11b-13 ESV)

Don’t allow the world to dictate how you spend your money. Renew your mind on the truth of God’s Word. Be grateful for what you have, maximize income, and minimize expenses. This will allow you to reduce debt quickly so you can experience the abundant life that God wants for you. Oh, and one more tip, use our fantastic new program called Money Dates to help you and your spouse to get united! It works!

This article was originally published on The Christian Post, September 4, 2020.

Dear Chuck,

I’m hearing more and more about financial scams…. I’m concerned about my daughter falling for one while she’s attending college out of state.

Scared of Scammers

Dear Scared of Scammers,

I’m with you! You and your daughter should be on alert as a downturn in the economy always creates an upturn in the activity of scammers!

Before I get into a deeper look at scams happening to so many groups right now, let your daughter know about this one: Students are receiving messages from scammers posing as someone from their school or college. Sometimes it is a computer generated voice message. These claim that students have to access a portal for information or stimulus payments using their college log-in details. This link leads to a “copycat” college sign-on page, enabling thieves to steal usernames and passwords. But, unfortunately, there are endless others.

Erin Hurd at the NerdWallet.com recently wrote:

More than 2.3 million cases of fraud and identity theft were reported in 2019, according to the Federal Trade Commission — an increase of 26% from five years earlier and 138% in a decade. Credit card-related scams accounted for a significant chunk of those cases, including more than 40% of identity theft reports. And those were just the cases that were reported to law enforcement and consumer protection agencies.

And this was before COVID hit!

Thieves are experts in devising ways to rob innocent individuals. I just learned of a young couple who lost their savings in a Target gift card scam. We should recognize warning signs and know how to protect ourselves, then share the knowledge with our families, friends, neighbors and churches. From young to old, scammers don’t care who they rip off. I hope this article will help you prepare your daughter while she is away at school.

A great deal of identity or account theft happens via the internet access services. Avoid public hotspot problems by asking employees for the correct network name and password. Beware of “free public Wi-Fi” names. Never log into your bank account or use personal information at a public site. Use a virtual private network (VPN) which secures connection on unsecured public networks.

Never give or sell your Social Security number or personal I.D. information to anybody. Don’t answer phone numbers you don’t recognize. If it is important, they will leave you a message or call back. Hang up on robocalls. Put your phone number on the National Do Not Call Registry. Don’t respond to threatening voicemails.

When using ATM or gas station card readers, look for skimmers which are devices attached on top of or beside the card slot. If there is any tampering, scratches, or adhesives on the machine, don’t use it.

Review URLs before entering private information. Check for the padlock symbol in the address bar or copy/re-enter the web address to see if it’s legit.

Check your financial accounts often. If you suspect fraudulent activity, notify your credit card issuer or bank immediately.

The Federal Trade Commission gives a few other suggestions.

Online Fraud and Scam Protection:

The Consumer Fraud Reporting website describes common scams with pertinent information. In addition, I’ve listed some categories alphabetically for reference.

Whether you experience an attempted scam or fall for it and are ripped off, it is good if you will take the time to report the crime to help others who may be next. Hopefully this list will help make that easier:

Over the years, I have counseled a number of victims of scams or people who were taken advantage of by a high pressure salesman, a dishonest business or an unscrupulous person. Remember, no matter what you have lost, whether it is your life savings, your identity information or simply your pride, God will not be mocked. The unrighteous scammers will one day receive due justice. Woe to them on that day.

Trust the Lord through your shock and pain. Turn to Him and ask for His help to restore whatever you have lost. I have seen Him take care of victims in ways they could have never imagined. He is a God of vengeance and justice. He can turn ashes into beauty.

This article was originally published on The Christian Post, August 28, 2020.

Dear Chuck,

I’m trying to teach my children/grandchildren some basic financial principles. Any tips I could pass on in regards to investing?

Motivated Grandmother

Dear Motivated Grandmother,

What a blessing for your family that you want to help them get better with their finances. It will not only help them for the here and now, but also prepare them for that day when their stewardship will be evaluated by the Lord.

Before investing, it is essential that young people understand that God owns everything and that He is their provider. This is the motivation to responsibly manage all that He entrusts to them, whether a lot or a little. This also sets their heart right to avoid investing to get rich but rather to be faithful and generous towards others.

When young people follow a few basic principles, margin is created for money to be invested. These go contrary to the way in which many Americans live today. Here is my simple list that if followed, will set them on the right path.

Establishing self-discipline early in life will enable them to live out Proverbs 21:20 which states, “The wise man saves for the future, but the foolish man spends whatever he gets.” (TLB)

It is not uncommon to find that a young person has already found themselves buried in credit card debt and is stuck in cycles of overspending. If you find that this is the case with any of your children/grandchildren, I recommend our trusted partners, Christian Credit Counselors. They have helped hundreds of thousands of people eliminate their credit card debt and rebuild their financial foundation.

Money saved is not at risk. However, money invested is at risk of loss. That’s why you should advise them to only invest money after becoming a giver and a saver. No one should invest without a purpose. So here are some questions to help establish a proper reason for investing.

Answer the following:

All of these should be considered and evaluated before any money is allocated to investment.

After setting goals, beginning investors must understand some basic investment rules. Investing is not intended to be an overnight get-rich-quick success. It is a long-term undertaking, so early investors have the advantage of giving their money time to grow.

It should not affect the daily family routine and must not cause the family stress or discord. In fact, I recommend that couples take time to discuss and pray through their goals to maintain unity. A wise spouse can offer unique insight and proper balance in decision making.

Start small and do something on a regular basis each month. It is surprising at how significant small decisions will become as the decades pass. Make sure you thoroughly understand each investment, that liquidity is important in the event of an emergency, and that diversification is key.

Think of investing like planting a tree. It could die. But if you nurture it, over time it will begin to grow and grow. The longer you allow it to remain planted in one spot, the more likely it will produce good growth yields. This is the philosophy of value investors as opposed to traders or gamblers.

Twenty-somethings have certain advantages over those who wait to begin investing, including time, the ability to weather increased risk and opportunities to increase future wages. – Jean Folger, Investopedia.com

Investing early helps you think about how you use money. When you develop Biblical financial habits early in life you are able to invest sooner. This gives you a head start and the benefit of time. Plus, you gain years of practice to help you recover from any mistakes and avoid emotional roller-coasting.

Research, Don’t Guess

Proverbs 24:3-6 (ESV) is a great verse to apply to your investing philosophy: “By wisdom a house is built, and by understanding it is established; by knowledge the rooms are filled with all precious and pleasant riches.” This means that we are to make investment choices by using our mind, not simply throwing darts and hoping to pop a balloon with a prize inside. Wisdom and knowledge are the keys to success. Diversification is Solomon’s advice in Ecclesiastes 11:2.

Most people think of the stock market when they think of investing. This would include a variety of choices for publicly traded securities such as:

But don’t forget other choices like real estate, starting a small business, or investing in a privately held company.

Finally, especially when it comes to your grandchildren, teach them to invest in themselves early in life to gain the education, skills, and wisdom to reach their income earning potential. One of the highest returns on any investment relative to temporal returns is to make ourselves more valuable whether as an employee or entrepreneur. God is honored when we become excellent at whatever we are called to do.

I encourage you to follow through with your desire to pass along God’s principles to your children and grandchildren. What a blessing it will be to see what incredible returns will happen in their lives as you make these deposits of love and wisdom. Go, Grandmother, Go!

This article was originally posted on The Christian Post August 21, 2020.

Dear Chuck,

My wife and I are considering buying a house now although it’s a year earlier than we planned. We don’t know if the low rates will be available next year. Should we go for it?

Buy or Hold?

Dear Buy or Hold,

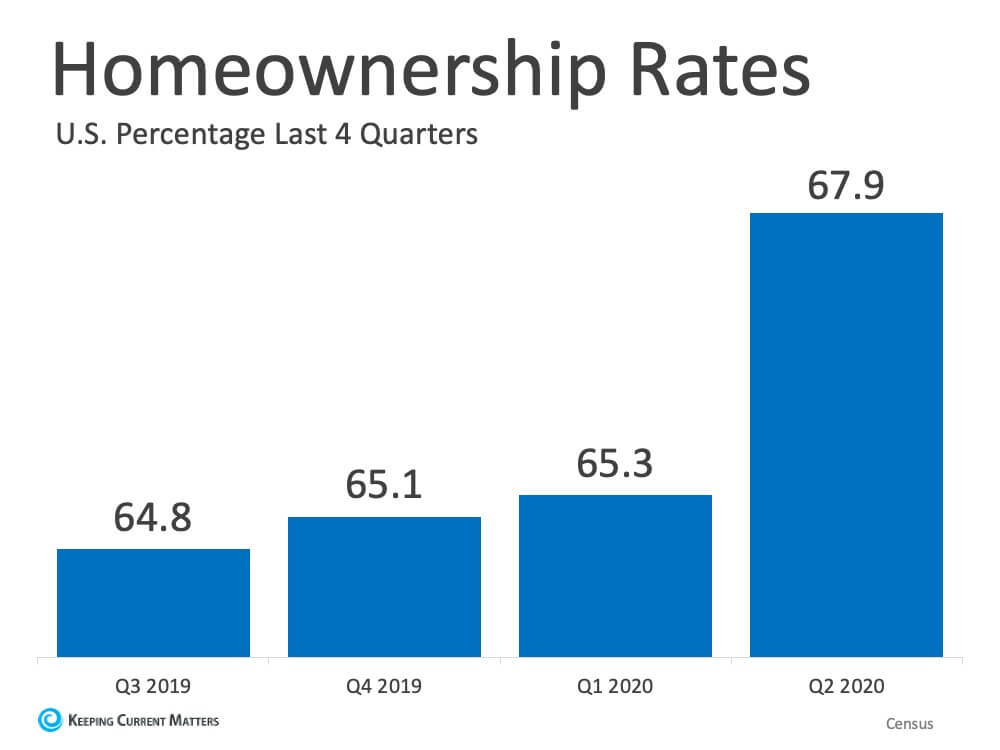

You and your wife are not the only ones with this mindset. Homeownership is on the rise in different parts of the United States. People have been stuck at home with time to research available inventory in different parts of the country. The historic low mortgage rates and pandemic fears along with the flexibility of remote work are propelling many to buy. Some are seeking to leave areas where crime and disruptive protesting have impacted their livelihoods.

It is a good time to buy a home, but only if you are ready. Let’s look at the trends first then some pros and cons of buying now.

(Image source: https://www.keepingcurrentmatters.com/2020/07/29/homeownership-rate-continues-to-rise-in-2020/)

You can read Zillow’s Forecast here. I have pulled some of the highlights which point out that rates are low, but so is inventory:

Low mortgage rates are poised to stay for a while, so buyer demand should stick around even as seasonal headwinds start to form. Although, there are some storm clouds gathering. Broader uncertainty due to the surge in coronavirus cases and the prospect of disappearing fiscal support pose looming limitations as well. Historically low levels of for-sale inventory also has the potential to thwart the strong gains the housing market has recently enjoyed, and while for-sale inventory rose slightly in June, inventory remains significantly below last year’s levels. The coming months will be a true test of the housing market’s enduring strength and resilience.

There are benefits to homeownership that include safety, security, and accessibility to desired education and lifestyle opportunities. Habitat for Humanity acknowledges the crucial role of homeownership in society:

Habitat for Humanity knows that safe, decent and affordable shelter plays an absolutely critical role in helping families to create a new cycle, one filled with possibilities and progress. Affordable homeownership frees families and fosters the skills and confidence they need to invest in themselves and their communities. The outcomes can be long-lasting and life-changing.

Studies conducted by academics and experts draw a straight line between housing quality and the well-being of children. Surveys of Habitat homeowners show improved grades, better financial health, parents who are more sure that they can meet their family’s needs. Wherever we work, we witness tangible evidence that strong and stable homes help build strong and stable communities.

The biggest financial decision most of us ever make is buying a house. Too often in America, we find couples who are “house poor.” This means that they were convinced they should stretch to buy a home in their preferred neighborhood, their preferred school district, or with their preferred amenities, only to get several months into it and find they stretched too far.

If your total housing expense–which includes your rent or mortgage, insurance, taxes, maintenance, and utilities–is 40% or more of your total income, it will likely cause financial stress. Plus, it restricts the ability to give, save, and invest.

Keeping your total housing expense at 30% or below will relieve a great deal of stress. Have a look at our free mortgage amortization calculator. Be sure to include these items in your budget:

But godliness with contentment is great gain, for we brought nothing into the world, and we cannot take anything out of the world. But if we have food and clothing, with these we will be content. (1 Timothy 6:6-8 ESV)

It is always good to be patient. I am curious as to why you were planning to buy a year from now. If you were waiting to save more for a down payment, or to be in a better position with moving expenses, by all means, wait. Those who are content and patient make far better decisions than those who are hasty and impatient.

I hope this helps you to make a better decision. My guess is that mortgage rates will be low for quite some time, so be patient and make a wise decision that will bring you and your family years of joy.

This article was originally published on The Christian Post, August 14, 2020.

Dear Chuck,

Gold is soaring now. Should I buy gold before our economy tanks?

Gold Fever

Dear Gold Fever,

I’m probably going to step on some toes because people have very strong opinions about gold.

Gold, speaking of the tangible metal, is an asset, a commodity, and makes for a good insurance policy–but not a great investment. It provides no income stream and does not earn dividends. It can be difficult to trade. People have made and lost money trading gold in the stock market, while others have profited mining it, using it for ornamental purposes and as a base metal.

Gold is a medium of exchange–if people want it. During a crisis, other things may prove to be more valuable such as food, medicine, transportation, shelter, etc. Some view it as a hedge against inflation. Others see it as a speculative asset that varies in price according to the emotion of the market. Gold can be held in the form of gold futures, gold coins, gold mining companies, gold ETFs, gold mutual funds, gold bullion, and gold jewelry.

The U.S. abandoned the gold standard in 1971 when our currency was no longer backed by gold, but is still important globally. Early in 2019, the World Gold Council reported that central banks throughout the planet bought the most gold in 2018 in over 51 years. Central banks bought 651 tonnes (metric) of gold, an increase of 74% from 2017. The biggest buyers were China and Russia.

When gold hit an all-time high recently, it confused experts. It usually rises when stock prices are falling or when inflation is rising. None of those things happened. Was it due to the worsening U.S.–China relations, the economic distress of the coronavirus, or the weakening U.S. dollar? It is a mystery but could be all of the above.

Warren Buffett does not consider it a worthwhile investment:

Gold is a way of going long on fear, and it has been a pretty good way of going long on fear from time to time. But you really have to hope people become more afraid in a year or two years than they are now. And if they become more afraid you make money, if they become less afraid you lose money, but the gold itself doesn’t produce anything.

I wrote about gold and diversification back in 2012 based upon Biblical principles.

Solomon, in his wisdom, offers an excellent investment strategy in Ecclesiastes 11:2: Divide your portion to seven, or even to eight, for you do not know what misfortune may occur on the earth. Solomon found that the only path to peace of mind in investment planning was to diversify and surrender the outcome to God. Based on this, it would be wise for investors to make informed choices that are spread out to cover the various categories of the investment spectrum.

Many investors today are hoarding precious metals, especially gold, as economic crisis insurance. Caution and preparation are wise, but no one can prepare for every possible calamity. Because the buying and selling of precious metals is oriented more toward a long-term investment strategy, any long-term financial planning could conceivably include the purchase of some precious metals.

Generally, though, the only people who are able to make money with precious metals are the brokers who live off of gullible amateur speculators. Nevertheless, if an investor is interested in investing in precious metals, he or she should limit his or her investment to no more than 5 to 15 percent of the total investment portfolio.

Precious metals are long-term stores of value and internationally recognized assets of last resort. They can diversify and stabilize a person’s portfolio, they can protect it against market fluctuations, and they do offer insurance against a currency collapse.

However, precious metals are volatile, speculative, high-risk investments. This investment area is for the investor with a strong heart and cash only. Unless an investor can afford to lose what he or she has invested, this is probably not an area in which a person would want to risk a lot of money, especially savings or retirement funds.

Although a portion of an investor’s investment portfolio could include precious metals, these will probably not protect an investor from financial misfortune in case of an economic crisis.

Choose my instruction instead of silver, knowledge rather than choice gold, for wisdom is more precious than rubies, and nothing you desire can compare with her. (Proverbs 8:10-11 ESV)

This article was originally published on The Christian Post, August 7, 2020.

Dear Chuck,

The government is talking about a second round of stimulus money – is it real? What should I do with it?

Watching for Money in the Mailbox

Dear Watching for Money in the Mailbox,

You are correct; the government is discussing the passing of another stimulus package. The Republican Party offered a $1 trillion proposal while the Democrats want $4 trillion. Treasury Secretary Steven Mnuchin wants $1,200 stimulus checks to be sent in August. But don’t assume that new money is on its way; there are qualifiers. Those making less than $75,000 will qualify for the full amount, those earning above $100,000 will not qualify, and those in-between will receive less than $1,200.

Based on the timing of the first CARES Act, we can make some predictions on when checks might be sent. If the current proposal passes the Senate and the House before the August recess, the first checks could be sent out by the week of August 24. If it doesn’t pass until after the recess, the checks could be sent the week of September 28.

Stimulus money is an unexpected windfall. It was never in your budget to begin with, so it offers lots of good options for improving your finances, if used wisely. Here are my thoughts and tips.

Crown is privileged to partner with Christian Credit Counselors to help free individuals and families from the burden of credit card debt. Their Christ-centered values and experienced team of friendly and professional counselors make their partnership an integral part of Crown’s mission to help individuals and families. If you need a debt management plan, this is a good time to contact them for their help.

You may be in a position to invest the money in a Health Savings Account (HSA), 401(k), a Roth IRA, or Taxable Investment Account. Or, invest in yourself via classes, certifications, online degrees, an upgraded computer, or equipping a home office.

Protect yourself from scammers. Don’t fall for the fake phone call from the “treasury department” needing your bank account information so they can make a transfer!

Don’t blow it in foolish ways. The government hopes that you will go out and spend the money quickly. It is better to be slow and deliberate before making a decision of what you should do with it.

Americans who are struggling should focus spending on immediate needs: housing, utilities, food and health care. Those who are at least 62 years old and are unable to make ends meet with the stimulus check may benefit from taking Social Security early. It can make sense for other reasons as well, making it worth the time to do some research.

The way we use stimulus money is an indication of what is in our hearts. God wants us to be faithful to Him when it comes to managing all money. Consider these passages:

One who is faithful in a very little is also faithful in much, and one who is dishonest in a very little is also dishonest in much. If then you have not been faithful in the unrighteous wealth, who will entrust to you the true riches? And if you have not been faithful in that which is another’s, who will give you that which is your own? (Luke 16:10-13 ESV)

This is how one should regard us, as servants of Christ and stewards of the mysteries of God. Moreover, it is required of stewards that they be found faithful. (1 Corinthians 4:1-2 ESV)

You and I are stewards of all that God provides, including stimulus checks! Put God first and manage it with the intention of pleasing Him.

This article was originally published on The Christian Post, July 31, 2020.

Dear Chuck,

I’m hearing more and more about a “cashless society.” What can we as believers do to prepare for such a possibility and how should we navigate the days ahead?

Prepping for Digital Currency

Dear Prepping for Digital Currency,

This is not an easy question as there are many strong, differing opinions; some say that it absolutely is going to happen, and others say that it absolutely will never happen.

A 2019 Harvard Business Review article points out that 30% of all transactions happen with cash. They don’t think it is likely to ever be eliminated as a form of payment. On the other side of the argument, a BBC article suggests it will get here sooner than we think. I fall somewhere in the middle as to the probability of it happening. But, to your point, we do need to be informed and prepared.

A cashless society means absolutely no cash. That means transactions will be fully digital and fully controlled. While many young people welcome it since they are almost there already, the idea deeply concerns me.

The most used form of payment today is debit cards, followed by cash. The coronavirus caused many to fear using cash because of possible transmission of the virus, even though there is no proof that paper money carries the virus any longer than plastic cards.

On July 14, 2020, an article from Bloomberg CityLab stated:

A June report from Square showed that at the start of the pandemic in March, 8% of U.S. sellers were effectively cashless, meaning that at least 95% of their sales were made through credit or debit card. That figure jumped to 31% by the end of April and has since leveled off at 20% in mid-June as cities reopen. In the U.K., cashless sellers jumped from 10% to 60%, according to the Square analysis, and dropped just slightly to 57% in June.

Cash carries more emotion for buyers. The loss when making a purchase is felt immediately. As CEO of a ministry that tries to help people steward their money, I’ve seen people improve their spending habits due to the psychological effect of using cash.

We’ve seen the use of cash discouraged and even refused by certain vendors. However, cashless stores were banned in San Francisco, New Jersey, and Philadelphia on the grounds of discrimination.

These factors could either propel or delay the push towards going cashless, so don’t make a determination too quickly one way or the other.

GlobalData predicts the following countries are poised to go cashless this decade: Finland, Sweden, China, South Korea, United Kingdom, and Australia.

Obtaining cash is getting more expensive. About 2 million Britons use cash day-to-day. However, 9,000 free-of-charge ATMs closed over the last two years, but cash machines that charge a fee for withdrawals increased 40% within a year. Negative interest rates will have an impact as well.

The International Monetary Fund (IMF) blog posts articles that reveal interesting data and political leanings. This one pushes the cashless move. However, the assistant director of the National Consumer Law Center, Lauren Saunders, says, “The cashless movement is a dangerous movement.”

Although disturbing, some are concerned with the government “unbanking” political enemies. Government control would also eliminate those who hoard cash or drop out of the financial system. The idea of the government being in control of all citizen money is concerning.

Protection is important. Supposedly, digital wallets are more secure than debit and credit cards because only the wallet providers see your information. Passwords and biometric authentication (retina scans, face, fingerprint, and voice recognition), auto-lock screens will be imperative to protect phones and accounts. This leads to even less privacy and ultimately less freedom once your biometric ID is used for all online access.

In Revelation 13, John describes the second beast that rises out of the earth:

Also it causes all, both small and great, both rich and poor, both free and slave, to be marked on the right hand or the forehead, so that no one can buy or sell unless he has the mark, that is, the name of the beast or the number of its name. This calls for wisdom… (v16-18a ESV)

Many believers see this verse pointing to a one-world government, headed by the Antichrist, that has absolute control over the entire global economic system. A global cashless society would be a step in making that control possible.

There are only two ways to be prepared for a cashless society. One is to grow in wisdom.

If any of you lacks wisdom, let him ask God, who gives generously to all without reproach, and it will be given him. But let him ask in faith, with no doubting, for the one who doubts is like a wave of the sea that is driven and tossed by the wind. (James 1:5-6 ESV)

Wisdom allows you to look at the facts and make appropriate decisions. We do not know if this trend is going to take us into a cashless society or not. That means we do not need to waste time in fear and needless use of energy to protect ourselves from it. At the same time, if we do head that direction, it will be wisdom which proves of greater value than our money.

The other way to be prepared is to be sure that your life is not defined by or controlled by money. The Bible tells us over and over to keep our lives free from the love of money. This allows us to avoid hoarding or the emotional fallout from losses. Our treasures have never been on Earth; therefore, whether we are cashless or not, we will never lose our true riches which are stored in Heaven.

If you’re looking for practical ways to prepare for these possibilities and seek to grow in wisdom, Crown offers many online studies, videos, and more on our online platform.

This article was originally published on The Christian Post, July 24, 2020.

Dear Chuck,

I am 46 years old. My company is closing its doors due to COVID-19. I have been adding to my 401(k) for 21 years. What do I do with it now?

Concerned About My 401(k)

Dear Concerned,

Thanks for the great question. Millions of people are facing a similar challenge. I will offer some explanation of the 401(k) program and some advice.

401(k) accounts are employer-sponsored defined contribution plans that function as tax-deferred retirement accounts. Employees who participate determine an amount to have taken out of their paychecks and directly sent to their 401(k) investment accounts. These may include mutual funds, exchange-traded funds, and target-date funds. Growth in 401(k)s have increased because pensions are less common.

More than 80 million workers actively participate in 401(k)s, with more than half-a-million different company plans in place, according to a January 2019 report by the American Benefits Council. Overall, a dizzying $5.7 trillion in assets are held within 401(k)s in the U.S.

Federal law requires employers to keep 401(k) funds separate from company assets. This prevents creditors from gaining access to it. You should be able to keep most of the funds and move them to another type of account.

Be sure to keep a record of your 401(k) accounts, all other bank or financial institution accounts, and important documents such as insurance policies, deeds and contracts. When there is turnover in the economy and moves like you are making now are happening more often, it is easy to lose track of transfers and financial accounts.

Millions of dollars are left unclaimed in everything from safety deposit boxes, bank accounts, savings accounts and retirement accounts each year. People simply forget they have the account or die without notifying their heirs of where the money was placed. It would be similar to having a storage facility that nobody ever knew about. All of your efforts to save are wasted which is poor stewardship.

The Bible reminds us to stay on top of the details: Know well the condition of your flocks, and give attention to your herds, for riches do not endure forever; and does a crown endure to all generations? (Proverbs 27:23-24 ESV)

It is not uncommon for me to hear from people who are losing money in their investment accounts, especially those who are making passive investments in a 401(k) or 403(b). Both of these accounts offer pre-packaged investment options so investors assume that making a quick choice is all that is necessary. Remember to do your homework on those choices and seek counsel from professional advisors or experienced investors who can help you with your asset allocation within your retirement accounts.

Proverbs 15:22 (NIV) is a great investment principle to put into practice: Plans fail for lack of counsel, but with many advisers they succeed.

God bless you as you seek your next work assignment. Don’t forget, we offer career coaching services as well. Learn more here.

This article was originally published on The Christian Post, July 17, 2020.

Dear Chuck,

I plan to get married soon. My future wife and I plan to combine our money at that point. We both have checking and savings accounts. What banks do you recommend?

Choosing a Good Bank

Dear Choosing a Good Bank,

I always like to say that marriage is a lifetime of learning to make good decisions together. Your question about a bank is a practical one, and is only just the beginning of thousands of more decisions you will need to make together.

Marriage is about becoming one. One in everything: name, address, bed, and money. Keeping anything separate, including checking accounts, develops a “his money, her money” philosophy, which usually leads to a him-versus-her mentality. There should be no “his money” or “her money” in marriage. It’s God’s money that we manage together. So let me give you enough information to help the two of you make a united choice on where you bank.

I would never deposit money in a financial institution that did not provide evidence that your deposits are insured by the Federal Deposit Insurance Corporation (FDIC) or the National Credit Union Administration (NCUA) which cover up to at least $250,000 per depositor.

Bankrate.com offers an excellent in-depth analysis of savings accounts.

Also check out Magnify Money’s list of:

The only reason to maintain separate accounts is for business purposes; for instance, to manage accounting for expenses associated with one’s job. Joint accounts require you to relax your grip on money. Rather than being “mine” or “yours,” it becomes “ours.” It requires mutual respect, honest communication, and working together for a common good. You can no longer justify selfish spending because in marriage, you are called to serve one another.

Joint accounts simplify bill paying and force earnest cooperation. Trust can be established and accountability expected. Common goals can be met through teamwork. Love and respect are foundational in stewarding the money you share in a common account. Money is a means by which God reveals our strengths and weaknesses and teaches us to depend on Him more fully.

Open new accounts before closing any existing accounts. Keep enough in them to meet the required minimum balance and to cover any automatic payments or checks that have yet to clear. Change direct deposits to the new accounts and adjust bill payments to begin once your first direct deposit goes through. Once all automatic transactions have cleared, you can empty and close your old accounts. Depending on the institution, this can be done over the phone, in writing, or in person. Verify that all transfers have occurred.

There are a number of good reasons to build a long-term history with a single institution. You will likely garner the maximum customer benefits if you maintain healthy balances and keep your accounts in order. Over time, you will achieve a valued customer status which may help if you ever encounter problems such as identity theft or need a loan or other assistance.

I hope this helps you and your fiancée make the decision together. The best decision will be one in which you are united, regardless of the bank you choose.

This article was originally published on The Christian Post, July 10, 2020.

Dear Chuck,

2020 has been a year of ”unexpecteds.” My wife is pregnant and we are growing concerned about raising a child in the city. We are considering moving since both our jobs offer online flexibility. Any advice? Thanks for your ministry.

Headed for the Suburbs

Dear Headed for the Suburbs,

First of all, congratulations on your pregnancy! Sounds like this may be your first child, hopefully of many more!

We are seeing an “urban exodus” brought about by many pressures for those living in major metropolitan areas. The coronavirus, political and social unrest, taxes, along with the cost of living, are weighing heavily on many people that populate our cities.

Some see the current threats as irresolvable. Many, weary of months in small apartments with young children, want space. Some have lost income, making city life unaffordable. A desire to work somewhere with open skies, a backyard, and friendly neighbors are luring many to the suburbs and country. They want peace and are moving to find it. Some justify second homes in the country as a necessary retreat from the city.

A Harris Poll taken in April 2020 found that nearly half of urbanites had browsed online for places to rent or buy away from less densely populated areas. The great migration of 2020 in the U.S. is to suburbs, self-reliance, and even off-grid living.

Real estate searches in suburban zip codes jumped 13% in May. Homes in certain areas sell within hours or result in bidding wars. People, desperate to leave cities, are buying homes sight unseen. Online real estate websites include Zillow, Trulia, Redfin, Homesnap, and Realtor.com. NeighborhoodScout.com grants access to information by address or area although a fee is required for in-depth analysis.

Rent or Buy

With interest rates so low, many see mortgage loans within reach. Bankrate.com offers current rates and calculators if buying is on your radar. Do not stretch to buy with the economy being so unstable or neglect an adequate emergency fund. Even though you both can work remotely, be sure your job security is strong before making a final decision. Check out my article on renting versus buying a house to help you make a rent-or-buy decision.

Moving Costs

Don’t forget to budget for moving costs, such as:

Get Informed

Familiarize yourself with the area. Drive through neighborhoods. Talk to residents. Ask questions. I’ve done this everywhere I’ve purchased a home. You will learn things about the homeowner association, schools, community, and more. A familiar area near friends or family can prove helpful with a baby on the way.

Research

The Bible tells of several men moving their families to escape dangerous times. A famine in Canaan led Abraham and Sarai to Egypt (Genesis 12:10) and Elimelech, Naomi, and their sons to Moab (Ruth 1:1). An angel warned Joseph to flee for protection in Egypt with Mary and Jesus (Matthew 2:13).

Ask God to give you clear direction. Pray with your wife. Seek counsel from wise people. Then move forward in faith knowing this: In the fear of the Lord one has strong confidence, and his children will have a refuge (Proverbs 14:26 ESV).

This article was originally published on The Christian Post, July 3, 2020.