Dear Chuck,

Since the FTX debacle, do you think the crypto market has been ruined?

Cautious Investor

Dear Cautious Investor,

I don’t think cryptocurrencies are ruined, but the idea that they are a trustworthy asset is severely damaged. Let’s look at a few details of FTX’s collapse and then some biblical principles for investors.

A Historic Destruction of Wealth

30-year-old Sam Bankman-Fried (SBF) lost a $16 billion fortune in less than a week. He resigned as chief executive on November 11th, the same day the cryptocurrency exchange FTX filed for bankruptcy. The entire staff of the FTX Future Fund resigned as well.

Before SBF’s empire collapsed, he spent millions in the Bahamas to fund a lavish lifestyle. He purchased a $40 million penthouse and a 52-foot yacht and spent tens of thousands of dollars every week to feed his staff and guests. FTX supposedly employed 300 people on the island. Interestingly, SBF received a $1 billion personal loan from one of his own firms.

Bloomberg called this debacle “one of history’s greatest-ever destructions of wealth.” SBF’s belief in “effective altruism,”the theory of making as much money as possible in order to do as much good as possible, is contrary to what the Bible teaches. It places man as the solution to man’s problems, as opposed to focusing on man’s need for a Savior and Redeemer. In SBF’s case, money was used as a guise for greed, selfishness, and virtue signaling.

Money Flows Toward Trust

Confidence is the most important aspect of any investment decision. We choose banks, advisors, investments, and even our relationships based on the intangible yet irreplaceable value of trust. I have often said that money flows toward trust just as water rolls downhill. That is the basis of how you and I manage money. Let me explain with a simple example.

You ask your teenage son to run to the grocery store to pick up a gallon of milk, a loaf of bread, and a dozen eggs, so you give him a $100 bill and ask him to bring you the change. (My illustration is before the recent rash of inflation.) He is eager to run the errand because he can drive the family car. It takes a while, but he finally returns with the milk, bread, and eggs. However, when you ask for your change back, he says there isn’t any. He explains that he is not sure what happened, but it was more expensive than his mom thought. While there would be some debate about what really happened, one thing is for sure. She will not give him a $100 bill to go to the grocery store for her the next time she needs milk, bread, and eggs!

In his piercing admonition in Luke 16:10–12, Jesus taught us that He manages funds based upon trust as well:

“Whoever can be trusted with very little can also be trusted with much, and whoever is dishonest with very little will also be dishonest with much. So if you have not been trustworthy in handling worldly wealth, who will trust you with true riches? And if you have not been trustworthy with someone else’s property, who will give you property of your own?”

In this teaching, we are the teenager with the $100 bill to run the errand. We are expected to be fully trustworthy with the Lord’s money if we expect to be trusted with true and better riches.

It is said that trust is the one thing in life that is the hardest to earn and the fastest to lose. The Lord calls us to be completely honest and trustworthy in all ways.

Future of Crypto Assets

FTX is not a crypto but a crypto exchange. However, the loss of trust in FTX and other exchanges that may have similar problems has had a contagious spread of fear among those who hold actual crypto assets. I appreciate John Mauldin’s perspective in his recent newsletter, Digital Shiny Objects. I recommend the entire article to you. Here is an excerpt:

I haven’t written much about crypto because, quite frankly, I’ve never felt the attraction. I’m not against the concept; I understand the philosophical libertarian argument. But I keep trying to find a “use case.” Yes, I can avoid public/government scrutiny of my financial activities but so can all kinds of bad actors. I trade the inherent problems of fiat currencies for a different set of problems.

Cryptocurrencies can be extraordinarily useful for people in emerging countries with problematic currencies. But if you are in most of the developed world, the volatility and risk of cryptocurrencies has so far been greater than that of your local currency. Yes, the dollar is depreciating due to inflation. I can manage that with reasonable planning. Using Bitcoin or another cryptocurrency simply changes my risk exposure.

Beware of the Lure

The Bible has much to say about the lure of riches and how easily we can be led astray. It is good to be a cautious investor not only to protect yourself from scams, rip-offs, and poor returns but also from being controlled by your own greed and covetousness.

“But godliness with contentment is great gain, for we brought nothing into the world, and we cannot take anything out of the world. But if we have food and clothing, with these we will be content. But those who desire to be rich fall into temptation, into a snare, into many senseless and harmful desires that plunge people into ruin and destruction. For the love of money is a root of all kinds of evils. It is through this craving that some have wandered away from the faith and pierced themselves with many pangs.” (1 Timothy 6:6–10 ESV)

“Do not be overawed when others grow rich, when the splendor of their houses increases; for they will take nothing with them when they die, their splendor will not descend with them.

Though while they live they count themselves blessed—and people praise you when you prosper—they will join those who have gone before them, who will never again see the light of life. People who have wealth but lack understanding are like the beasts that perish.” (Psalm 49:16–20 NIV)“Whoever trusts in his riches will fall, but the righteous will flourish like a green leaf.” (Proverbs 11:28 ESV)

The Crown Stewardship Podcast can be a valuable tool to provide wisdom and insight into how you can effectively steward God’s resources—both time and money. You can subscribe for alerts of new episodes. I hope you find it beneficial.

This article was originally published on The Christian Post on December 2, 2022.

Dear Chuck,

When it comes to our finances, we live with good intentions but put off budgeting and planning until we face another crisis. My husband and I want to break our cycle of procrastination, crisis, firefighting, and then back to procrastination. We need help to stay focused.

Painful Procrastination

Dear Painful Procrastination,

You have come to the right place! I became an expert procrastinator in college. Like you, I often ignored due dates and warnings. I nearly failed a language course because I put off going to the lab until it was almost too late. My professor scolded me for trying to cram all of my practice sessions into the final two weeks of the semester, but he showed mercy! I tend to have an optimistic view about everything, which makes me slack in planning. Most of my progress has come through learning from my wife, who is always thinking and planning ahead. The Bible also speaks to the issue!

Don’t be too hard on yourself. Procrastination is part of our fallen nature. We know taxes are due April 15th every year, but millions wait until the final days and hours to file tax returns. We know a car must have oil and gasoline to operate properly, but we tend to ignore the warning lights. We know Christmas comes every December, but the malls will be full of shoppers on December 24th. We know our bills are due on time every month, but we tend to wait until we are under pressure to take action.

Cost of Procrastination

Procrastination costs us in numerous ways. As you pointed out, it is stressful and leads to a self-inflicted crisis. Let’s examine just how much it costs to put off the discipline of careful planning.

Peace

Time

Quality

Money

Making temporary sacrifices in your lifestyle now will positively impact your future. Allow these verses to speak to your heart:

“The prudent sees danger and hides himself, but the simple go on and suffer for it.”

(Proverbs 22:3 ESV)“Know well the condition of your flocks, and give attention to your herds, for riches do not last forever; and does a crown endure to all generations?” (Proverbs 27:23–24 ESV)

Take Weekly Action

Invest in Your Future

The Bible says that where our treasure is, there our hearts will be as well. Investing in your training or a system to keep you on track makes you much more likely to follow through. Possibly, you can make Christmastime a turning pointfinancially. How about your husband and you give each other the gift of a Crown budget coach or take an online class together? We receive testimonies from couples at all stages of life who have finally overcome their lack of financial progress by simply hiring one of our coaches.

I hope this helps you get going! Merry Christmas to you and yours.

This article was originally published on The Christian Post on December 9, 2022.

Dear Chuck,

I always thought a small diversification into cryptos would protect me from the collapse of fiat money, but now with the collapse of FTX, I am losing trust in the entire concept of currency. What should I do?

Losing Trust in Currencies

Dear Losing Trust in Currencies,

As painful as it is to be deceived and lose trust in an institution, an investment firm, or any form of currency, it was misplaced trust to begin with. The Bible warns us never to love money. Few that I have ever known have admitted to it. However, we often have to come to grips with the fact that placing our security, confidence, or trust in it is not too dissimilar to loving money.

Hebrews 13:5–6 is one of my favorite passages regarding money:

Keep your lives free from the love of money and be content with what you have, because God has said, “Never will I leave you; never will I forsake you.” So we say with confidence, “The Lord is my helper; I will not be afraid. What can mere mortals do to me?”

The implied message here is that money will leave you and forsake you, but only Jesus will never do that. We are to keep our hope, security, and confidence in Christ and His kingdom, even while seeking to be faithful stewards of the resources we temporarily manage on Earth.

The Crypto Debacle

Sam Bankman-Fried, who goes by SBF, was arrested earlier this week. His name and image will forever be an icon for the breach of trust. He is at the center of the unbelievable cryptocurrency scandal, leaving millions of people angry, fearful, and disillusioned—not just you. He faces federal criminal charges, including wire fraud, wire fraud conspiracy, securities fraud, securities fraud conspiracy, and money laundering.

The Securities and Exchange Commission (SEC) announced separate charges for violating the Securities Act and the Securities Exchange Act. The complaint says, “Throughout this period, Bankman-Fried portrayed himself as a responsible leader of the crypto community. He touted the importance of regulation and accountability. He told the public, including investors, that FTX was both innovative and responsible. Customers around the world believed his lies, and sent billions of dollars to FTX, believing their assets were secure on the FTX trading platform.”

SEC Chair Gary Gensler stated, “We allege that Sam Bankman-Fried built a house of cards on a foundation of deception while telling investors that it was one of the safest buildings in crypto.”

Ponzi scheme king Bernie Madoff was sentenced to 150 years in prison. It is possible that prosecutors will make an example of SBF’s crimes.

Expect More Government Regulation

Every time a disaster like this happens, government agencies seek to increase regulation in order to rebuild trust. Mike Novogratz, bitcoin bull and Galaxy Digital CEO, said, “The FTX debacle has created a ‘deficit of trust’ in the whole industry.” In an interview with CNBC, he shared, “This is about transparency and disclosure, in lots of ways. Our industry has failed to self-regulate. I think the money side of crypto, companies like ours that buy and sell and lend and do derivatives, are going to get regulated and should be.”

Dan Dolev, a Mizuho analyst, explains, “What FTX told you is that one day you could be worth the world, and the second day you could be worth nothing, and I think consumers are going to be very scared.” Market share gains by Coinbase will be “very minimal in the greater scheme of things” because of lack of trust.

Yesha Yadav, professor of law and director of diversity, equity and community at Vanderbilt University, said, “The level of disillusionment and disappointment and sense of feeling deceived by FTX is so deep because it was seen as one of the most compliance-friendly institutions in the crypto economy and one that would be leading the regulatory efforts.”

John J Ray III, the U.S. attorney who took over as CEO of FTX, has been stunned by the incompetence of SBF and his executive team. Ray declared that he has never seen “such a complete failure of corporate controls and such a complete absence of trustworthy financial information as occurred here.” He told Congress Tuesday, “This is just plain, old-fashioned embezzlement, taking money from others and using it for your own purposes. This is not sophisticated at all.”

In October, cryptocurrencies stolen by cybercriminals set a new record of over $3 billion. This was prior to news of the FTX debacle released in November. Will regulation solve the problem? Was it not the lack of regulations that originally drew people to cryptocurrencies?

Who to Trust

According to Crown’s late founder, Larry Burkett:

Trickery, double-dealing, lying, cheating, and subterfuge are all the practices of one who deliberately deceives. The most devastating loss associated with deceit is the dulling of spiritual awareness. Guilt associated with a known deception will cause the Christian to withdraw from God’s presence. Once withdrawn, subsequent deceptions become easier, less conviction is felt, and life is full of defeat and frustration. Deception destroys trust and leads to hypocrisy and a critical spirit. No one is immune to the temptation to deceive, particularly when money is concerned. God’s Word gives us guidelines for making decisions in spite of our normal reactions.

“It is better to take refuge in the Lord than to trust in humans.

It is better to take refuge in the Lord than to trust in princes.”

Psalm 118:8–9 ESV

Are we willing to put God totally in control of our finances? He promises to satisfy our needs, so are we willing to trust Him with everything? What about trusting Him with our losses?

“Trust in the Lord with all your heart, and do not lean on your own understanding.

In all your ways acknowledge him, and he will make straight your paths.”

Proverbs 3:5–6 ESV

My suspicion is that your crypto losses have been painful. We must all trust God regardless of what we have or do not have. That does not mean we stop working, giving, saving, spending, or investing. We do our part to be faithful with the temporal resources we have but only store up for ourselves treasures in Heaven.

The Crown Stewardship Podcast can be a valuable tool to provide wisdom and insight into how you can effectively steward God’s resources—both time and money. You can subscribe for alerts of new episodes. May we all be found faithful stewards of the Lord’s resources.

This article was originally published on the Christian Post on December 16, 2022.

Dear Chuck,

We’ve made financial mistakes in the past and want to improve our credit score in the New Year. What steps should we take, and what should we avoid?

Managing Our Credit Score

Dear Managing Our Credit Score,

This is a great goal for the New Year, and it will impact almost every area of your finances!

Recently, my 89-year-old father and I were comparing our credit scores. I was pretty proud of mine until he told me his. His was nearly perfect, which is a rare feat! I wondered, “How in the world was his score better?”

He knew a trick that I had not implemented: improving his credit utilization ratio. By reducing the limits of available funds on his credit cards, his credit utilization ratio proved better than mine. In other words, if you have very little debt and very reasonable limits on your available debt, your score improves. I knew that principle, but I had not acted on it yet.

Managing Your Credit Score

Your credit score is a three-digit number that grades your credit and bill payment history. Scores range from 300 to 850. These are calculated by the three major consumer credit bureaus—Equifax, Experian, and TransUnion—using information from lenders, credit card issuers, and other financial institutions. Higher scores demonstrate a lower risk to lenders. Scores of 800–850 are exceptional, 740–799 are very good, 580–669 are fair, and 300–579 are poor. My Dad’s score, by the way, was 842.

Your credit score is basically your financial reputation. Lenders determine the risk of repayment based on credit reports. Higher scores reduce borrowing costs over your lifetime because lower interest rates are granted. Scores affect a mortgage’s APR (annual percentage rate), interest rates on loans, and the cost of car and home insurance; they also determine whether a landlord will rent to you.

Some factors used in scoring include:

Emergencies can destroy credit scores. Business failure, job loss, or medical emergencies present costs that many cannot cover in a reasonable time. Unfortunately, your credit report can be damaged for years. Bankruptcies remain on record for seven years (Chapter 13) or ten years (Chapter 11). With time, you can improve your score, so do not lose hope. Follow these tips:

Canceling cards without reason can actually hurt your score. In some cases, an old card on file, even if not used anymore, demonstrates your experience in borrowing. Tuck it away in a safe place, and simply do not use it.

Check, Freeze, and Unfreeze Reports

Check your credit reports annually. Put a reminder on your calendar, and do not neglect to do it. Errors are common, and you must act to fix them. AnnualCreditReport.com grants access to a free report each year.

It’s important to freeze your credit reports to protect you from thieves opening new accounts in your name. When frozen, your information will not be given out for credit approval. You have to unfreeze it if you need to allow access to your report. You can do this yourself.

TransUnion (888-909-8872)

Experian (888-397-3742)

Equifax (888-298-0045)

Work to repair your credit score on your own. There are many credit repair companies and free credit report companies that are scams. Here are common red flags:

For Those with No Credit History

Those with no credit history should consider a secured credit card through a bank or credit union. A deposit is held as collateral until the account is closed. Try to avoid annual fees, and read the fine print to understand the contract.

Credit-builder loans are offered by credit unions, banks, and some online lenders. The money you agree to borrow (typically $300 to $1,000) is deposited into a bank account and held by the lender. Monthly principal and interest payments are required, which build a nest egg while also building credit. Once the loan is repaid in full, the funds are then yours. Make sure they report payments to the three major consumer credit bureaus before applying.

Truth and Borrowing

The Bible shows the way to an excellent credit score. Borrowing is not prohibited. God simply lays down clear guidelines for our protection: (1) credit should never be normal for God’s people; (2) credit should never be long-term; (3) never sign surety (an obligation to pay) without an absolutely certain way to pay.

Your stewardship score is much more valuable than your credit score. Paying off a lot of debt quickly can negatively impact your credit score. But it’s more important to live in the freedom of being out of debt than to have a perfect credit score. “You were bought at a price; do not become bondservants of men.” (1 Corinthians 7:23 ESV)

Do these things, and you likely will never really need to worry about your credit score. In the meantime, take care of your finances so if you ever do have to borrow, you can qualify for the very best repayment terms. Hopefully, one day you may have a higher credit score than my Dad.

If credit card debt is a source of financial pain for you, consider contacting Christian Credit Counselors. They are a trusted source of help toward financial freedom.

Note: Since I answered this question in a lengthy Lifeway article in 2021, I refer to much of that original content in my reply above.

This article was originally published on The Christian Post on December 23, 2022.

Dear Chuck,

We want to start the New Year right when it comes to our finances. Beyond a “get out of debt” resolution, what are the best moves to get us on track?

Looking for Financial Tips

Dear Looking for Financial Tips,

My best tip is to practice the simple but powerful act of daily discipline.

For example, years ago, I struggled to cut back on my sugar intake. I was frustrated with my physical state and knew that I could do better with a little discipline. So, on January 1st, I resolved to eliminate as much sugar as possible from my diet: no desserts, candy, or sugary beverages. Each day, I learned to say no to what I wanted (sugar) to gain what I needed for tomorrow (better health).

I renewed my resolution each morning for the entire year. This small victory brought great rewards and taught me to exercise self-control in other areas of my life. Let me repeat that daily formula:

Saying No to What I Want Today = Gaining What I Need for Tomorrow

Start Small

If you can be disciplined in just one area of your life, you can learn to be disciplined in all areas of your life—but it must start with one. This principle directly relates to your finances. To reach financial goals, you must start with a simple discipline that you faithfully practice one day at a time. This small daily effort exercised over a long period of time will enable you to achieve more than you can imagine when it comes to your financial goals. Stated another way, “Little habits have big results.”

Spiritual Discipline

“Whoever can be trusted with very little can also be trusted with much, and whoever is dishonest with very little will also be dishonest with much. So if you have not been trustworthy in handling worldly wealth, who will trust you with true riches?” (Luke 16:10–11 NIV)

“Commit your work to the Lord, and your plans will be established.” (Proverbs 16:3 ESV)

“But the fruit of the Spirit is love, joy, peace, patience, kindness, goodness, faithfulness, gentleness, self-control; against such things there is no law.” (Galatians 5:22–23 ESV)

What, Why, How, Celebrate

The ultimate purpose of a believer’s financial goals should be to glorify God. Goals will take on greater significance if you aim higher than simply keeping yourself afloat. Put your spending plan on paper (or in a spreadsheet or banking app) in order to view the state of your finances more clearly. Determine what you want to achieve in 2023. The “why” of your plans will keep you motivated. Write down your “why.” Good intentions become a plan only when written down and acted upon. Now write down how you will make progress every day. Next, plan to celebrate once you achieve each step of your goals. Remember, faithful steps will become lifelong habits.

What is the goal?

Why is the goal important?

How will you act on the goal daily?

Plan your favorite celebration once the goal is reached.

Financial Goals to Consider

Here is the step-by-step plan I recommend, in order of priority.

Practice this habit: give first, and save second. If you do this before spending, your finances will begin to dramatically improve.

Don’t Give Up!

Give yourself some grace to learn new disciplines and establish healthy financial habits. Imagine that you are flying a plane from point A to B. Even if you zig-zag or get off course, you don’t give up; you make course corrections and keep the plane flying!

Godliness with money requires sacrifices in order to act and grow in faithful stewardship. As you humbly depend on the Lord, you’ll experience a closeness to Him that will motivate you even more.

Keep an eternal perspective. This is not our home, and our mansions are not to be built on Earth. God promises true riches that money cannot buy and eternal rewards that we cannot fathom. Immerse yourself in Scripture, and renew your mind on Truth to overcome the temptations of this world. Focus on the Source of all strength, hope, and peace—He will be your greatest treasure in the new year.

Maybe it will encourage you to know that I am in a group of nine who have committed to another year-long fast from sugar. Disciplines are easy to lose, so I am back on the formula of saying no to what I want today in order to gain what I need for tomorrow.

Stay in touch, and let us know how we can help. We have great budget coaches if you need some extra support.

Happy New Year to you!

This article was originally published on The Christian Post on December 30, 2022.

Dear Chuck,

I hate carrying a balance on our credit cards, but I can’t seem to get them under control. I need some help!

Carrying Heavy Balances

Dear Carrying Heavy Balances,

Unfortunately, inflation is harming the financial situation of many Americans. Rising credit card debt is one of the obvious indicators that millions of others are experiencing the same challenge you are having!

A National Trend

Americans owe approximately $887 billion on their credit cards—13% higher than a year ago. According to the Federal Reserve Bank of New York, credit card debt is rising at its fastest pace in more than 20 years.

It’s been reported that 46% of Americans have credit card debt. 43% say they depend on theirs to cover essential living expenses. They owe an average of more than $6,000. Four in five Americans with credit card debt also carry debt in the form of auto loans, student loans, medical bills, and a mortgage. The Washington Post reports that credit card borrowers are also taking longer to pay off their debt. Any gains made with stimulus money were wiped out by higher prices for gas and groceries, as well as rising interest rates.

The problem with credit card debt is the accompanying high-interest rate. When a balance is carried, the total grows each month. Ted Rossman, senior industry analyst for CreditCards.com, reports that those who have been in credit card debt for at least a year increased by 10% from last year. He notes that minimum payments at 18.17% interest on a credit card balance of $5,270 will take 16 years to pay off at the cost of $11,875.

Getting out of the High-Interest Debt Trap

It is probably your goal, too, but I recommend eliminating credit card debt as soon as possible! This Crown article has several methods that you can use.

According to creditcards.com, the average credit card interest rate on October 26th was 18.91%. As federal interest rates rise, the average APR (annual percentage rate) for new cards is expected to reach 19.66% by winter. Many will pay more than that. Data reveals that the average credit card offer advertises a maximum APR of 26.36%. Last year, the prime rate was 3.25%, but it was 6.25% on 10/26. The Fed will continue to hike rates until they get inflation under control. This will negatively impact those who carry credit card balances because debt will cost more.

Reduce Your Interest Rate

To secure a lower APR, creditcards.com recommends the following:

This shows creditors that you are responsible.

Reduce Expenses and Spending Habits

Reduce the Need for Debt

Big Idea

Serve as your own banker, and avoid paying credit-related interest and fees. Start by saving $1,000, and increase this as you are able until you have 3–6 months of living expenses in an emergency savings account. This will eliminate your need to use credit cards in the future. You simply pay cash and replenish your savings by paying yourself back!

By starting with a small discipline, you will find you will become more disciplined in all areas of managing money. Remember the words Jesus taught His disciples: “One who is faithful in a very little is also faithful in much…” (Luke 16:10a ESV)

Consider contacting Christian Credit Counselors if you need outside support with the financial pain of credit card debt. They are a trusted source of help toward financial freedom.

This article was originally published on The Christian Post on November 4, 2022.

Dear Chuck,

The Parable of the Dishonest Manager looks like Jesus commends lying. Am I right about this? Curious what you think.

Curious Reader

Dear Curious Reader,

Almost two-thirds of Jesus’ parables mention money or possessions and our beliefs and use of them. He talked a lot about money—more than He did about heaven and hell combined. Few are more piercing and often misunderstood than The Parable of the Dishonest Manager in Luke 16.

People frequently conclude that the manager is commended for being dishonest. But that is not so! He was commended for being shrewd. “The master commended the dishonest manager for his shrewdness. For the sons of this world are more shrewd in dealing with their own generation than the sons of light.” (Luke 16:8 ESV)

Good Managers Do Not Waste Money

The word shrewd conjures up, in my mind, the villainous robber baron Henry F. Potter, who tried his best to gain control of the Bailey Brothers Building and Loan Bank in the classic film It’s a Wonderful Life. The antagonist is perfectly portrayed by Lionel Barrymore as a self-centered, greedy, and conniving rich man who is eager for power and control.

But the term “shrewd” is not limited to those with evil intentions. The definition is:

The manager’s behavior, when called into account, indicates that he was guilty of wasting someone else’s possessions. This is the reason he was being fired. It introduces an interesting, sobering idea of one kind of sin: wasting someone else’s money. The Pharisees had to be examining their own stewardship of money as they heard the story unfold.

Culture portrays rich people who are foolish with money. Think about celebrities with rock-star lifestyles, the indulgence of lottery winners, or those lighting cigars with $100 bills. The reality is that people who have earned money and worked hard for it detest waste.

The dishonest manager faced the possibility of unemployment. He would have to beg for a living (which he refused to do), dig ditches (which he was not capable of doing), or come up with a scheme to get what he wanted (a free ride). So he went about reducing or forgiving debtors so that he could make friends who would supply his needs in the future—when everything he had would be gone. (By the way, forgiving our debtors, those who wrong us, is a fantastic way to make friends.)

Are You Shrewd with Money?

Let’s amplify Luke 16:8–9: worldly people are more astute, clever, artfully resourceful, and sharp in their discernment when it comes to the use of money among themselves than Christians are. Christ used the context of this shrewd manager, who is dishonest because he is not walking in the light, for two purposes:

“And I tell you, make friends for yourselves by means of unrighteous wealth, so that when it fails they may receive you into the eternal dwellings.” (Luke 16:9 ESV)

What Does Shrewd Stewardship Look Like?

In the film It’s a Wonderful Life, we see two worldviews portrayed brilliantly by Frank Capra in his depiction of the human condition of a shrewd antagonist vs. a shrewd hero. Henry Potter wants money, power, and control. George Bailey put others before himself. He sacrificed his honeymoon, dreams, and ambitions to save the hard-earned money of the everyday folks of Bedford Falls. He was cheered for his character and integrity as a steward of the Bailey Building and Loan.

So, in the coming days, take a few hours to watch It’s a Wonderful Life again. It is considered one of the top 100 most influential movies of all time. Incredibly, the entire plot is about money and the struggle between selfishness and generosity. It is the story of two very shrewd people! Analyze the way you handle what God provides. Are you more like George Bailey or Henry Potter? Would you be defined as shrewd? Why or why not? What do you need to change in your life to repurpose your use of money?

The Crown God is Faithful devotional provides inspiring and practical biblical wisdom. You can sign up to receive the devotionals daily to help transform not only your finances but also every area of your life.

This article was originally published on The Christian Post on November 25, 2022.

Dear Chuck,

I am exhausted trying to make it to the end of the month while remaining within my budget. I feel like inflation is robbing me of more than my money. I am losing my joy every day that this continues.

Exhausted by Inflation

Dear Exhausted by Inflation,

I wish I could tell you that it will soon be over, but since no man knows the future, I steer clear of trying to predict it. We can only look at the facts and adapt to the reality of our circumstances today. My hope is that this reply will help bring back your joy.

Inflation with Risk of Recession

We are experiencing both inflationary times and a risk of contraction of economic activity. This can cause great fear and uncertainty. Consumer confidence is shaken when unemployment rises, businesses close, and the stock market grows increasingly volatile.

Putting the Brakes on Inflation

On Wednesday, November 2nd, the Fed raised interest rates another .75 percentage points, pushing borrowing costs to the highest level since the Great Recession. More could lie ahead. Could the effort to bring down the cost of living plunge us into a recession? Maybe. The bright side is that savers will benefit from higher rates on their accounts. It is a difficult balance to curb inflation without tipping into a recession, but this is a clear sign that our government wants to contain inflation. Maybe the end is in sight.

Making It to the End of the Month

A Forbes survey of consumers reports that current economic conditions have caused 38% to dine out less, 36% to adjust their budgets, 33% to reduce the miles they drive, and 32% to purchase cheaper or different items than usual. In addition, 23% of Gen-Z consumers plan to take on another job.

If you spend less than you earn, you need not fear a recession or prolonged inflation. How is it possible to spend less than you earn? You either have to earn more money or cut expenses. Pray for wisdom to make wise decisions. Like the Apostle Paul, we can learn to be content in any circumstance, even in the midst of sacrificing comfort.

“Whoever works his land will have plenty of bread, but he who follows worthless pursuits will have plenty of poverty. A faithful man will abound with blessings, but whoever hastens to be rich will not go unpunished.” (Proverbs 28:19–20 ESV)

The Harvard Business Review offers the following tips:

Budget Wisely

Reduce Debt and/or Increase Income

Stay Employable

Rejoice Today

We only have today, so regardless of our circumstances or what may be looming in the future, we should find reasons to rejoice. Every morning that I wake up, I say this verse in my head or sometimes aloud: “This is the day that the Lord has made; let us rejoice and be glad in it.” (Psalm 118:24 ESV). I then go about doing my duty as faithfully as I can, knowing that He will get me through every storm. I hope your joy returns today.

If credit card debt is adding extra stress during these uncertain economic times, consider contacting Christian Credit Counselors. They are a trusted source of help toward financial freedom.

This article was originally published on The Christian Post on November 11, 2022.

Dear Chuck,

My wife and I are finally living on a budget! What are some key steps in our financial plans that we should aspire to achieve now?

Getting Our Act Together

Dear Getting Our Act Together,

Bravo! I read some years ago that about 60% of people say they need or desire to live on a budget, but only 20% actually do it. This is consistent with what I have seen with those I have counseled through the years. Getting this done is a significant step towards financial freedom that will allow you to live on less than you earn while giving, saving, and investing.

A general answer to your question is to follow the steps outlined in the Crown Money Map; however, I was recently reminded of another important financial milestone that I think will help you and your wife. In fact, I think everyone, single or married, should have The Notebook.

The Notebook

I recently visited a class at church where a couple shared their story. They first connected with Crown in 1976, the year Larry began his ministry! They read his books, taught the Crown courses, and have been united in their desire to be good stewards throughout their entire marriage. It was a joy to hear how God had brought them through the ups and downs of their financial circumstances over the nearly 50 years of their marriage. However, the main focus of their class was simply called The Notebook.

Their key point was that very few couples are fully aware of everything they need to know if one or the other were to die unexpectedly. The proverbial question is, “What would we do if one of us were to get run over by a bus?” Of course, nobody thinks it will happen to them, so they told stories of couples, young and old, who found themselves scrambling to know what to do in the fog and confusion of the death of a spouse. One widow in her mid-40s did not even know the addresses of the rental properties they owned. Her husband had managed all of the details of their finances. Not only was she in a deep valley of pain and grief, but she was also overwhelmed with trying to sort through their financial affairs.

Set Your House in Order

Hezekiah was instructed to set his house in order:

“In those days Hezekiah became ill and was at the point of death. The prophet Isaiah son of Amoz went to him and said, “This is what the Lord says: Put your house in order, because you are going to die; you will not recover.” (2 Kings 20:1 NIV)

To accomplish this, our instructors walked us through their “notebook” system. It is a collection of instructions and records for those left behind in the event of one’s death (or even extended hospitalization.) I have known and heard of too many widows who could not access important accounts or find valuable documents with the sudden passing of a spouse. This would be a great task to complete over the holidays.

Buy a large notebook that can hold all of your key documents, either originals or copies, with the location of the originals included. Once completed, agree to store it in a safe place for easy access, and notify next of kin where that is. This is a valuable gift to loved ones that should be updated annually or whenever passwords or other important information change. To get you started, here are the recommended contents:

The Notebook

If you want a concise guide to walk you through the organizing process, I highly recommend Brian Kluth’s 40-page Legacy Organizer. It contains these topics. Crown also has a guide called Blueprint For Your Family’s Finances, complete with forms and worksheets for short- and long-term planning.

It takes some time and discipline to get this done, but just like the work you put in to complete your budget, it will be worth it. You will both appreciate the peace of mind of knowing your house is in order.

To gain more wisdom and insight into how you can effectively steward God’s resources—both time and money—the Crown Stewardship Podcast can be valuable. You can subscribe for alerts of new episodes. I hope you find it beneficial.

This article was originally published on The Christian Post on November 18, 2022.

Dear Chuck,

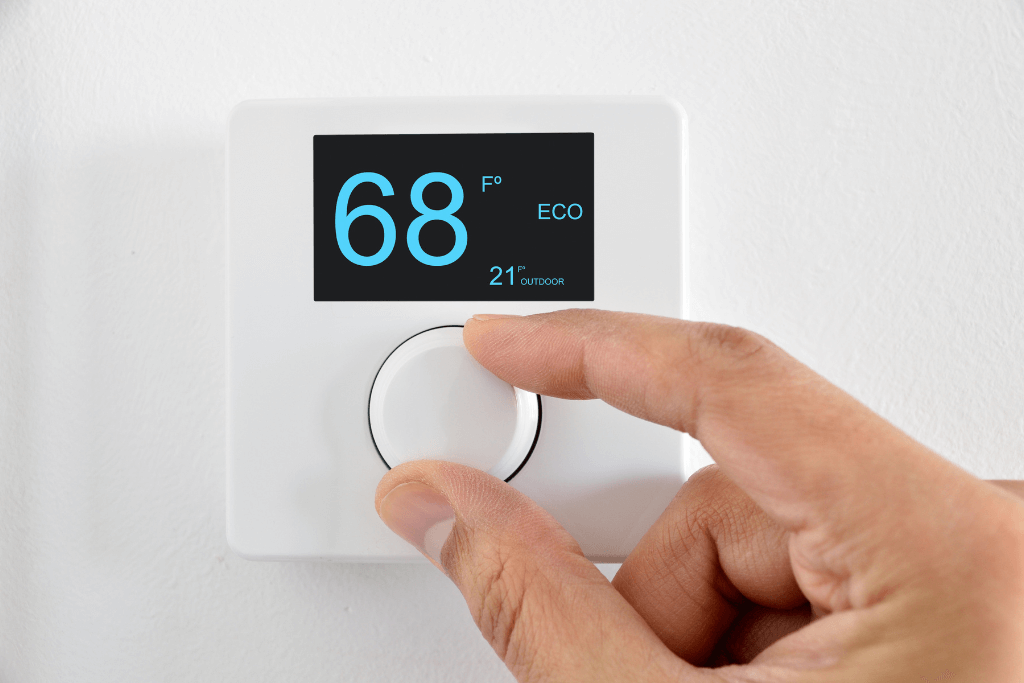

It is already cccccold where I live. My heating bills are getting painful. Any tips to save money this winter?

Bracing for the Winter Bills

Dear Bracing for the Winter Bills,

Unfortunately, we all need to be prepared to pay more to heat our homes in the coming months, regardless of the weather. Why? A hot summer, the Russia-Ukraine War, inflation, and the forecast of a cold winter will all impact our bills.

This week, Business Insider reported that the Energy Information Agency warned that those who use natural gas for heating will spend an average of $931 this winter. This is up 28% ($206) over last year. Prices are up, and colder temperatures are expected. The National Energy Assistance Directors’ Association says home heating costs are reaching the highest level in more than10 years. The cost of heating a home is becoming unaffordable for millions of lower-income families.

I looked at what Europe is doing in its energy crisis and realized we could do that here.

Tips to Reduce Costs in Winter

The Best Savings

Try adjusting your thermostat to 68F for most of the day this winter. The US Department of Energy says that for maximum efficiency, choose eight hours per day to reduce that temperature by 7 to 10 degrees. This can reduce yearly energy costs by up to 10%. Setting the thermostat to a lower temperature will help it retain heat longer and reduce the amount of energy needed to keep it warm. A benefit is that sleeping in cooler temperatures grants more restful sleep.

Tips to Reduce Energy Usage Year Round

Unpack groceries first; then load all refrigerated and frozen items at once.

A cell phone charger, TV, or desk lamp that is plugged in, even though turned off, still uses electricity and costs you money. “Phantom load” is the term used to describe electricity consumed by electronics that are plugged in though not being used. It can add up over time. Walk through each room of your house, and see what is plugged in. Smart strips detect when appliances are not in use and stop sending electricity to them. It’s easy to turn off a strip of multiple things instead of unplugging them individually.

Trouble Paying Bills?

Contact your utility provider, and work out a payment plan. Ask if you qualify for additional assistance. Be patient and polite when discussing your situation. LIHEAP (Low Income Home Energy Assistance Program) may provide assistance. The National Energy Assistance Referral (NEAR) hotline is 866-674-6327.

Prioritize your most urgent payments, such as food, housing, and utilities. Cut back on non-essential spending. Eliminate all impulse purchases by changing your behavior. Take a break from social media, shopping with friends, and browsing on your computer or phone. Adjust your budget now to be sure you can cover the increased costs this winter.

Thank you for the question. I hope you can stay warm and stress-free about your energy bills this winter.

If credit card debt is adding to your financial stress, Christian Credit Counselors is a trusted source of help to ease the financial pain.

This article was originally published on The Christian Post on October 28, 2022.