Dear Chuck,

I am 25, live in a hot housing market, and feel squeezed by rising rents. I can’t see any way that I could ever buy a home! I need a plan and some hope.

Sick of Paying Rent

Dear Sick of Paying Rent,

We are in a very unique time when millions of renters are motivated to buy a home but feel trapped. Hopefully, this will not last too much longer. In the meantime, there are steps you should be taking now.

The Refinancing Boom

There was a refinance boom during Covid-19. Mortgage rates fell dramatically, and 14 million mortgages were refinanced. A 30-year mortgage fell to 2.65% in early January 2021, which allowed average homeowners to decrease monthly payments by $220. Others took advantage of 15-year mortgages, which dropped to 2.16%. Although monthly payments increased, these borrowers were motivated to save tens of thousands of dollars in interest while building equity faster than a 30-year mortgage.

Those desiring to buy a home today are struggling to find what they want because many homeowners do not want to sell. Mortgage rates are near 7%, and home prices are still high. These are disincentives.

According to Market Watch, “The mortgage refinancing boom is over, but its impact will be seen for decades to come,” said Andrew Haughwout, director of household and public policy research at the NY Fed.

Research shows that the refi boom of 2020-2021 differed from booms in 2003 and 2013 in three specific ways: interest rates were historically low, home equity was at an all-time high, and the rebound in rates was historically steep.

Count the Costs

When calculating the ability to buy, do not forget to add in the costs of property taxes, insurance, utilities, and HOA fees, along with emergency funds for maintenance and repairs. Consider additional costs for landscaping, furniture, window coverings, and décor. Take into account future expenses: child care, private education, braces, pets, college, vehicles, weddings, continued inflation, and unexpected costs, like caring for a family member or a loss of income. Depending on the climate, you may have expenses for snow removal, tree maintenance, and after-storm care. Will there be greater transportation costs? Needs arise out of the blue.

Experts recommend the 28/36 rule when buying a home:

If you are married, I recommend buying a house based on the lower of the two salaries because that provides flexibility in the use of a spouse’s income for greater saving, investing, or future goals. It also provides some protection in the event of job loss or if one of you chooses to pause your career.

Start Now; Prepare to Buy When the Market Changes

First, you should begin now to save for a down payment:

Next, be patient as you watch for mortgage rates to drop and more home inventory to come on the market in your area. When you think you are ready to buy, create a budget with a proposed mortgage payment. Include all expenses you may encounter. Do not fudge. It is wise to buy in a price range that keeps your expenses in a similar range as your rental costs, if possible. Buying too much house impacts saving for retirement, paying off debt, traveling, and the freedom to give as the Lord directs. It can create stress that affects your marriage and career. Just because you qualify for a more expensive home does not mean you should buy one!

Praise God for the place you live now. There are many benefits to renting that are not available to homeowners. Remember to number your days, for we are all just passing through. Steward wisely, and live intentionally with your “future home” in mind. Our hope is in the life to come, not in this one.

If credit card debt is a concern, Christian Credit Counselors is a trusted source of support. Getting out of debt can certainly help with your goal of home ownership. Reach out to them today; they may greatly benefit you.

This article was originally published on The Christian Post on May 26, 2023.

Dear Chuck,

I work and live with those who buy whatever they want, whenever they want. I find myself constantly influenced to join their spending sprees! Can you give me any tips that I can implement to control my spending immediately?

Spending Too Freely

Dear Spending Too Freely,

Yes, I can help you—been there, done that! Living in debt is deceptive. I once saw a sign that described what it was really like living beyond our means and on ever-increasing debt: “I started out in life with nothing, and I have most of it left!”

Based on consumer credit statistics, you are not the only one struggling. For the first time in more than 20 years, credit-card debt failed to fall between the fourth and first quarters. The U.S. credit card debt level is approaching a historic high of $1 trillion.

Find a Great Example to Watch and Learn From

Early in our marriage, my wife, Ann, worked with a remarkable single mom. She immigrated to the United States with her former husband, who was a soldier at the time. Shortly after they arrived in this nation, which was very foreign to her, she delivered their child, and he exited their lives. She found herself alone, without sufficient resources, without support systems, and facing a daunting challenge to make it all work.

We got to know her through work, but she became a close personal friend. Immediately, her habits stood out to us: she carried her simple lunch every day, including a dessert of 10 chocolate chips in a reusable sandwich bag (without the cookies). Rather than joining a fitness club, she walked ten flights of stairs each day after lunch in the bank building where she worked for slightly above entry-level pay. Her frugality kept her fit in mind, body, and finances. She earned a college degree and paid for a house and her daughter’s education. She eventually married.

Interestingly, this was also during a time of high inflation in the 80s. Mortgage rates soared to 17%! Although a painful time in many ways, she found joy in spending far less than she earned; she kept a budget, set goals, and made steady progress with her humble, disciplined lifestyle. She never complained. We actually were the ones most impacted after she spent time in our home over meals and holidays.

Know Where Every Dollar Is Going

Today, our economy is on shaky ground. I recommend using a budget and then applying the tips below to change your habits, prepare for the future, and live on less. Ann and I have learned to be frugal without missing out on life. We have found unexpected joy in saving money and becoming more generous.

Increase Your Savings

Build your emergency fund to avoid having to borrow or use a credit card. Stop all impulse spending, and reduce debt so you can pay off all bills each month. By eliminating interest charges and penalties, you take a step back from the financial cliff. Implementing a frugal lifestyle will give you extra money to deposit in a fund each month. Set up an automatic deposit, and increase the amount over time.

Time with Friends/Entertainment

If your friendships are not beneficial to you and your budget, make new ones. Volunteering is a great way to broaden your community. Enjoy budget-conscious friendships by going on walks, visiting museums, or taking advantage of free events. Listen to books, and work puzzles. Gather friends to play board games, hike, or bicycle. Pack a picnic, and meet at a park. Plan a potluck. Ask others to join you in a no-spend month. Make it a time to share budget-saving ideas and encouragement. Those you think don’t need to watch their spending may join you so they can save or give more. Consider the fact that they may be living a lifestyle that hides financial pain.

Limit/Drop Social Media Plus a Few Other Things

Scan credit card and bank statements for items to drop, like subscriptions and memberships. Instead, use the library or YouTube for free. Read for personal development and financial prowess.

Food

Gasoline

Reduce driving, compare prices (GasBuddy.com), carpool, bike, walk, and work remotely when possible.

Utilities

Clothing

Shop thrift/resale shops and yard sales, accept hand-me-downs, and borrow for special occasions. Aim for quality, not quantity. Get creative, and remake clothes. Cut off a dress for a new blouse. Convert pants to a new pair of shorts. When shopping online, put items in your shopping cart, then wait and compare prices for several days. It is likely you can live without them.

Self-Care

Take care of yourself but in a cost-efficient manner. Extend the time between hair or manicure/pedicure appointments. Or temporarily do without. Eliminate other expenses, or trade skills for essential services.

Wait, Wait, and Wait Some More!

The wise man saves for the future, but the foolish man spends whatever he gets.

Proverbs 21:10 TLB

Learning to delay gratification and wait for what you need pays big dividends. God can surprise in amazing ways! It is a sign of wisdom according to the Proverbs.

Christian Credit Counselors is a trusted source of support in assisting people with getting on the road to financial freedom. Reach out to them today; they may be of great benefit to you.

This article was originally published on The Christian Post on May 19, 2023.

Dear Chuck,

I am a baby boomer with lots of friends and a healthy community at church, but I see loneliness as a major problem for so many of my friends, our kids, and our grandkids. How do you think this trend will impact the economy in the future?

Worried about the Disconnected

Dear Worried about the Disconnected,

I am glad to hear of your concern for the disconnected and your insightful connection of this problem with economics. Loneliness is truly a devastating and costly problem.

Loneliness is no longer a problem that affects just the elderly or shut-ins. Three years after Covid-19 lockdowns and restrictions, reports reveal that loneliness has become a public health crisis. The U.S. Surgeon General recently addressed the issue: Our Epidemic of Loneliness and Isolation.

According to the Harvard Health Blog, “Isolation is the objective measure of how large your social network is, whereas loneliness is a subjective perception of how one feels. In other words, you can have many friends and be lonely, or no friends and not be lonely.” However, isolation is a risk factor for loneliness.

The High Cost of Loneliness

The CDC reports that social isolation and loneliness cost the U.S. economy an estimated $406 billion a year, in addition to approximately $6.7 billion in annual Medicare costs. The socially isolated are more likely to need skilled nursing care in a facility. This becomes very expensive to beneficiaries because of limitations in Medicare coverage.

A study by the University of Chicago found that loneliness can be as debilitating as anxiety or depression. High blood pressure, heart disease, obesity, and a weakened immune system, along with cognitive decline and Alzheimer’s, are linked to it, increasing the risk of premature death. The disabled, those with poor physical and mental health, single parents, and the financially insecure particularly suffer. Research shows that social isolation is as bad as smoking 15 cigarettes per day or drinking six alcoholic beverages a day. This is a serious and costly issue.

God created us to thrive within a community. Busyness, technology, and social media cannot substitute for in-person socialization. Without it, there is a price to pay:

Financial Behavior of the Lonely

A study out of Hong Kong reported that the lonely or rejected tend to put a greater value on money. They often make risky financial decisions that offer high rewards. They spend money, often sacrificing important resources, in an effort to secure social bonds, fit in, or be accepted. Those who place their identity in money feel pressure to be financially successful. They may forfeit time with family and friends to reach goals while damaging the quality of their relationships. Loneliness can also follow sudden wealth because people often don’t know who to trust. It is easier to build walls of protection than determine who is truly genuine.

“I cannot even imagine where I would be today were it not for that handful of friends who have given me a heart full of joy. Let’s face it, friends make life a lot more fun.”

–Chuck Swindoll

Some Helpful Action Steps

The lonely commonly withdraw, which only exacerbates the problem. One must step out of comfort zones to conquer loneliness. If a child or spouse is suffering, find ways to broaden their activities. Seek wise mentors, trusted friends, family members, or coaching to aid in social skills. Ask God for help, and see who He brings into your life. When we moved to a new city, my wife and I prayed for local couple friends, and the Lord graciously provided. Mayo Clinic reports that friendships enrich your life and improve your health.

Here are some helpful tips:

It takes work to make and maintain relationships, but it is so beneficial. Invite someone to walk and talk. Spend some money on an experience that is good for your mental health. Do not wait for someone to call or invite you somewhere. Reach out first. You may discover that person is just as hungry for friendship as you.

“The dearest friend on earth is a mere shadow compared to Jesus Christ.”

–Oswald Chambers

If you’re looking for a way to help others or make connections, consider starting a small group or volunteering. Here is a Crown resource that you might find beneficial. Thank you for the excellent question.

This article was originally published on The Christian Post on May 12, 2023.

Dear Chuck,

We have a budget, but the cost of groceries and eating out is ridiculous! Something has to change. What can we do? We are exceeding our food budget every single week.

Fed Up with Grocery Prices

Dear Fed Up with Grocery Prices,

You are correct. Something does have to change for almost all of us who are being pinched by the price of food. I am fortunate that my wife, Ann, who does research on all of my articles, is also a great grocery shopper, so I asked her to contribute her insights, which greatly helped my reply.

Has Greed Taken Over the Food Industry?

Hmm, supply-chain issues have been resolved, cost pressure from the war in Ukraine has eased, stores are stocked with inventory, compulsive pandemic shopping has ended, and employees gained higher wages, so why are grocery prices still inflated? Have you heard of “greedflation”?

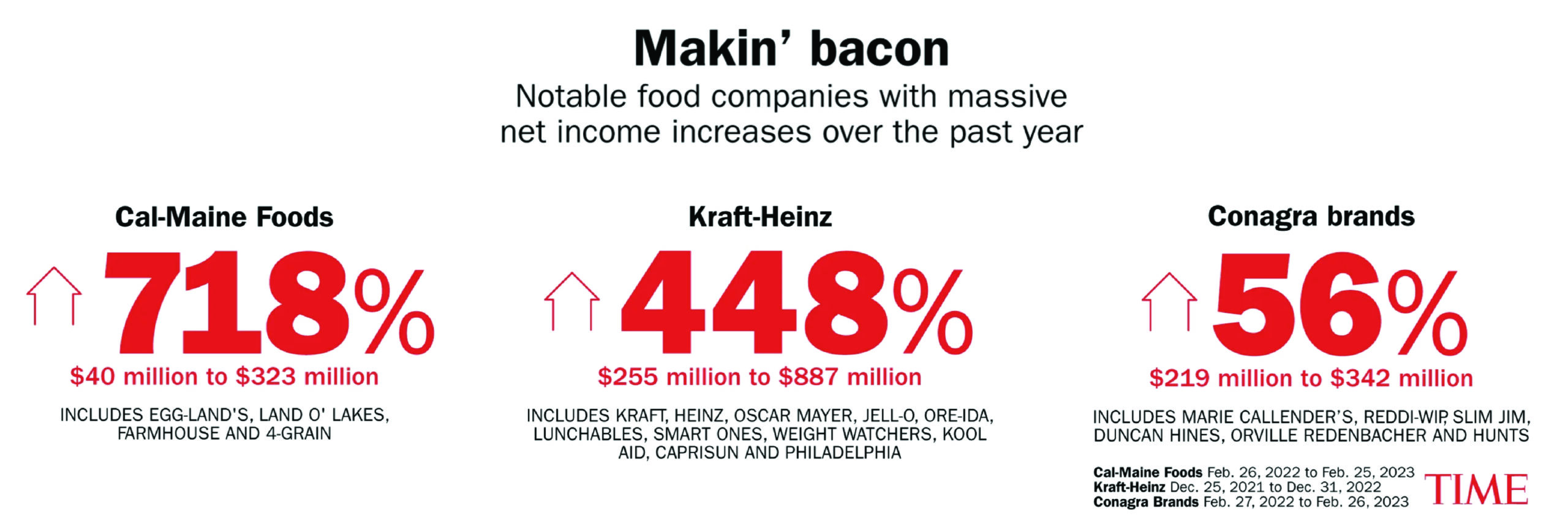

Eggs are 70% more expensive than they were a year ago, with many stores limiting purchases to two dozen. Other staples remain elevated in price, while only a few things have come down. Several explanations are possible. Mergers in the food industry have resulted in few competitors. Profit hoarding, or as some call it, “greedflation,” occurred when corporations amplified disruptions to their benefit. See the staggering numbers here or in the graphic from Time Magazine below.

Businesses know that people will pay more for what they want, so getting them to forfeit profits will be tough. The ultimate solution will come when leaders are willing to sacrifice millions (billions) of dollars in bonuses, perks, and salaries for the good of the nation. Inflation tends to be “sticky” or hard to get rid of. Don’t count on it going away soon; so in the meantime, you must get proactive.

Ideas from Ann, My Money-Saving-Grocery-Shopper Extraordinaire

One obvious way to reduce your bill is to go on a diet. Seriously!

Reduce your consumption of sugar, meat, soda, juices, alcohol, and prepackaged foods/snacks. Compare unit prices using a calculator if necessary. A shopping list app or shopping guide may be helpful. In addition, avoid eating out for a month, and see how much you save. Here are some other helpful hints:

Wonder what you should be spending? The USDA compiled a Thrifty Food Plan Cost guide.

The internet offers many budget-saving recipes. Bon Appetit even has a list of cheap dinner ideas.

Become an expert at saving money on groceries. Meet regularly with friends to share cost-saving tips and recipes. Notify one another of sales, and share items you find. Learn to make all that you can from scratch, from salad dressings to snacks. Involve the whole family, and praise each other’s attempts to fight this battle.

Try not to complain, especially in front of your spouse or children. Remember the Israelites whom God rescued out of Egypt? He provided for their every need, yet they failed to meditate on His goodness. They did not give thanks. Instead, they wept in self-pity and said, “Oh that we had meat to eat! We remember the fish we ate in Egypt that cost nothing, the cucumbers, the melons, the leeks, the onions, and the garlic. But now our strength is dried up, and there is nothing at all but this manna to look at.” (Numbers 11:4–6 ESV)

Being mindful of this, focus on what you do have. Ask God for help. Then give thanks, and celebrate discounted items or delicious cost-saving recipes you find. Enjoy potlucks with friends or neighbors. Enjoy a “Cheapest Meal Competition”—that must also be delicious! Try memorizing Psalm 100, and give thanks at every meal. Pray for those who literally have no food or can only afford one meal a day.

Thank you, Ann.

Economic Cycles

It has been said that the best cure for high prices is high prices. People tend to pull back spending when it no longer makes sense; thus, demand drops until prices also decline. By becoming more frugal during this time, your spending habits will help accelerate a price adjustment in the long run. Thank you for the question.

The Crown God Is Faithful devotional can offer some inspiring and practical Biblical wisdom in such uncertain times. You can subscribe to receive daily devotionals that will help transform your finances and provide much-needed encouragement. May it be a blessing!

This article was originally published on The Christian Post on May 5, 2023.

Dear Chuck,

I would like to eliminate our high interest credit card debt. What are your thoughts on taking out a HELOC to pay it off?

HELOC or NOT?

Dear HELOC or NOT?

Just to be sure readers know what we are talking about, HELOC stands for Home Equity Line of Credit. It is a line of credit that uses the equity in your home as collateral. Because of high interest rates and inflation, more and more homeowners are using a HELOC. The rates are usually more favorable than other forms of consumer debt, especially credit cards. This revolving line of credit is quickly replacing the older method of “cash out refinancing.” It can be helpful when used wisely because it gives homeowners access to equity to help meet cash flow needs—emphasis on the word wisely.

General Thoughts on HELOCs

Paying off credit card debt can be a good use of a HELOC for the disciplined spender. You must strive to reduce the use of credit cards and faithfully pay off the balance every month to avoid accumulating high cost debt again. Know, too, that if repayments of the loan are missed, you face the danger of foreclosure. So your decision must first be based upon your personal discipline to keep within a budget and a plan.

A home equity loan pays a lump sum at a set interest rate, whereas a HELOC allows funds to be taken as needed. This keeps monthly payments lower and helps avoid unnecessary debt. Some nominal costs are involved, and interest is only charged on what is borrowed. However, the rate is typically variable, and the payout period ranges from 10 to 20 years.

To qualify, verifiable income, good credit, and considerable equity are needed. Reliable payment history may be investigated. See Bankrate.com or Forbes for current HELOC rates. Lenders will use Loan-to-Value (LTV), Combined Loan-to-Value (CLTV), and Debt-to-Income (DTI) ratios as well as other factors to determine individual interest rates and the amount eligible to borrow.

Terms to Know

Pros

Cons

When to Use

When to Avoid

HELOC or NOT?

The best use of a HELOC is to increase property value. The risk is that one’s home is used as collateral. If convinced this kind of borrowing will be beneficial, compare rates and fees of different lenders. Understand the repayment structure and all requirements before signing any paperwork. What is the prepayment fee and policy? Does a low monthly rate come with a balloon payment? Will a shorter repayment timeline grant a lower rate? Is there an inactivity fee? Does your bank or credit union offer member discounts?

Once the loan begins to amortize, monthly payments can be painful unless the borrower is disciplined and prepared. That is why I recommend that a payback plan be in place before borrowing any money.

“The rich rules over the poor, and the borrower is the slave of the lender.” (Proverbs 22:7 ESV)

The Bible warns of debt becoming a form of slavery. Avoid presuming on the future—especially during uncertain economic times. And do not borrow to simply keep up with friends or neighbors. While a HELOC can be helpful in extreme cases, I always think it is best to make a plan to pay off the debt causing you pain without creating more debt. For most people, this is a safer and wiser path to financial freedom.

My bottom line: paying off high debt with a low rate HELOC can be wise if the Lord directs you in this way. Pray for wisdom.

Christian Credit Counselors is a trusted source of support in assisting people with getting on the road to financial freedom. Reach out to them today; they may be of great benefit to you.

This article was originally published on The Christian Post on April 28, 2023.

Dear Chuck,

My husband and I believe America has lost its way. I see so much pride, division, financial fear, and greed that I wonder if we can even recover. How can an individual make a difference?

Overwhelmed by America’s Decay

Dear Overwhelmed,

You, like so many others, are expressing a sense of gloom that has come over the nation. As believers, we are inwardly groaning at what we see happening to the nation that once stood as a beacon of light to a dark world. And your concerns are reflected in the data.

According to findings in a recent survey by the Wall Street Journal, traditional or core American values are declining, while the value placed on money is increasing:

The loss of values that unite and the increase in the value placed on money are dangerous trends. Most tension, family friction, strife, anger, and frustration are caused directly or indirectly by money. Christians have access to Biblical financial principles, but do we implement them? Many do not—either by choice or ignorance.

Love Is Not Proud

C.S. Lewis called pride “the great sin.” He said, “Pride is spiritual cancer: it eats up the very possibility of love, or contentment, or even common sense.”

If we humble ourselves before the Lord, individuals can make a difference, and God has given us clear instructions on what we are to do!

God is love and desires that we use what He provides, whether great or small, to love Him and others. Jesus said, “You shall love the Lord your God with all your heart and with all your soul and with all your strength and with all your mind, and your neighbor as yourself.” (Luke 10:27 ESV) This applies to every area of our lives—even finances. Do you know anyone who models this well? If not, can I challenge you to become that person? The world needs examples!

Below are three ways you can begin to make a difference.

Financially Love Your Family

No matter how much our culture drifts away from God, we are to care for the needs of our families. This includes their financial, spiritual, and emotional needs:

Financially Love Your Church

We can plug into our local, Bible-believing, gospel-centered church and support its mission and programs. Change happens in community, and the church was created to strengthen one another as we serve others in love:

Financially Love Your Neighbors

We are to care for one another in word, deed, and dollars:

America Is Not Our Home

The core problem is that the world has been ravaged by sin since Adam and Eve disobeyed God’s commands. We need personal redemption from the sin that has controlled us and a kind and generous heart toward those who remained trapped in the darkness.

While we are blessed to live in America, I am constantly reminded that it is only our temporal home. Let’s do all we can to be salt and light until our journey here is complete.

The Crown God Is Faithful devotional can offer some inspiring and practical Biblical wisdom in such uncertain times. You can subscribe to receive daily devotionals that will not only help transform your finances but will also provide much-needed encouragement. May it be a blessing!

This article was originally published on The Christian Post on April 21, 2023.

Dear Chuck,

Our finances are stretched so thin that I am stressed out all the time. We live on a budget, but my husband and I both need some hope that it will not always be this way.

Living on a Financial Cliff

Dear Living on a Financial Cliff,

There is certainly reason for hope, so hang on!

Let’s put your challenges in a current economic context and then a Biblical context before I offer some practical tips to help you through this painful time.

Economic Context

With the lingering impact of inflation, a new CNBC survey reports that 70% of Americans say they, too, are feeling financial stress, and 58% report they are living paycheck to paycheck. The report pointed to several specific concerns, including a lack of savings and a dependency on debt.

“People are worried that the money they’ve saved won’t last and are worried they’re going to have to lean more on their credit cards and other sources of debt just to get by,” said Bruce McClary, a senior vice president at the National Foundation for Credit Counseling.

With rapidly increasing costs, higher interest rates, and a sense of economic uncertainty in the air, many are feeling like their finances are balanced on a razor’s edge with no margin for error.

Biblical Context

The Bible is full of people who had to face incredible amounts of stress. It is also full of principles and truth that help us to reframe our present circumstances. I am reminded of Romans 8:18–21:

I consider that our present sufferings are not worth comparing with the glory that will be revealed in us. For the creation waits in eager expectation for the children of God to be revealed. For the creation was subjected to frustration, not by its own choice, but by the will of

the one who subjected it, in hope that the creation itself will be liberated from its bondage to decay and brought into the freedom and glory of the children of God. (NIV)

We live in a fallen world—in bondage to decay—because of mankind’s disobedience to God, but a promise of freedom and redemption awaits those who are children of God. Considering our eternal future, our present trials and tribulations are insignificant. Remember to keep your present cares and burdens in the context that this is not our home. We temporarily manage what God provides and seek to be faithful until we have finished our race.

Help in Reducing Your Financial Challenges

Three very practical steps will help you reduce the immediate pain you are in.

First, no matter how much or how little income you have each week or month, be sure that you are spending less than that amount. Think of the old game of limbo, where you have to bend your body to get under a bar without knocking it off. The bar represents your income. Your attempts to get under it represent your control over your spending. That is why a budget is so very helpful. You can adjust your expenses to ensure that you never exceed the height of the bar (your weekly or monthly income).

Second, build an emergency savings fund. You need at least $1,000 set aside to help with unexpected expenses. That is the bare minimum. Set a goal of saving three months of overhead. Emergencies always happen, so this is non-negotiable. In the CNBC survey, most of those who report living paycheck to paycheck say they do not have any money saved. This is like flying through the air on a trapeze bar without a safety net. It is scary! Crown has some free tools to help you get that accomplished. Perhaps you need to adjust your budget. You might benefit from our budgeting resources and a coach.

Finally, make a plan to reduce your debt and break any dependence on credit cards, store accounts, buy-now-pay-later plans, or payday loans. The largest expense in most American budgets today is interest expense on debt. Just imagine how free you would feel without debt hanging over you each month. We partner with Christian Credit Counselors to help free people from this burden.

Thank you for writing. Please know that we want to help! May God give you His peace and the freedom you so desire.

Christian Credit Counselors is a trusted source of support in assisting people with getting on the road to financial freedom. Reach out to them today; they may be of great benefit to you.

This article was originally published on The Christian Post on April 14, 2023.

Dear Chuck,

It sure looks like Larry Burkett’s book “The Coming Economic Earthquake” is happening before our very eyes! Is this the big one that he warned us about?

Economic Observer

Dear Economic Observer,

It would be hard to overestimate the number of times I have been asked this question in the past 22 years that I have worked with Crown. So my answer is always the same, “No, not yet.” Let’s review a few key points from Larry’s book that you referenced, and then I will add my thoughts about the times we are in now.

The Coming Economic Earthquake

Larry authored his best-selling book in 1991. Within the pages, Larry discussed economic history, the US government’s violations of Biblical principles of sound money, and the plausible scenario for what could happen to the debt-fueled American economy. He was careful to say that he was not a prophet, nor could he tell the future, but he was compelled to warn about the possibility that America’s economy could be destroyed within ten years of the publication of his book. That was 32 years ago.

Fortunately, the American economy has survived a number of very significant challenges since then, including the Great Financial Crisis of 2007–2008. Larry’s timing was way off. He was labeled an alarmist, and many discredited his thesis altogether. But let’s take a look at the argument that Larry made and compare it to where we are now, three decades later.

At that time, an estimated 20% of the annual budget deficit was funded by foreign investors. That number has increased to 30% in the estimated federal budget proposed for the coming fiscal year.

An article on Schiffgold says: “Since March 2020, the federal government has added $4.7 trillion to the national debt. And as WolfStreet put it, the Federal Reserve went ‘hog-wild’ with debt monetization. . . . At some point, the central bankers will be faced with a choice – continue monetizing the debt and inflating the money supply or deal with surging inflation by letting rates rise. It can’t do both. And neither of these choices will play out well for the American people.”

As Larry Burkett said, “What is the national debt but the visible indicator of gross fiscal mismanagement on the part of our leaders?”

Where Are We Now?

All of the warning signs that Larry wrote about are certainly still in play. In fact, they have been every year since he first penned the book; however, the American economy has shown incredible resilience to shocks and has expanded more than Larry may have ever dreamed or imagined. Through economic expansion and federal monetary policy, “the big one” has been staved off far longer than Larry and many other experts thought would be possible.

In Deuteronomy 28, God gave clear economic instructions to His chosen people: “And if you faithfully obey the Lord your God, being careful to do all his commandments that I command you today, the Lord your God will set you high above all the nations of the earth.” The promises for obedience that follow are for blessings of abundance and strength, including verse 12b: “…And you shall lend to many nations, but you shall not borrow.” However, the curses for disobedience would undo all their progress, including verses 43–44: “The sojourner who is among you shall rise higher and higher above you, and you shall come down lower and lower. He shall lend to you, and you shall not lend to him. He shall be the head and you shall be the tail.”

America was the largest creditor nation in the world in the late-‘70s but flipped to the largest debtor nation in the world by the mid-’80s. Our nation is facing an ever-increasing mountain of debt and a potential banking crisis while attempting to control inflation and fight off a recession or worse. I cannot help but believe it is all related to our declining interest in obeying God. The heart of our economic problem is truly the heart problem of our people. Until we believe God is needed here, we should not expect to avoid an economic crisis.

An economic earthquake will come; we just don’t know when.

In such uncertain times, the Crown God Is Faithful devotional can offer some inspiring and practical Biblical wisdom. You can subscribe to receive daily devotionals that will help transform your finances and provide much-needed encouragement. May it be a blessing!

This article was originally published on The Christian Post on April 7, 2023.

Dear Chuck,

This banking crisis has me nervous. How bad is it? Should we trust our small regional banks? Where should we put our money?

Widowed and Worried

Dear Widowed and Worried,

As you are, we should all be concerned and paying attention. This is a very real and dangerous economic challenge.

What Happened?

Silicon Valley Bank and Signature Bank are the 2nd and 3rd largest bank failures in U.S. history, topped only by Washington Mutual, which collapsed in the financial crisis of 2008. 94% of Silicon Valley’s deposits were uninsured, as were 90% at Signature. SVB had a concentration of tech startups, and Signature had a significant number of holders of cryptocurrencies. Together, the banks held combined assets of nearly $320 billion.

The assets at SVB were too heavy in long-term treasury bonds that were purchased before the Fed raised interest rates. Their value decreased as investors preferred new bonds that earn higher rates. Rather than analyzing the market value of the bonds, the accounting value gave a false portrayal of the bank’s status. To calm a run on banks, the current administration guaranteed uninsured deposits at both banks, and the Federal Reserve announced a lending program for institutions needing to borrow money to cover withdrawals. Over time, the FDIC fund will have to be replenished, possibly by a “special assessment” on banks that customers will undoubtedly have to pay in fees.

“The principle of sound money was ignored by the Fed. SVB violated principles of diversification and prudence. It set aside its fiduciary duty to steward the assets of others and focus on business, not ideology.” (Jerry Bowyer)

Bank Contagion

I don’t pretend to be an economist or understand the complexity of the current banking crisis. I do know that the First Republic Bank is also distressed and had to be rescued by its rivals. Credit Suisse, a century-old European stalwart bank, had to be rescued by rival UBS (United Bank of Switzerland) for it to remain solvent. While some are calling for more bank reform and regulation as the solution, the Federal Reserve is working overtime to stop runs on banks and ease the fears of depositors like you and me. By some indications, as of this writing, those measures are working to diminish the fear of a complete banking meltdown.

What To Do with My Money Now?

An in-depth article in Fortune Magazine gives insight into the history of bank failures and some helpful advice on managing your bank accounts. Here are a few tips from my perspective:

The Economic Finger Trap

One side of our economic challenges can be solved by controlling inflation, which requires raising interest rates. The other side can be controlled by increasing liquidity in our banks, thereby increasing inflation. Some say the Fed will be choosing between generational inflation and another banking crisis in the days ahead.

“A prudent person foresees danger and takes precautions. The simpleton goes blindly on and suffers the consequences.”

Proverbs 27:12

The coming days will be interesting indeed. This should be a wake-up call to millions of people, especially Christians. We need to live prepared for any of these possible scenarios.

The Crown God Is Faithful devotional offers inspiring and practical Biblical wisdom. You can subscribe to receive daily devotionals that will help transform your finances and provide much-needed encouragement. May it be a blessing!

This article was originally published on The Christian Post on March 24, 2023.

Dear Chuck,

My husband and I bought our first home in an older neighborhood where young families are choosing to live. We put 10% down and now want to build equity in our home, but we have more time than money. What are the best ways to build “sweat equity” as “do-it-yourselfers”?

First-Time Homeowners

Dear First-Time Homeowners,

Congratulations! I am happy for you and want to give some solid advice to a question that is more complicated than it may seem.

Get Rid of the PMI First

Because you qualified for a mortgage without having the desired 20% down payment, you are now required to have Private Mortgage Insurance (PMI). Getting rid of this should be your first and highest priority, as it adds costs and impedes your progress in actually owning your home. Nerd Wallet offers great advice and options for your consideration. Regardless of the method you choose, get out of it before you start any projects on building equity.

Building Equity

Many people have moved over the past few years, and some hope to become homeowners this year. The value of your home and the ability to build equity can fluctuate wildly by region and economic conditions, so let’s discuss the topic of equity.

Equity is the amount of the home that actually belongs to you. If your home is worth $400,000 and you owe $150,000, then your equity is $250,000 (market value – loan balance = equity). Your equity grows as the value increases and debt decreases. Why is equity important?

Not All Real Estate Is a Good Investment

It is true that historically the best pathway to building personal assets in America has been homeownership. But that is a very broad assumption. I have counseled many young couples who have lost their shirts by buying a home, especially when sinking money into a project that they may never recover. In fact, this happened to me when Ann and I were first starting out as a couple. Let’s help you avoid that by being very careful with the decisions you make to create “sweat equity.”

Improve Value and Build Equity

Any improvements or upgrades should fit the neighborhood to ensure you get the value back at resale. Do not overspend. You are much better off having the least expensive home in a nice neighborhood than the most expensive home in a so-so neighborhood!

Upgrades vary depending on the location and home values in your neighborhood. Know what upgrades will truly benefit the home. Check with realtors or appraisers. Don’t ignore problems. Maintain instead of waiting to repair. This is a basic financial principle of home ownership. Even though you want new countertops, a leaky roof must be repaired or replaced because it protects the entire house for decades to come. Adding some paint will likely be a much better investment than a swimming pool. Know your market before deciding where you will spend money and time on improvements.

Any work you do yourself can greatly increase your equity. Make a plan, set goals, and then set aside time and money for the projects. Take your time, and shop sales. YouTube is a great source of valuable instruction. Recruit friends to help you, and be willing to return the favor. It makes the work more rewarding and builds a tight community. I have practiced this with neighbors wherever we have lived.

Sometimes value is gained by adding square footage via an attic or basement. This is often less costly than actually adding on to the house. Again, it depends on location. A garage apartment or guest house may increase a home’s value and be an added source of income.

Impact on Neighborhood

People will notice the care you put into your property. Your work may encourage neighbors to do likewise. This can improve the value of your entire neighborhood.

Homeownership requires adequate emergency savings. An older home may have really strong bones, but maintenance and repairs are a fact of life. Stay on top of these. Do not procrastinate when a sign of a problem appears. Stay ahead of any issues!

Here are a few good resources:

Caring for your home means you are always in a position to sell should the need or desire occur.

Keep an eye on the market, and do not overdo it. Continue to replenish your emergency funds. Care for your home as if it were the Lord’s. Make it a place to welcome others and a place of rest for your soul. If done right, your time and money will likely increase market value and equity over time.

Another important way to make strides in your financial health is to diligently pay off credit card debt. Christian Credit Counselors is a trusted source of support. They specialize in assisting people with getting on the road to financial freedom.

This article was originally published on The Christian Post on March 17, 2023.